1

CONSUMER FINANCIAL PROTECTION BUREAU | JUNE 2020

Data Point: 2019

Mortgage Market Activity

and Trends

A First Look at the 2019 HMDA Data

This is another in an occasional series of publications from the Consumer Financial Protection

Bureau’s Office of Research. These publications are intended to further the Bureau’s objective of

providing an evidence-based perspective on consumer financial markets, consumer behavior,

and regulations to inform the public discourse. See 12 U.S.C. §5493(d).

[1]

[1]

This report was prepared by Young Jo, Feng Liu, Akaki Skhirtladze, and Laura Barriere.

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 2

Table of contents

Table of contents ......................................................................................................... 3

1. Introduction .............................................................................................................4

2. HMDA data coverage of the mortgage market ...................................................... 8

3. Mortgage applications and originations .............................................................11

4. Mortgage outcomes by demographic groups..................................................... 19

4.1 Distribution of home loans across demographic groups .......................... 19

4.2 Average loan size by demographic group ................................................. 27

4.3 Jumbo lending........................................................................................... 31

4.4 Variation across demographic groups in nonconventional loan use ....... 32

4.5 Denial rates and reasons ........................................................................... 36

5. Incidence of higher-priced lending ...................................................................... 46

6.1 HOEPA loans ........................................................................................ 55

6. Lending institutions ..............................................................................................58

7. Conclusion ............................................................................................................. 69

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 3

1. Introduction

This Data Point article provides a first overview of residential mortgage lending in 2019 based

on data collected under the Home Mortgage Disclosure Act (HMDA). HMDA is a data collection,

reporting, and disclosure statute enacted in 1975. HMDA data are used to assist in determining

whether financial institutions are serving the housing credit needs of their local communities;

facilitate public entities’ distribution of funds to local communities to attract private investment;

and help identify possible discriminatory lending patterns and enforce antidiscrimination

statutes.

1

Institutions covered by HMDA are required to collect and report specified information

about each mortgage application acted upon and mortgage purchased.

2

The data include the

disposition of each application for mortgage credit; the type, purpose, and characteristics of

each home mortgage application or purchased loan; the census-tract designations of the

properties; loan pricing information; demographic and other information about loan applicants,

such as their race, ethnicity, sex, age, and income; and information about loan sales.

3

The 2019 HMDA data are the second year of data that incorporate changes made to HMDA

under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (DFA). Among

the changes mandated by the DFA were changes to some data points and also authorizing the

Bureau to collect new and revised data points. The Bureau issued a final rule implementing

these and other changes in October 2015 (2015 HMDA rule).

4

The 2015 HMDA rule made four

primary changes to the data collected starting in January 1, 2018: (1) mandated reporting of

open-end lines of credit (LOCs); (2) changed the transactional coverage definition from loan-

purpose-based to one based primarily on whether the loan was secured by a dwelling; (3)

modified definitions and values of some existing data points; and (4) required reporting of 27

new data points.

5

1

For a brief history of HMDA, see Federal Financial Institutions Examination Council, “History of

HMDA,” available at www.ffiec.gov/hmda/history2.htm.

2

The 2019 HMDA data, which are used for the analysis of this Data Point, cover mortgage applications

acted upon and mortgages purchased during the calendar year of 2019 and reported in 2020.

3

See https://s3.amazonaws.com/cfpb-hmda-public/prod/help/2019-hmda-fig.pdf for a full list of items

reported under HMDA for 2019.

4

See Home Mortgage Disclosure (Regulation C), 80 FR 66128 (Oct. 28, 2015). In September 2017, the

Bureau published in the Federal Register a rule which made a few technical corrections to and clarified

certain requirements of the rule implementing HMDA. This rule also increased the threshold for

collecting and reporting data about open-end LOCs for a period of two years. See 82 FR 43088 (Sep. 13,

2017).

5

Beginning with 2018 HMDA data, the Economic Growth, Regulatory Relief, and Consumer Protection

Act (EGRRCPA) exempted certain insured depository institutions and credit unions from the requirement

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 4

Consistent with the last year, the Consumer Financial Protection Bureau (hereafter, Bureau) is

issuing two Data Point articles. This first article follows a consistent format as previous annual

articles released by the Federal Reserve, which accompanied the release of a public version of

the aggregate HMDA data, and focuses specifically on trends in mortgage applications and

originations. By examining the HMDA data over several years (2004–2019), this article closely

analyzes trends using historical data points that had been collected prior to the 2015 HMDA

Rule. The Bureau’s second Data Point article, which is scheduled to be published later, includes

analyses of open-end LOCs and dwelling-secured applications not covered in the first article.

