GHG PROTOCOL

MITIGATION GOAL STANDARD

AN ACCOUNTING AND REPORTING STANDARD FOR

NATIONAL AND SUBNATIONAL GREENHOUSE GAS

REDUCTION GOALS

• 450+ staff

• Issue areas:

– Climate

– Energy

– Food

– Forests

– Water

– Sustainable cities

About WRI

• The GHG Protocol sets the global standard

for how to measure, manage, and report

greenhouse gas emissions

• Convened in 1998 by WRI and WBCSD

• Provides:

– Greenhouse gas accounting and

reporting standards

– Sector guidance

– Calculation tools

– Trainings (webinar, e-learning and in-

person training)

• Standards and tools available free of charge

at www.ghgprotocol.org

About the Greenhouse Gas Protocol

Greenhouse Gas Protocol standards

Corporate Standard

Project Protocol

Product Standard

Corporate Value Chain

(Scope 3) Standard

Mitigation Goal

Standard

Policy and Action

Standard

Global Protocol for

Cities (GPC)

Relationship of different standards

New standards

How to estimate the

greenhouse gas effects of

policies and actions

How to assess progress toward

national or subnational GHG

emissions reduction goals

New standards can help answer:

• Are countries on track to meet their

climate commitments?

• How effective are local or national

policies to drive emissions

reductions?

• Will countries’ actions add up to

limit warming to under 2 degrees

Celsius?

Source for carbon budget: IPCC AR5 Synthesis Report

Need for new standards

• New diversity of national and subnational GHG reduction

goals (e.g., INDCs)

• New needs for estimating GHG effects of policies and

actions (e.g., NAMAs)

• Lack of consistency and transparency in current

approaches

• Lack of capacity

• No international guidelines until now

Standard development process

Secretariat (WRI)

Advisory Committee (30)

Technical Working Groups (80)

Review Group (130)

Pilot Testers (30)

• 270 participants in 40 countries; three year process

Pilot testing: 32 policies/goals in 20 countries/cities

US

Mexico

Costa Rica

Colombia

Chile South Africa

Indonesia

Japan

South Korea

China

India

Bangladesh

Tunisia

UK Belgium

Germany

Israel

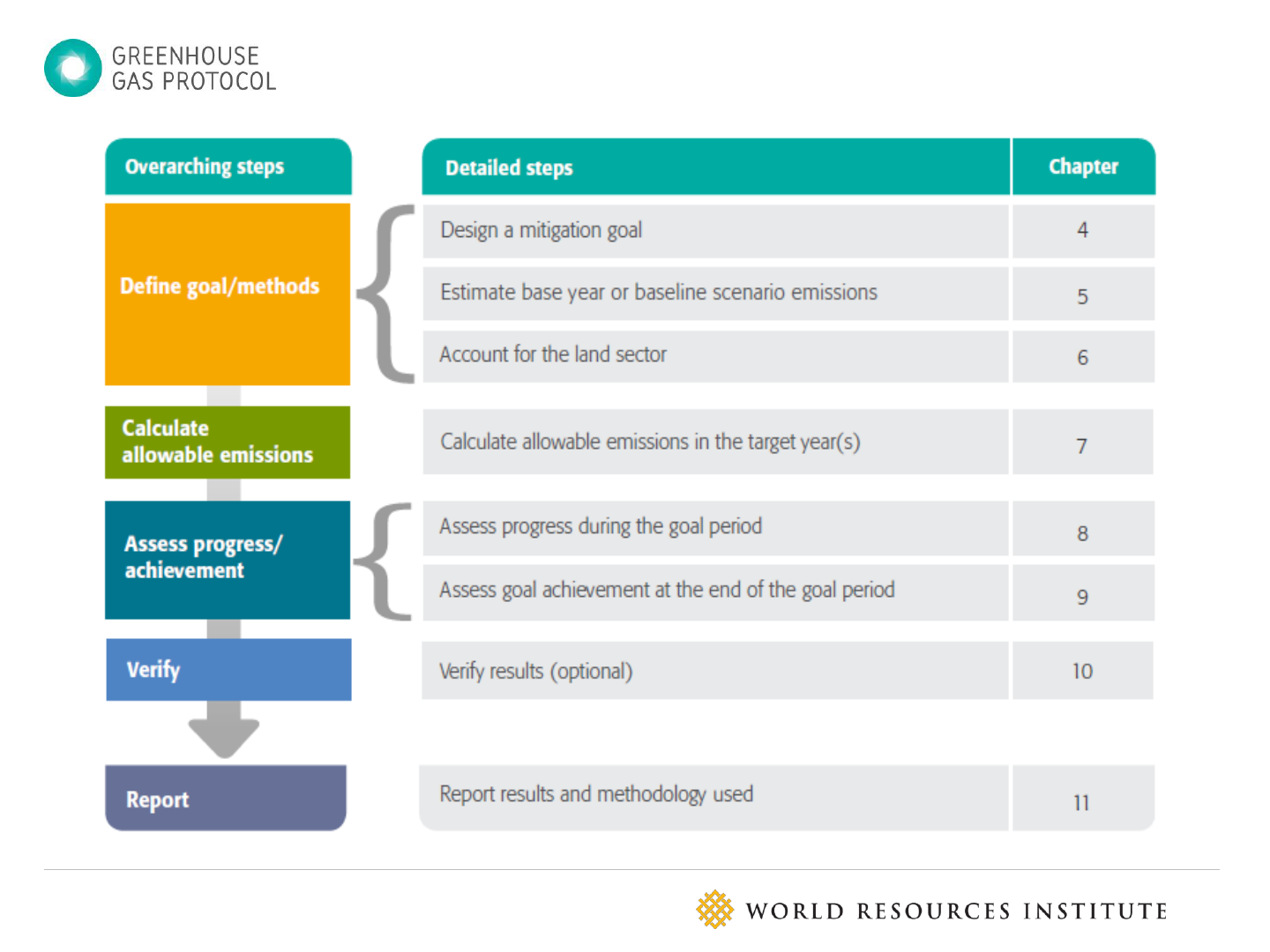

Chapter 1 Introduction

• Guide users in answering the following questions:

– For jurisdictions that do not have a mitigation goal:

Which factors to consider when designing a mitigation

goal

– Before the goal period: How to calculate allowable

emissions in the target year or period

– During the goal period: How to assess and report

progress

– After the goal period: How to assess and report goal

achievement

Why use this standard?