Furthermore, the second article focuses on an in-depth cross-sectional analysis of new or

revised data points that were added under the 2015 HMDA rule. The Bureau is releasing these

two articles at different times to make the static application-level 2019 HMDA data file available

to the public as soon as possible.

With the first Data Point article, the Bureau is publishing a static application-level 2019 HMDA

data file that consolidates data from individual reporters. The data file is modified to protect

applicant and borrower privacy.

6

The data file and the two Data Point articles reflect the data as

of April 27, 2020. Though this static file will not change, the Bureau will also provide an updated

file separately to reflect any later resubmissions or late submissions. The results using the

updated file may differ from those reported in this Data Point article, although the Bureau

expects them to be largely consistent.

The remainder of this article summarizes the 2019 HMDA data and recent trends in mortgage

applications and originations. The Bureau seeks to make the 2019 HMDA data as comparable as

possible to HMDA data from previous years, including HMDA data prior to the data collected in

2018 when the majority of the 2015 HMDA Rule took effect. To do this, the Bureau excludes 2.1

million open-end LOCs except reverse mortgages and the 1.1 million records that were dwelling-

secured but for a purpose other than purchase, home improvement, or refinance, because such

records were not required to be reported prior to 2018. In addition, the Bureau converts any

to collect and report data on 26 of the 27 new data points added under the 2015 HMDA rule for certain

types of entities and transactions. For more details on the 2015 HMDA rule, see the “Data Point: 2018

Mortgage Market Activity and Trends,” available at https://www.consumerfinance.gov/data-

research/research-reports/data-point-2018-mortgage-market-activity-and-trends/

6

For more information concerning these modifications and the Bureau’s analyses under the balancing

test it adopted to protect applicant and borrower privacy while also fulfilling HMDA’s disclosure

purposes, see 84 FR 649 (January 1, 2019).

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 5

changes made to data points by the 2015 HMDA rule back to their historical values and does not

incorporate any of the new HMDA fields into the first article.

7

Some of the key findings are:

8

5,496 institutions reported closed-end records in 2019, down 3 percent from the 5,666

which reported in 2018.

In total, the number of closed-end originations in 2019 increased by 26 percent, from 6.4

million in 2018 to 8.1 million in 2019. Most of the increase was driven by an increase in

the number of refinance loans. For example, the number of home-purchase loans

secured by one-to-four-family properties increased by about 174,000, whereas the

number of refinance loans nearly doubled from 1.9 million in 2018 to 3.4 million in 2019.

The number of home improvement loans secured by dwellings declined slightly from

183,000 in 2018 to 174,000 in 2019.

Black borrowers increased their share of home-purchase loans for one-to-four-family,

owner-occupied, site-built properties in 2019. Approximately 7 percent of such loans

went to Black borrowers, up from 6.7 percent in 2018. In contrast, 60.3 percent went to

non-Hispanic White borrowers, down slightly from 62 percent in 2018. The share of

Asian borrowers declined by 0.2 percentage points whereas that of Hispanic White

borrowers increased by 0.3 percentage points. The share of home-purchase loans to low-

or-moderate-income (LMI) borrowers increased slightly from 28.1 percent in 2018 to

28.6 percent in 2019.

Unlike other racial and ethnic groups, Asian borrowers increased their share of refinance

loans for a first-lien, one-to-four-family, owner-occupied, site-built properties from 3.7

percent to 5.4 percent in 2019. In addition, the share of refinance loans for high-income

borrowers and properties in high-income neighborhoods also increased by 2.1

percentage points and 5.0 percentage points, respectively.

Not adjusting for inflation, the average loan amount for a first-lien, one-to-four-family,

owner-occupied, site-built home-purchase and refinance loans increased by 4.2 percent

and 23.4 percent, respectively. For the first time since the Great Recession (2009/2010),

the average home-purchase loan amount for Hispanic White borrowers surpassed their

pre-Recession peak level. The average home-purchase loan amounts for Asian, Black,

7

See https://www.consumerfinance.gov/policy-compliance/guidance/hmda-implementation/ for a list of

new HMDA fields, as well as additional reference material about recent changes to the HMDA reporting.