• To help national and subnational governments design and

implement mitigation goals that make a transparent and

meaningful contribution to effective global GHG mitigation

• To help users assess progress toward mitigation goals

• To help policymakers and other decision makers develop

effective strategies for managing and reducing GHG

emissions

How this standard may be useful

• To support consistent and transparent public reporting of

mitigation goal design choices and progress toward goal

achievement

• To support national governments in meeting international

reporting obligations

• To create more international consistency and

transparency in the way jurisdictions design and assess

progress toward mitigation goals

How this standard may be useful (cont.)

Who may want to use the standard?

• Governments (subnational, national)

• Research institutions

• NGOs

• Companies

Before the goal

period: What factors

to consider when

designing a goal and

how to calculate

allowable emissions

in the target year

During the goal

period: How to

assess and report

progress

After the goal

period: How to

assess and report

goal achievement

When the standard can be used

• Voluntary

• All countries and regions

• Economy-wide mitigation

goals and sectoral goals

• Variety of goal types

What does the standard apply to?

Placeholder for picture

Chapter 4 Designing a mitigation goal

• To identify mitigation opportunities

• To track changes during the goal period

• Methodologies to use:

– National jurisdictions: most up-to-date IPCC guidance and

guidelines agreed under the UNFCCC

– Subnational jurisdictions: internationally accepted methods, e.g.

Global Protocol for Community-Scale Greenhouse Gas Emission

Inventories (GPC), in addition to relevant IPCC methods

• Global Warming Potentials (GWP):

– IPCC values based on a 100-year horizon

• As agreed under the UNFCCC, or

• The most recent values published by the IPCC

Preparation: Developing a GHG inventory

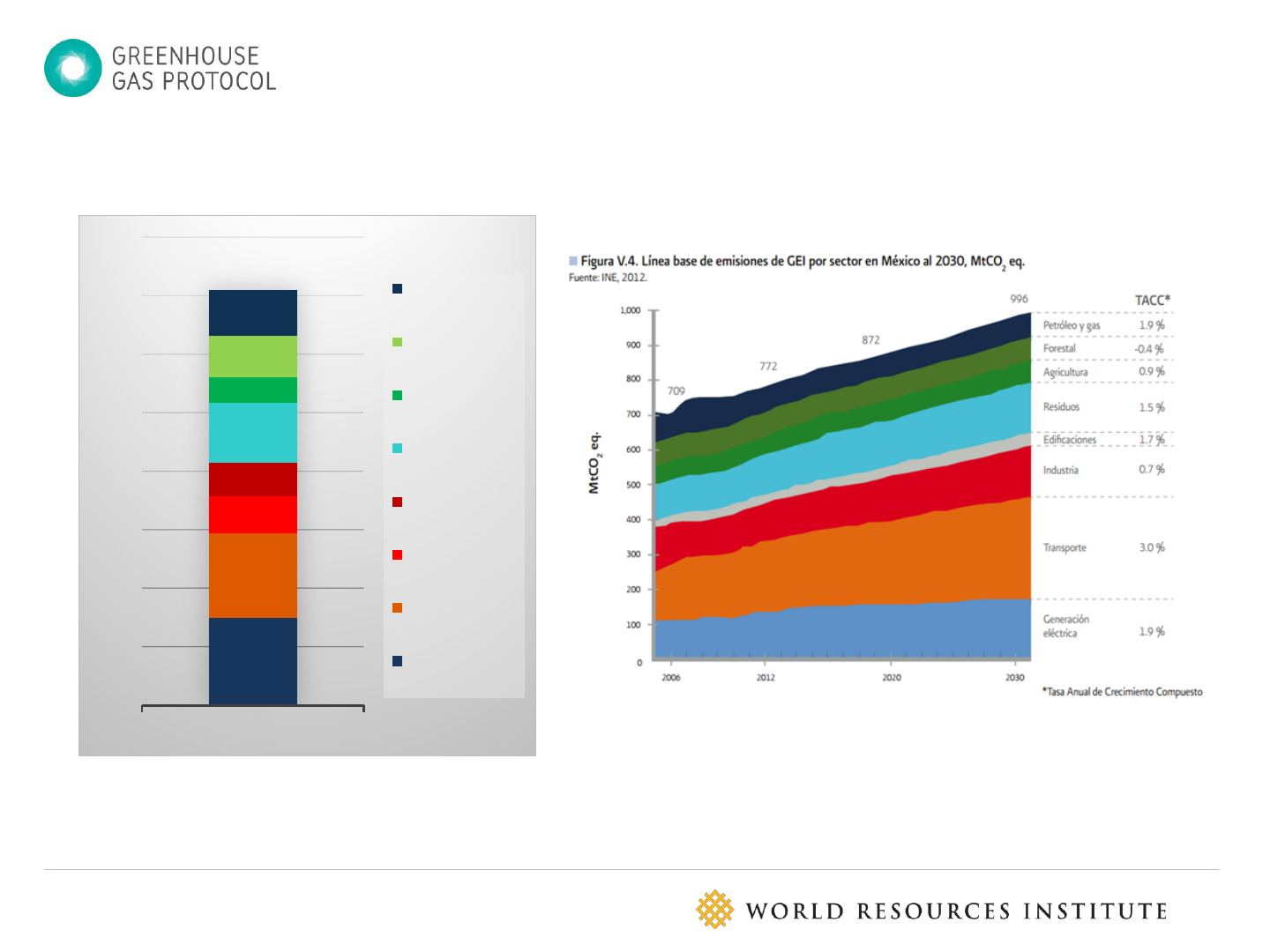

Example Mexico: understanding future trends

0

100

200

300

400

500

600

700

800

MEXICO 2006

Energy sector

other

LULUCF

Agriculture

Waste

Manufacturing

Industrial

processes

Transport

Energy industry

Largest source of emissions is the

energy sector

Largest growth of emissions is

expected in the transport sector

Sources: Mexico’s GHG inventory 2006 (left), UNFCCC GHG data by Party;

Projected BAU emissions per sector, Mexico’s fifth National Communication,

page 253

• To inform the design of the goal, users should consider global

mitigation needs

• Recent findings from climate science, such as IPCC reports,

can help understand the magnitude of emission reductions

needed

Preparation: Assess mitigation needs

• Starts with understanding the GHG inventory and the

contribution of each sector and gas

• Needs to take into account expected future development

• Assessment methods should provide an indication of:

– The magnitude of available reduction opportunities

– Potential cost of each opportunity

– Potential benefits of each opportunity

Preparation: Assess mitigation opportunities

Choose geographic coverage

• Define which geographic area the mitigation goal covers:

– At the national level

– At a regional level

– For one or more cities

National

Regional

City

Choose and define sectors to be included

• The most comprehensive approach is to include all IPCC sectors

in the goal boundary

• High emitting sectors should be included to increase mitigation

opportunities

• Sector definition for the goal should be consistent with the GHG

inventory

• Sectoral goals may be adopted as a way to focus mitigation

efforts and resources on a high emitting sector

Choose treatment of the land sector

The land sector is treated separately because of the significance of

natural-disturbance-related emissions and legacy effects.

Four options:

• Include in the goal boundary: The land sector is included in the

goal boundary, like other sectors.

• Sectoral goal: A sectoral goal for the land sector is separately

designed and assessed, apart from any other mitigation goals a

jurisdiction may have.

• Offset: The land sector is not included in the goal boundary.

Instead, net land sector emissions added to emissions from sectors

included in the goal boundary.

• Do not account for the land sector: The land sector is not

included in the goal boundary.

Choose coverage of in-jurisdiction and out-of jurisdiction

Definition

• In-jurisdiction emissions are emissions from sources located

within a jurisdiction’s boundary.

• Out-of-jurisdiction emissions are emissions from sources located

outside of a jurisdiction’s boundary that occur as a consequence of

activities within that boundary.

Treatment

• Users in national jurisdictions that choose to set a goal for out-of-

jurisdiction emissions shall define separate goals for in-jurisdiction

and out-of-jurisdiction emissions.

• Users in subnational jurisdictions shall report whether the goal

covers out-of-jurisdiction emissions and, if so, which out-of-

jurisdiction emissions are included and excluded.

Select GHGs covered

• Recommended comprehensive coverage of 7 Kyoto greenhouse

gases

– Carbon dioxide (CO

2

)

– Methane (CH

4

)

– Nitrous oxide (N

2

O)

– Hydrofluorocarbons (HFCs)

– Perfluorocarbons (PFCs)

– Sulfur hexafluoride (SF

6

)

– Nitrogen triflouride (NF

3

)

• Users may include fewer greenhouse gases depending on

objectives, data quality, mitigation opportunities, and capacity.

Choose mitigation goal type

• The standard is primarily designed to support four goal types

Example of a base year emissions goal

Example of a fixed-level goal

Example of a base year intensity goal

Example of a baseline scenario goal

Example of static versus dynamic baseline scenarios

• Emission reductions to be

achieved by policies, actions,

or projects

• Baseline scenario goals framed

in terms of emission

reductions to be achieved by

policies, actions or projects

• Non-GHG goals

Some parts of the Mitigation Goal

Standard are useful. Also see the

Policy and Action Standard for

further guidance.

Other goal types

Placeholder for picture

• Choose a single year of historical data (base year) or an average of

historical data over multiple years (base period)