8

For 2019 mortgage lending activities, this Data Point article is based on the analysis of the static

consolidated application-level 2019 HMDA data file made available concurrently to the public. Analyses

of the prior years’ data in this Data Point article are based on the updated consolidated application-level

HMDA data, rather than the static data initially released to the public for such years. Accordingly, the

results herein for prior years’ HMDA data may differ from those initially released in prior years.

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 6

and non-Hispanic White borrowers had already surpassed their pre-Recession peaks

before 2019.

The denial rates for a first-lien, one-to-four-family, owner-occupied, site-built home-

purchase and refinance loans decreased between 2018 and 2019. The decline was

particularly large for refinance loans, where the denial rate decreased by 33.8 percent,

compared with 10 percent decrease for home-purchase loans.

Black and Hispanic White borrowers continued to be much more likely to use

nonconventional loans (insured by Federal Housing Administration (FHA) or a guarantee

from the Department of Veterans Affairs (VA), the Farm Service Agency (FSA), or the

Rural Housing Service (RHS)) than other racial and ethnic groups. In addition, the share

of nonconventional loans for home-purchase increased slightly from 2018 to 2019, putting

an end to the general downward trend observed since the Great Recession.

Nondepository institutions’ (non-DIs’) share of mortgage originations continued an

upward trend that began back in 2010. In 2019, this group of lenders accounted for 61.6

percent of first-lien, owner-occupied, site-built home-purchase loans, slightly up from

61.1 percent in 2018. Non-DIs were also more likely than DIs to (1) originate

nonconventional loans, (2) originate loans to minority borrowers and low- or moderate-

income (LMI) borrowers, as well as for properties in LMI neighborhoods and (3) sell

originated loans instead of holding them.

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 7

2. HMDA data coverage of the

mortgage market

The HMDA data are the most comprehensive source of publicly available information on the

U.S. mortgage market, and the only publicly available source of nationwide application-level

data on mortgage credit. Given that mortgage debt is by far the largest component of household

debt, the data have been used extensively for research and supervisory work, as well as for

public policy deliberations related to the mortgage market.

Although the HMDA data are the most extensive application-level data on residential mortgage

lending in the U.S., they do not cover the entire mortgage market. Among depository

institutions (DI), the smallest institutions, institutions without any branches in a metropolitan

statistical area (MSA), and institutions that are not federally insured or regulated or do not

make loans insured by a Federal agency or intended for sale to Fannie Mae or Freddie Mac, do

not have to report HMDA data. The 2015 HMDA rule’s changes to institutional coverage criteria

for closed-end loans took effect in 2017 and raised the reporting threshold from one covered

origination to 25 covered originations for DIs.

9

This change thus further increased the number

of exempted DIs. Among nondepository institutions (non-DI), institutions that make few

mortgage originations and those that operate entirely outside of an MSA do not have to report

HMDA data.

10

To assess HMDA’s overall coverage of the mortgage market, the Bureau first estimates the

universe of mortgage lenders and the number of mortgage originations by all lenders regardless

9

For reporting of open-end LOCs, the 2015 HMDA rule established an institutional coverage threshold of

at least 100 open-end LOCs in each of the two preceding calendar years. See 80 FR 66128 (Oct. 28, 2015).

In a rule finalized in August 2017, the Bureau temporarily increased the open-end threshold to 500 open-

end LOCs for calendar years 2018 and 2019. For example, if an institution was over the 25 closed-end

loan threshold in both of the two preceding years, but under the 500 open-end LOC threshold in either of

the two preceding years, it would still have to report closed-end loans but not open-end LOCs. See 82 FR

43088 (Sep. 13, 2017).

10

This section describes HMDA coverage applicable at the time the data discussed here were reported.

For 2019 data, DIs with less than $46 million in assets or less than 25 covered, closed-end originations in

either of the last two years, and non-DIs with less than 25 covered, closed-end originations in either of the

last two years were not required to report closed-end data under HMDA. For additional details, see

Federal Financial Institutions Examination Council’s “A Guide to HMDA Reporting: Getting It Right!”

available at https://www.ffiec.gov/hmda/guide.htm.

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 8

of whether they are HMDA reporters or not.