• Choose a base year or base period for which representative,

reliable, and verifiable emissions data are available to enable

comprehensive and consistent tracking of emissions over time

Choose base year

• Single-year targets are more vulnerable to inter-annual fluctuations

• Emissions can increase during the goal period and then be reduced

only shortly before the target year larger amount of cumulative

emissions

Single year goals

• Fluctuations in

emissions can

pose challenges

to meeting a

single-year goal

• Commitment to reduce, or control the increase of, annual emissions

(or emissions intensity) by an average amount over a target period

• Adopting multi-year goals will have a better chance of limiting

cumulative emissions over the goal period

Average multi-year goals

• Commitment to reduce, or control the increase of, annual emissions

(or emissions intensity) by a specific amount each year over a

target period

Annual multi-year goals

• It is likely that

multi-year goals will

lead to transformed

emissions pathways

in which emissions

continue to be

reduced after the

goal period

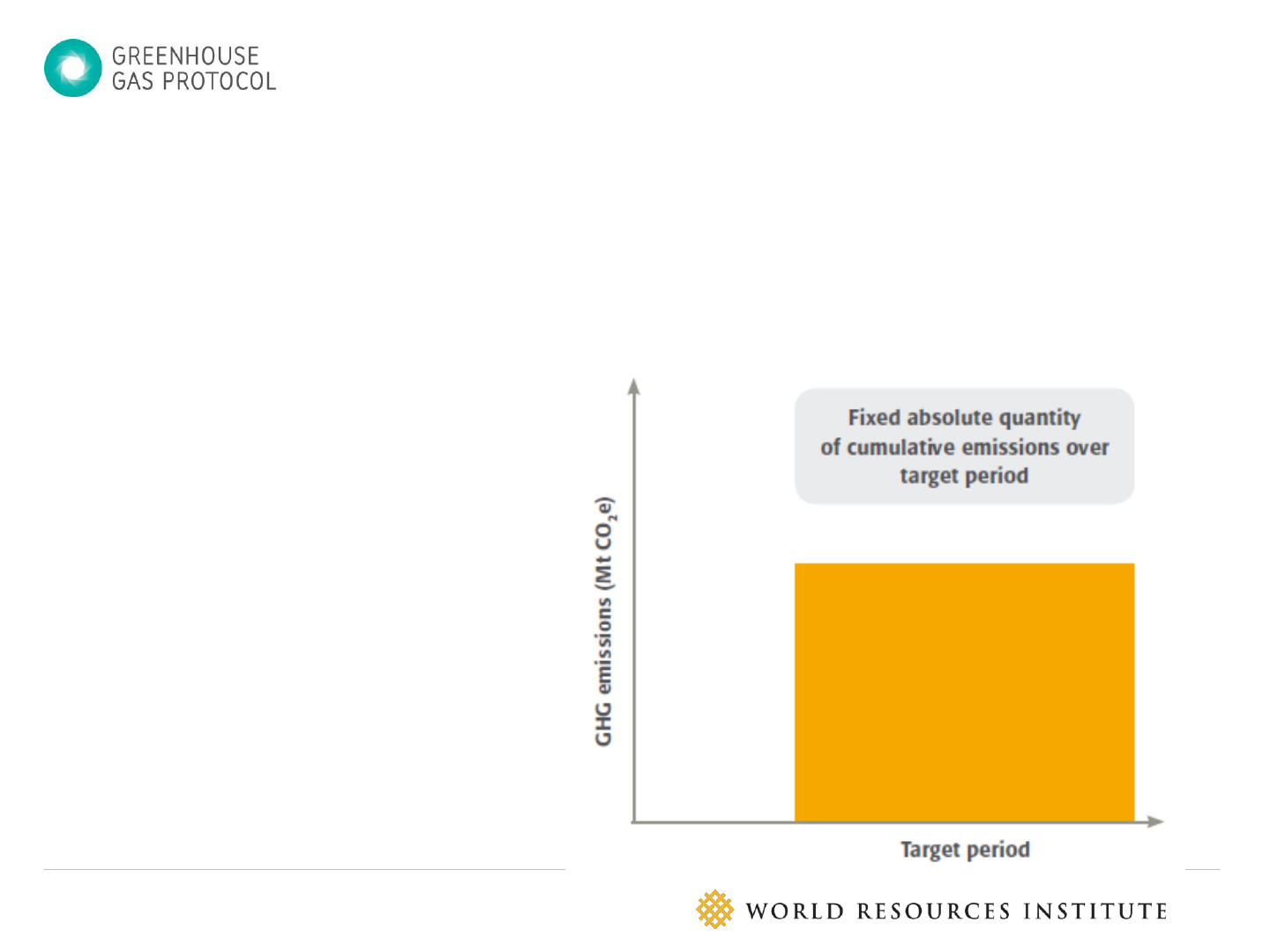

• Commitment to reduce, or control the increase of, cumulative

emissions over a target period to a fixed absolute quantity

• Cumulative multi-year goals are often referred to as “carbon

budgets.”

Cumulative multi-year goals

• Annual or average

multi-year goals can

also be converted to

cumulative multi-

year goals

• Average and

cumulative multi-

year goals offer

more flexibility

• Long-term goal of reducing emissions by at least 80 percent

below 1990 levels by 2050

• Individual carbon budgets for intermediate periods with

growing stringency

Example: UK’s fixed-level, cumulative multi-year goals

• Choose a single year (target year) or a multi-year period (target

period) for the goal

• Choose:

– Short-term goals

– Long-term goals

– A combination of both

• The most robust approach is to set a combination of short- and

long-term goals that are consistent with an emissions trajectory that

phases out greenhouse gas emissions in the long-term

• In particular, users that choose a single-year goal should consider

adopting a series of single-year goals for different timeframes

Choose target year or target period

• A goal may be achieved using any combination of emission reductions from

within the goal boundary (domestic reductions) and transferable emissions

units generated outside of the goal boundary

Decide on use of transferable emissions units

– Emissions allowances from emissions trading programs

– Offset credits generated from outside of the goal boundary

• if a jurisdiction is expected to be a net seller of emissions

units in the target year or period, the jurisdiction will need

to plan for greater domestic emission reductions to

achieve the goal.

• Understanding the quantity of units that are expected to

be sold can help policymakers design mitigation strategies

for any additional emission reductions needed to achieve

the goal.

If selling units

• Real: Emission reductions or removals represent actual emission

reductions and are not artifacts of inaccurate or incomplete accounting.

• Additional: Emission reductions or removals are beyond what would

have happened in the absence of the incentive provided by the offset

credit program or project.

• Permanent: Emission reductions or removals are irreversible or if

sourced from projects subject to potential reversal have guarantees to

ensure that any losses are compensated for.

• Transparent: Offset credits are publicly and transparently registered

with unique serial numbers to clearly document offset credit generation,

transfer, retirement, cancellation, and ownership.

Criteria for use of offset units

• Verified: Offset credits have been appropriately validated and verified to

a standard that ensures reproducible results by an independent third

party that is subject to a viable and trustworthy accreditation system.

• Owned unambiguously: Ownership of GHG reductions or removals is

clear by contractual assignment and/or government recognition of

ownership rights. Transfer of ownership of offset credits must be

unambiguous and documented.

• Addresses leakage: Emission reductions or removals are generated so

as to address leakage.

Criteria for use of offset units (cont’d)

• Rigorous monitoring and verification protocols: Allowances

are generated based on robust methods for measuring emissions

that ensure the quality and comparability of underlying emissions

data.

• Transparent tracking and reporting of units: Allowances are

publicly and transparently registered to clearly document their

generation, transfer, and ownership. Emissions trading programs

are transparent regarding rules and procedures for monitoring,

reporting, and verification, as well as compliance and

enforcement.

• Stringent caps: Emissions trading programs have stringent caps

that limit the amount of emissions in a given time period to a

level lower than would be expected in a business-as-usual

scenario.

Criteria for use of allowances from emissions trading

• Double claiming occurs when a single transferable

emissions unit is claimed by two different jurisdictions and

applied toward the mitigation goal of both

• Double selling occurs when a single unit is sold twice

• Double issuance occurs when more than one transferable

emissions unit is generated for one unit of emission

reduction

Types of double counting

• A registry that lists the quantity, status (canceled, retired, or

banked), ownership, location and origin of transferable emissions

units held by a jurisdiction

• A transaction log that records the details of each transaction

between registry accounts, including the issuance, holding,

transfer, and acquisition of transferable emissions units

• Agreements between buyers and sellers that specify which party

has the exclusive right to claim each unit and specifies what

percentage, if any, is shared

• Legal mandates that disallow double counting and employ

penalty and enforcement systems

• Information sharing to identify units that are already

registered in other programs

Mechanisms to prevent double counting

Users should define an ambitious

goal level that:

• Substantially reduces emissions

below the jurisdiction’s business-

as-usual emissions trajectory

• Corresponds to an emissions

trajectory that is in line with the

level of emissions reductions

necessary to avoid dangerous

climate change impacts, as

determined by the most recent

climate science.

Define the goal level

• Choice of goal type:

Base year emissions goals and fixed-level goals are

• simpler to account for,

• more certain, and

• more transparent

Users seeking to accommodate short-term emissions increases

should consider adopting base year emissions goals or fixed-level

goals that are framed as a controlled increase in emissions from

a base year.

Static baseline scenario goals provide more certainty and

transparency regarding intended future emissions levels than

dynamic baseline scenario goals.

Key considerations for goal design

• Choice of goal timeframe:

– Multi-year goals have a better chance of limiting cumulative

emissions over the goal period than single-year goals

– Adopting a combination of short-term and long-term goals

provides more clarity for long-term planning and better

ensures a decreasing emissions pathway.

Key considerations for robust goals (cont’d)

• Use of transferable emissions units: Ensuring that any

transferable emissions units applied toward a goal

– Meet the highest quality principles

– Are generated in the target year or period

– Include mechanisms for tracking units to double counting

• Choice of goal level: The goal level should

– Significantly reduce emissions below the jurisdiction’s business-

as-usual emissions trajectory

– Correspond to an emissions trajectory that is in line with

emissions reductions necessary to avoid dangerous climate

change, as determined by the most recent climate science.

Key considerations for robust goals (cont’d)

Chapter 5 Estimating base year / baseline scenario

emissions

• Develop and report a complete inventory for the base year

or base period

• Aggregate emissions from the GHG inventory for all gases

and sectors that are included in the goal boundary,

including out-of-jurisdiction emissions, if relevant

• For base periods: calculate the average annual emissions

level over the base period

Calculate base year / base period emissions

• Divide base year emissions by the level of output in the

base year

• Data for the level of output should be reliable, verifiable,

and gathered from official sources

• Report the level of output in the base year, and data

sources used

Calculating base year emissions intensity

Estimating baseline scenario emissions:

Choose emissions projection model

• The choice of model typically reflects a tradeoff among

several factors, including:

– available resources, including financial resources and

technical expertise;

– data availability;

– model performance, including level of sophistication and

suitability for jurisdiction;

– software costs;

– alignment with other models being used by the

jurisdiction;

– the expected use of the model outputs

Identify emissions drivers

• Economic activity (for example, GDP and sectoral composition of

GDP)

• Structural changes in economic sectors (e.g., shifts from

manufacturing to service sector jobs, shifts of industrial production

between countries)

• Energy prices by fuel type

• Energy supply and demand by fuel type

• Emissions intensity by fuel type

• Population and degree of urbanization

• Technological development

• Land-use practices

Defining assumptions using published data

• Existing data sources of sufficient quality may be available to define

assumptions for emissions drivers:

– peer-reviewed scientific literature,

– government statistics,

– reports published by international institutions (such as IEA,

IPCC, IMF, World Bank, UN, etc.),

– national, regional, state, city, or sector-level sources specific to

the jurisdiction, and

– economic and engineering analyses and models

Identify policies and actions to include

• Emissions will be affected by policies and actions implemented in

the jurisdiction

• This includes policies and actions designed to reduce emissions as

well as those designed to meet other objectives

• Which policies are included in the baseline scenario and the

assumptions made about their likely effects on emissions can have a

significant effect on resulting baseline scenario emissions

• Users should include all policies and actions that:

(1) have a significant effect on GHG emissions, either increasing or

decreasing them, and

(2) are implemented or adopted in the year the baseline scenario is

developed

Example: Chile’s national baseline emissions

Develop a range of plausible scenarios

• A range of baseline scenarios reflects the upper and lower bounds of

plausible emissions trajectories associated with a range of assumptions

• Out of the range choose and report a single baseline scenario against

which to set the goal and track progress

Example: Chile’s national baseline emissions

Chapter 6 Accounting for the land sector

Selecting and reporting the accounting method

• Choose accounting method:

– Land-based accounting assesses net emissions (emissions +

removals) of select land-use categories,

– Activity-based accounting assesses net emissions of select

land-use activities

Land-based accounting

• Determines the scope of accounting based on six land-use

categories:

– Forestland

– Cropland

– Grassland

– Wetland

– Settlement

– Other

• Accounting should cover all lands within the category of

interest

Activity-based accounting

• Bases the accounting on a predetermined set of land-use

practices

• The aim is to limit accounting to those lands subject to direct

human influence and thereby exclude non-anthropogenic fluxes

• All anthropogenic activities that result in changes in carbon pools

or fluxes and emissions resulting from land-use change activities

should be included

• Land sector accounting methods are used to assess changes in

net emissions (emissions + removals) within each land-use

category or activity

• There are three land sector accounting methods:

(1) relative to a base year/period emissions (also known as net-

net),

(2) without reference to base year/period or baseline scenario

emissions (also known as gross-net);

(3) forward-looking baseline

Choose the accounting method

Accounting relative to base period emissions

Accounting without reference

Forward-looking baseline accounting

• Base year emissions goal: Account relative to base year/period

emissions (also known as net-net accounting)

• Fixed-level goal: Account in the target year/period, without

reference to base year/period or baseline scenario emissions

(also known as gross-net accounting)

• Base year intensity goal: Account for emissions intensity relative

to a base year/period (also known as net-net accounting)