11

The estimate uses data from the HMDA data, the

Bank/Thrift and Credit Union Call Reports, and other data sources. This analysis focuses solely

on closed-end mortgages.

For financial institutions that did not report HMDA data in a given year but reported relevant

mortgage activity to one of the alternative sources, the Bureau employed several different

estimation strategies. For example, for credit unions that did not report HMDA data, the agency

examined their year-to-date closed-end loan origination volumes reported at the end of the year

to Credit Union Call Reports. In doing so, the Bureau used only the categories of mortgage loans

under the Credit Union Call Reports that are the same as the transactional coverage

requirements governing the 2019 HMDA data.

12

For banks and thrifts that did not report under

HMDA, the Call Reports contain information only on the end-of-period balance of the

mortgages on their books, but not on the origination volumes within the reporting period. For

those institutions, the Bureau developed a set of econometric models, first estimating the

relationships between annual originations and the end-of-year balances using HMDA

reporters.

13

These models control for an array of institutional characteristics, such as assets,

institution type, number of employees, and number of branches in MSAs. The Bureau then

applied this estimated relation to the characteristics of non-HMDA reporters to estimate their

closed-end mortgage origination volumes.

14

Based on this analysis, the Bureau estimates that the share of institutions and originations

covered by HMDA remain largely constant from 2018 to 2019. In 2019, approximately 11,200

institutions originated at least one closed-end mortgage loan, with a total origination volume of

about 9.2 million loans. These estimates largely remain unchanged from 2018 when the Bureau

estimated 11,800 total institutions with an origination volume of 7.3 million loans.

11

Note for the discussion in this section, the Bureau defines the universe of mortgages in line with the

transactional coverage criteria under HMDA that is applicable at the time the 2019 HMDA data were

collected.

12

For instance, these estimates include mortgage loans regardless of lien status but do not include open-

end LOCs.

13

The Bureau assumes the dependent variable (the number of mortgage originations for each institution)

follows a Poisson distribution, and that the logarithm of its expected value can be modeled by a linear

combination of unknown parameters. In other words, the Bureau estimated Poisson regressions.

14

Alternatively, one might compare the number of loans reported under HMDA with the number of loans

reported in consumer credit files maintained by nationwide consumer reporting agencies (NCRAs).

However, there are several disadvantages in using NCRA data to estimate the total universe of mortgage

originations, including (1) a lag between the time when a mortgage is originated and when the

information on the mortgage tradeline is first reported to the credit bureaus (2) potential duplication and

transactional coverage issues, and (3) the estimates reported from NCRAs do not allow the breakdown of

the origination volumes by the origination entities.

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 9

The 2019 HMDA data contained closed-end data from a total of 5,496 institutions. Although this

is lower than the 5,666 institutions that reported in 2018, the percentage of total institutions

that reported under HMDA was similar in each year (49.1 percent in 2019 vs. 48.0 percent in

2018). In addition, HMDA reporters originated about 8.1 million loans or about 88 percent of

the estimated total number of closed-end originations in the U.S. In 2018, HMDA reporters

originated about 6.4 million loans or approximately 88 percent of the estimated number of

originations.

15

15

Calculations in the text are based on precise data values. Using rounded numbers from the printed

tables may lead to different values due to rounding error.

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 10

3. Mortgage applications and

originations

In 2019, a total of 5,508 financial institutions—banks, savings associations, credit unions, and

nondepository mortgage lenders—reported data on 15.1 million applications and 9.3 million

originations under HMDA. Beginning with data collected in 2018, the reporting of home equity

lines of credit (HELOCs) became mandatory rather than optional.

16

The number of HELOC

records decreased from 2.3 to 2.1 million between 2018 and 2019, and the number of HELOC

originations also declined from 1.1 to 1.0 million. Also beginning in 2018, financial institutions

were required to report a loan purpose other than purchase, home improvement, or refinance.

The number of records for the purpose other than purchase, home improvement, or refinance

decreased from 1.4 million in 2018 to 1.3 million in 2019.

To make the 2019 HMDA data as consistent as possible with historical data, the Bureau excludes

all HELOCs as well as records for a loan purpose other than purchase, home improvement, or

refinance. These exclusions reduce the number of HMDA reporters by 12 to 5,496.

17

Unless

specifically noted, the remainder of the article will focus on these 5,496 financial institutions to

facilitate comparability of HMDA data over time.

Table 1 presents the number of one-to-four-family properties applications and originations by

loan purpose (e.g., home purchase, home improvement, refinance) as well as the number of

multifamily applications and originations dating back to year 2004. The one-to-four family

originations are first disaggregated by lien status (e.g., first lien, junior lien) and occupancy

(e.g., owner-occupied, non-owner-occupied). Then, the first-lien, owner-occupied originations

are further disaggregated by property type (e.g., site-built, manufactured home) and by whether

it is a conventional loan or not.

18

Finally, the site-built, nonconventional originations are

disaggregated by nonconventional loan types (e.g., FHA-insured, VA-guaranteed, FSA/RHS).

16

HELOCs are defined as open-end LOCs except those that are reverse mortgages.

17

The 2015 HMDA rule change that eliminated reporting of unsecured home improvement loans was one

reporting change the Bureau was unable to make consistent over time. When applicable, results prior to

2018 include unsecured home improvement loans, while those beginning with 2018 do not.

18

Manufactured-home lending differs from lending for site-built homes. Furthermore, even among the

manufactured home loans, chattel-secured lending differs greatly from those that are not chattel secured.

Chattel-secured lending typically carries higher interest rates and shorter terms to maturity (for pricing

information on manufactured home loans, see Tables 8 and 9). This Data Point article focuses almost

entirely on site-built mortgage originations, which constitute most originations (as shown in Table 1).

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 11

Nonconventional loans are those with mortgage insurance or other guarantees from federal

government agencies, including the FHA, VA, and the U.S. Department of Agriculture’s

FSA/RHS. Conventional lending encompasses all other loans, including those held in banks’

portfolios, those sold to Government-Sponsored Enterprises (GSEs), such as Fannie Mae and

Freddie Mac, and those packaged into private-label securities. In general, nonconventional

loans have higher allowable loan-to-value (LTV) ratios—that is, borrowers provide relatively

smaller down payments relative to conventional loans.

The total number of originations reported under 2019 HMDA increased by approximately 2

million (26 percent), with the increase in refinance loans driving 80 percent of the increase.

Lenders reported approximately 8.1 million originations in 2019, up from 6.4 million

originations in 2018. In addition, lenders reported 12.6 million applications, which includes 2.9

million applications that the lenders closed as incomplete or the applicant withdrew before the

lender made a decision.

Refinance applications for one-to-four family properties increased from 3.8 million in 2018 to

5.9 million in 2019. Refinance originations also nearly doubled, by approximately 1.5 million

from 2018 to 2019. More detailed information on refinance loans available in the 2019 data

shows that less than half (41.1 percent) of refinance loans were cash-out refinances. This

contrasts with 2018 when cash-out refinance loans accounted for 56.3 percent of all refinance

loans.