• Baseline scenario goal: Use forward-looking baseline accounting

method

Recommended approach

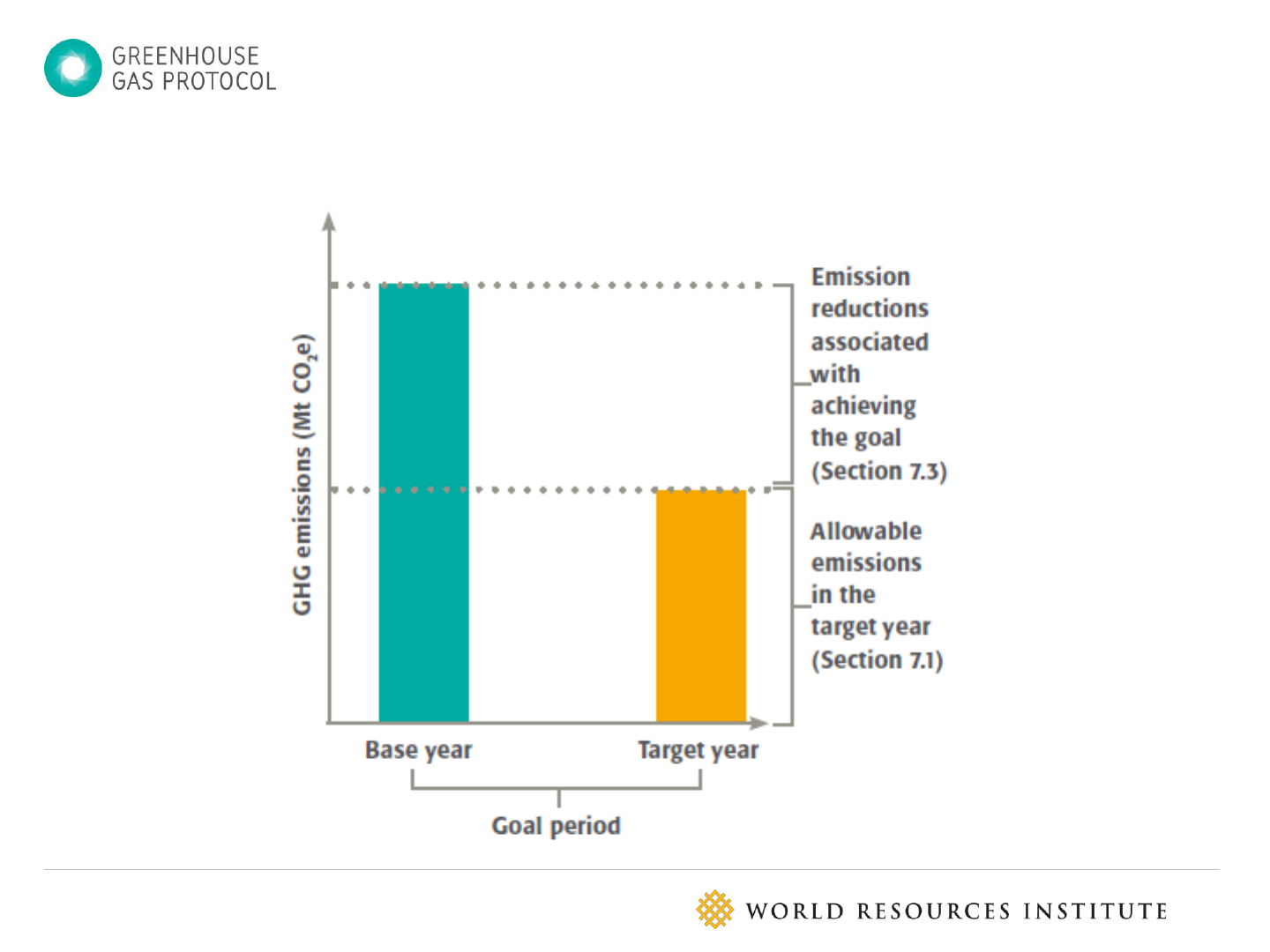

Chapter 7 Calculate allowable emissions

• Allowable emissions represent the maximum quantity of

emissions that may be emitted in the target year or target period

that is consistent with achieving the mitigation goal

• Calculating allowable emissions provides users with critical

information for

– Decision making,

– Designing mitigation strategies,

– Assessing progress during the goal period, and

– Assessing goal achievement

Calculating allowable emissions

Example of allowable emissions for a base year goal

Example of allowable emissions for a baseline goal

Equations for calculating allowable emissions

Equation for calculating allowable emission intensity

Setting milestones: Example along a linear emissions path

Chapter 8 Assessing progress

• The frequency of assessment depends on:

– stated objectives,

– policy-making needs,

– data availability,

– cost, capacity, and

– stakeholder demand

• If feasible, progress should be reported on an annual basis

• The same frequency should be used throughout the goal period

Choose frequency of assessment

Assessing progress

• There may be a time lag between the GHG inventory year and the

year in which the inventory is actually published

• Official statistics for the unit of output may not be immediately

available

A complete assessment will need to be based on a published

inventory and official statistics

Develop GHG inventory for reporting year

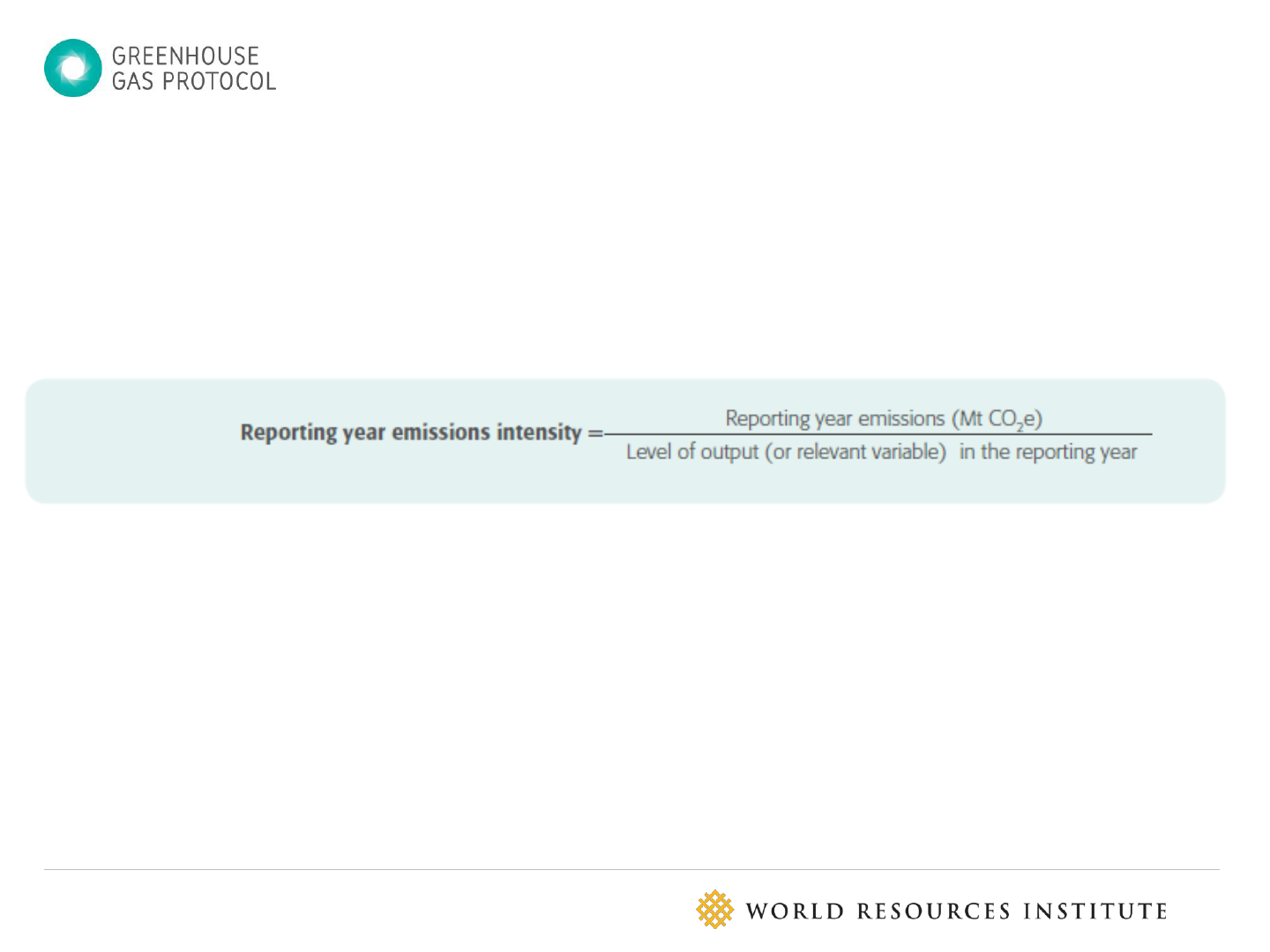

Calculate reporting year emission intensity

• What to recalculate:

1. Base year emissions, base year emissions intensity, or

baseline scenario emissions;

2. Allowable emissions or emissions intensity; and/or

3. Reporting year emissions

• Why:

1. Due to methodological changes

2. Due to changes in emissions drivers (dynamic baseline

scenarios)

3. Due to changes to the goal itself

Recalculate emissions (if relevant)

Calculate change in emissions

Calculate additional reductions needed to achieve the goal

Example: Assessing progress toward South Africa’s mining

sector goal

Example: Tracking progress towards Israel’s goal

• Develop an informational baseline scenario that includes all

implemented and adopted policies and uses the reporting year as

the start year

• Compare baseline scenario emissions in the target year(s) to

allowable emissions

Assess whether the jurisdiction is on track to achieve the goal

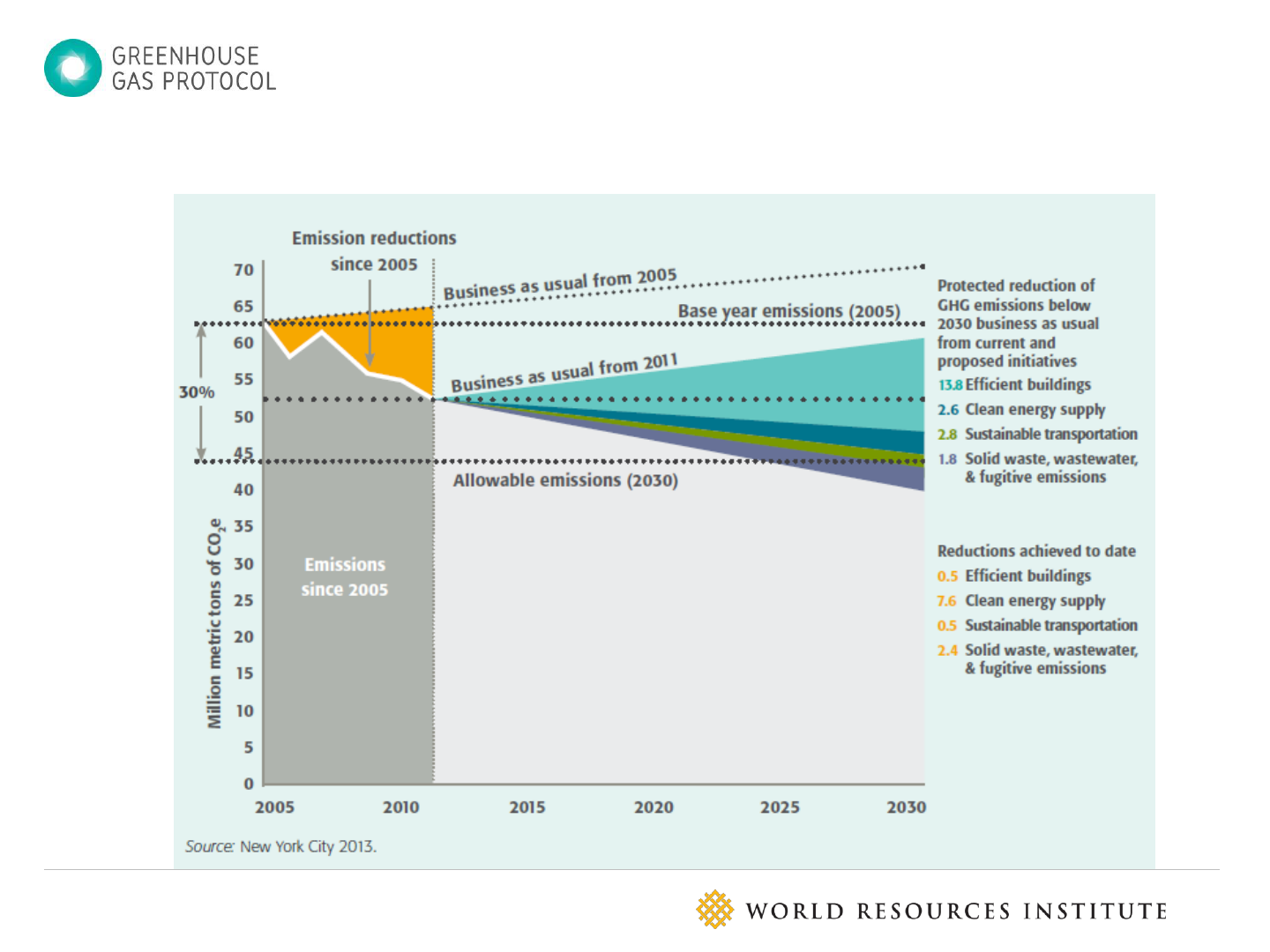

Example: New York City’s progress toward meeting its goal

Chapter 9 Assessing goal achievement

Calculate target year/period emissions

• Develop a complete GHG inventory for the target year(s) or period

• Aggregate emissions from the GHG inventory for all gases and

sectors that are included in the goal boundary, including out-of-

jurisdiction emissions, if relevant

A complete assessment will need to be based on a published

inventory and official statistics

Determine quantity of transferable emissions

• Report the

– type,

– vintage, and

– quantity (in terms of Mt CO

2

e)