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 12

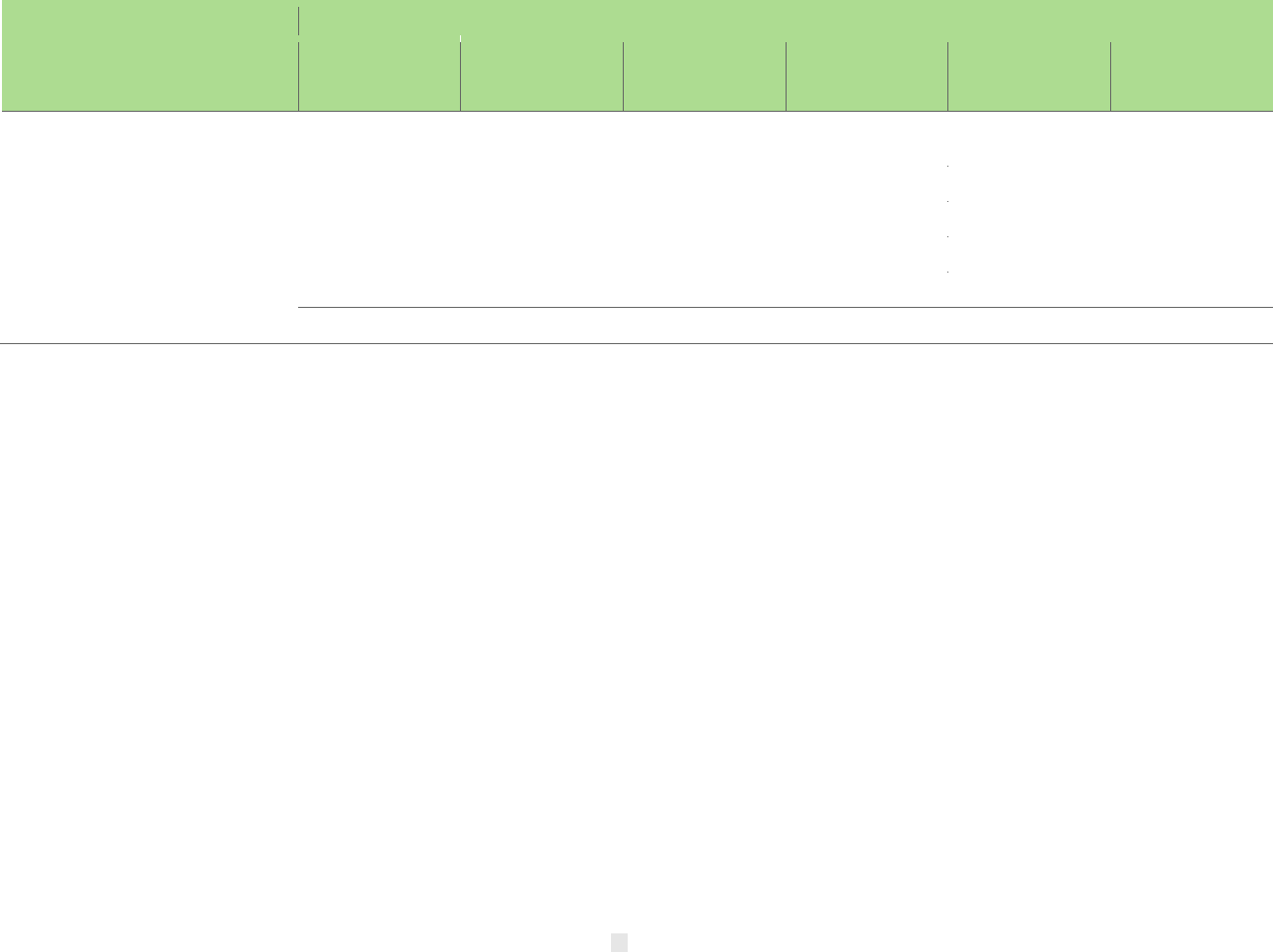

TABLE 1: APPLICATIONS AND ORIGINATIONS (IN THOUSANDS), SHARE OF ONE-TO-FOUR-FAMILY SITE-BUILT,

NONCONVENTIONAL LOAN ORIGINATIONS (PERCENT), AND PRE-APPROVALS AND LOAN PURCHASES (IN

THOUSANDS)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

1-4 FAMILY

Home purchase

Applications

(1)

9,804 11,685 10,929 7,609 5,060 4,217 3,848 3,650 4,023 4,586 4,679 5,196 5,694 6,036 6,069 6,284

Originations 6,437 7,391 6,740 4,663 3,139 2,793 2,547 2,430 2,742 3,139 3,248 3,676 4,046 4,251 4,262 4,436

First lien, owner occupied 4,789 4,964 4,429 3,454 2,628 2,455 2,219 2,073 2,343 2,703 2,815 3,210 3,544 3,699 3,707 3,853

Site-built, conventional 4,107 4,425 3,912 2,937 1,581 1,089 1,006 999 1,251 1,630 1,741 1,899 2,123 2,297 2,410 2,489

Site-built,

nonconventional

553 411 386 394 951 1,302 1,152 1,019 1,033 1,007 1,006 1,235 1,340 1,309 1,186 1,249

FHA share (%) 74.6 68.6 66.0 65.8 78.9 77.0 77.4 70.9 68.0 62.8 58.3 64.6 64.6 62.3 60.2 60.4

VA share (%) 21.6 26.7 29.0 27.1 15.2 13.9 15.2 18.2 19.9 24.2 28.3 26.0 26.9 28.7 31.2 31.8

FSA/RHS share (%) 3.9 4.7 5.0 7.1 5.9 9.0 7.4 10.9 12.0 13.1 13.3 9.4 8.5

9.1 8.6 7.9

Manufactured,

conventio

nal

106 100 101 95 68 43 45 40 44 51 51 56 59 67 80 83

Manufactured,

nonconventional

24 27 30 29 28 21 17 15 14 14 16 20 22 26 31 32

First lien, non-owner

occupied

857 1,053 880 607 412 292 285 314 355 388 378 406 435 472 470 481

Junior lien, owner

occupied

738 1,224 1,269 552 93 44 42 41 43 46 53 58 65 79 83 101

Junior lien, non-owner

occupied

53 150 162 50 6 2 2 1 1 1 2 2 2 2 2 2

Refinance

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 13

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Applications

(1)

16,085 15,907 14,046 11,566 7,805 9,983 8,437 7,422 10,526 8,564 4,526 5,957 7,187 4,949 3,832 5,927

Originations 7,591 7,107 6,091 4,818 3,491 5,772 4,971 4,330 6,668 5,141 2,370 3,234 3,759 2,523 1,941 3,447

First lien, owner occupied 6,497 5,770 4,469 3,659 2,934 5,301 4,519 3,856 5,930 4,393 2,001 2,847 3,375 2,207 1,662 3,116

Site-built, conventional 6,115 5,541 4,287 3,407 2,363 4,264 3,837 3,315 4,971 3,634 1,608 2,155 2,529 1,635 1,247 2,295

Site-built,

nonconventional

297 151 110 180 506 979 646 508 917 715 363 661 812 541 384 786

FHA share (%) 68.3 77.3 87.5 91.5 92.2 83.7 79.3 63.2 61.2 61.2 47.6 59.6 49.5 53.3 55.4 47.0

VA share (%) 31.4 22.4 12.3 8.3 7.6 15.9 20.3 35.9 37.8 37.6 51.9 40.2 50.1 46.0 44.3 52.7

FSA/RHS share (%) 0.2 0.3 0.2 0.1 0.2 0.4 0.4 0.9 0.9 1.2 0.5 0.3 0.4 0.8 0.3 0.3

Manufactured,

conventional

77

70 60 56 42 36 25 25 31 32 22 21 20 19 20 21

Manufactured,

nonconventional

7 8 12 16 22 22 10 9 11 12 8 10 14 13 10 14

First lien, non-owner

occupied

618 582 547 474 330 350 359 394 660 673 310 329 329 253 206 262

Junior lien, owner

occupied

464 729 1,036 661 219 115 88 74 73 70 55 55 52 60 69 67

Junior lien, non-owner

occupied

13 25 39 23 9 7 6 5 5 5 4 4 3 3 3 3

Home improvement

Applications 2,200 2,544 2,481 2,218 1,413 832 671 675 779 833 846 926 1,005 1,054 350 347

Originations 964 1,096 1,140 958 573 390 342 335 382 425 411 477 536 549 183 174

MULTIFAMILY

(1)

Applications 61 58 52 54 43 26 26 35 47 51 46 52 50 48 62 66

Originations 48 45 40 41 31 19 19 27 37 40 35 41 40 38 51 54

Total applications 28,151 30,193 27,508 21,448 14,320 15,057 12,981 11,782 15,375 14,034 10,097 12,132 13,937 12,086 10,314 12,624

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 14

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total originations 15,040 15,638 14,011 10,480 7,234 8,974 7,879 7,122 9,828 8,744 6,064 7,428 8,381 7,361 6,437 8,111

Memo

Purchased Loans 5,142 5,868 6,236 4,821 2,935 4,301 3,231 2,939 3,163 2,788 1,800 2,126 2,232 2,089 1,757 2,072

Requests for preapproval

(2)

1,068 1,260 1,175 1,065 735 559 440 429 474 474 496 531 514 485 467 445

Requests for preapproval

that were approved but not

acted on

167 166 189 197 99 61 53 55 64 69 64 63 60 36 75 74

Requests for preapproval

that were denied

171 231 222 235 177 155 117 130 149 123 125 115 115 107 102 77

NOTE: Components may not sum to totals because of rounding. Applications include those withdrawn and those closed for incompleteness. FHA is

Federal Housing Administration; VA is U.S. Department of Veterans Affairs; FSA is Farm Service Agency; RHS is Rural Housing Service.

(1) A multifamily property consists of five or more units.

(2) Consists of all requests for preapproval. Preapprovals are not related to a specific property and thus are distinct from applications.