of transferable emissions units retired and sold in the target year, relevant

year of the target period, or over the target period

• Units that have been applied toward the goal are retired permanently and

cannot be used again by the retiring jurisdiction or any other jurisdiction

• Use sample GHG balance sheet to report and track units

Sample GHG

balance sheet

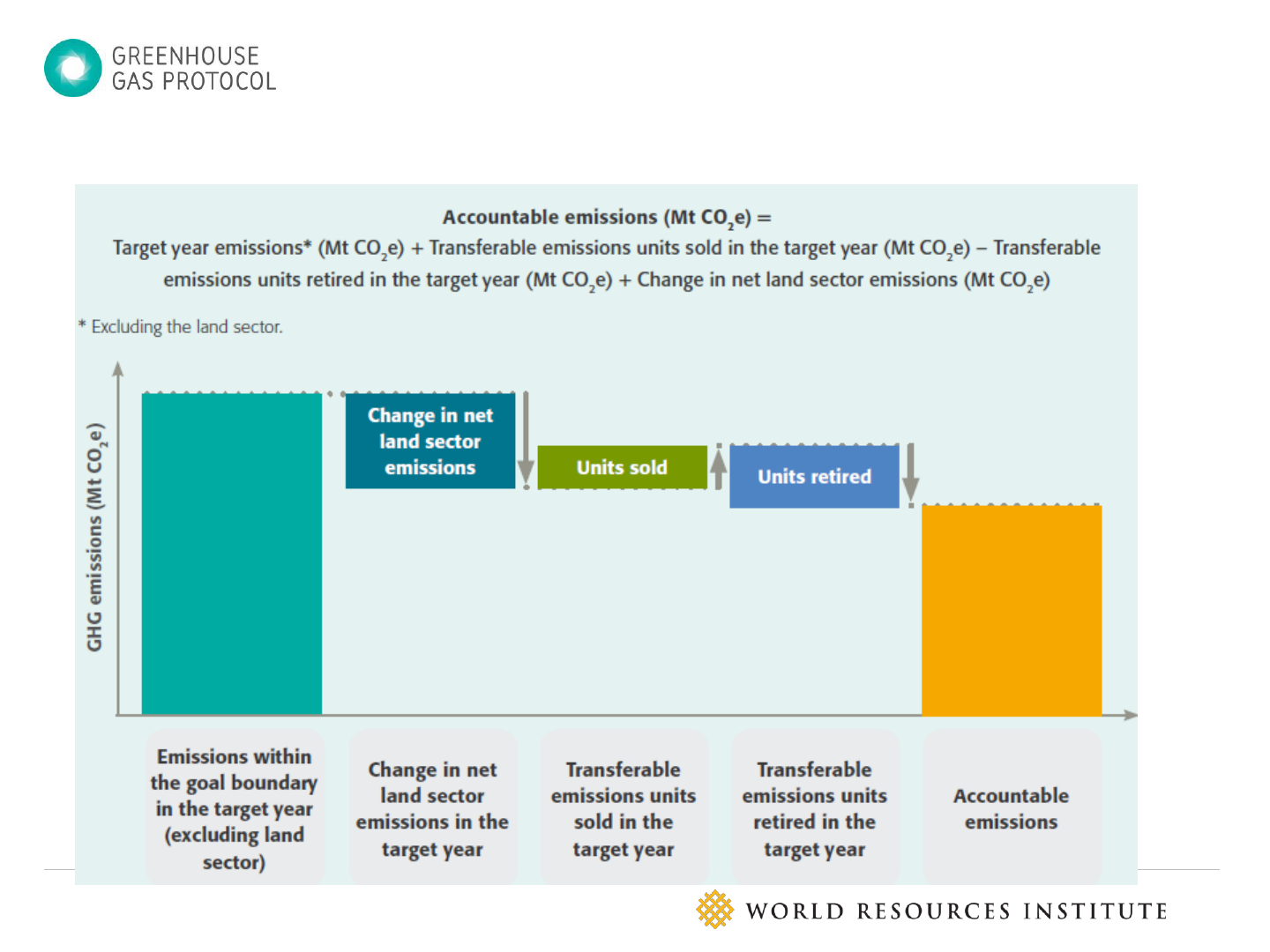

• Accountable emissions are the quantity of emissions and

removals that users apply toward achieving the goal, and may

take into account sales and retirement of transferable emissions

units and change in net land sector emissions, depending on

goal design.

Calculate accountable emissions

Calculate accountable emissions (no land use offsets)

With treatment of the land sector as an offset

Recalculate emissions

• To maintain the consistency of time-series data and enable

meaningful comparisons of emissions at the end of the goal period,

emissions and other values may need to be recalculated:

– Due to methodological changes

– Due to changes in emission drivers (for dynamic baselines)

• Report any emissions recalculations, including recalculations of base

year emissions, base year emissions intensity, baseline scenario

emissions, and allowable emissions or emissions intensity, and the

recalculated values alongside the original values

Example: the City of Seattle

• Accountable emissions

exceeded allowable emissions by 0.34 Mt

CO

2

e, and, thus Seattle’s goal was not achieved.

Chapter 11 Reporting

• Report the results of the assessment according to a standardized set

of reporting requirements

• Optional reporting information can further enhance transparency

• Four parts to the reporting requirements/template:

1. Design of the goal

2. Calculation of allowable emissions in the target year or period

3. Assessing progress during the goal period

4. Assessing goal achievement

Reporting