SOURCE: Here and in subsequent tables and figures, except as noted, Federal Financial Institutions Examination Council, data reported under the Home

Mortgage Disclosure Act (www.ffiec.gov/hmda).

DATA POINT: 2019 MORTGAGE MARKET ACTIVITY AND TREND 15

FIGURE 1: NUMBER OF HOME-PURCHASE AND REFINANCE MORTGAGE

ORIGINATIONS, 1994-2019

The decrease in interest rates was likely a main driver behind the increase in refinance

applications and loans. Average interest rates declined throughout 2019 and were generally

lower in 2019 than 2018. The average rate on 30-year fixed rate conventional conforming

mortgage loans made to prime borrowers started at 4.5 percent at the beginning of 2019 and

decreased to 3.7 percent by the end of 2019.

19

In contrast, interest rates gradually increased

from 3.9 percent in the beginning of 2018 to 4.5 percent by the end of 2018. The reported

interest rates in HMDA data follow a consistent pattern. The median interest rate for 30-year

19

This measure comes from Freddie Mac’s Primary Mortgage Market Survey and is available from the

Federal Reserve Bank of St. Louis’ Federal Reserve Economic Database (FRED) at

https://fred.stlouisfed.org/series/MORTGAGE30US.

16

conventional loans for prime borrowers (with a credit score of at least 620) was 4.1 in 2019

HMDA data compared to 4.8 in 2018 HMDA data.

Home-purchase originations for one-to-four family properties increased from 4.3 million in

2018 to 4.4 million in 2019. This is a continuation of an upward trend dating back to 2011.

Figure 1 shows that, unlike the number of refinance loans, which has been volatile throughout

the observed period, the number of home purchase loans has been steadily increasing since

2011, reaching a similar level in 2019 as in 2007.

20

The historical fluctuations in the volume of

refinance loans compared with a steady increase in home-purchase loans in recent years

suggests that a decision to refinance is more responsive to the changes in interest rates than a

decision to purchase a home.

The volume of home improvement loans reported declined from 183,000 in 2018 to 174,000 in

2019. As noted above, this measure cannot be constructed consistently over time since all results

prior to 2018 included unsecured home improvement loans, but the results beginning in 2018

do not.

Most one-to-four family home-purchase loans were first liens for owner-occupied properties. In

2019, there were 3.9 million such originations, representing about 87 percent of home purchase

loans, which was unchanged from 2018. Although the share of first-lien originations for owner-

occupied properties did not change, there was some variation in the size of the increase across

different loan and property types. For example, among first-lien, owner-occupied, one-to-four-

family, home-purchase originations, the number of site-built, nonconventional originations

increased by 5.4 percent between 2018 and 2019. On the other hand, in this same subset of

home-purchase originations, the number of manufactured, nonconventional originations

increased by 2.5 percent.

Similar to home-purchase loans, most one-to-four-family refinance loans were first liens for

owner-occupied properties. The volume of these refinance loans increased significantly during

2019. There were 3.1 million first-lien, owner-occupied refinance originations in 2019, nearly

double the number in 2018. Furthermore, most of first-lien, owner-occupied refinance

originations were for conventional loans for site-built homes. In fact, the share of conventional

loans for site-built homes was larger among refinance loans (73.6 percent) than home-purchase

loans (64.6 percent).

Among first-lien, home-purchase loans for one-to-four-family, owner-occupied, site-built

properties, 33.4 percent were nonconventional loans, up slightly from 33 percent in 2018 but

20

The HMDA data prior to 2004 did not provide lien status for loans, and thus the number of loans prior

to 2004 in Figure 1 include both first- and junior-lien loans.

17

down from a peak of approximately 54 percent in 2009. Figure 2 shows that the change in the

nonconventional share of loans is mostly driven by change in the share of FHA loans. Unlike the

FHA share of loans, the VA and FSA/RHS shares make up a small and stable proportion of

nonconventional loans.

FIGURE 2: NONCONVENTIONAL SHARE OF HOME-PURCHASE MORTGAGE

ORIGINATIONS, 1994-2019

In addition to loan applications and originations, the HMDA data also include preapproval

requests for home-purchase loans. As shown in Table 1, lenders reported approximately

445,000 preapproval requests, which is down slightly by less than 5 percent from 2018. About

17 percent of these requests were denied. Approximately 17 percent of them were requests that

lenders had approved but the applicants did not take any further action.

Finally, HMDA data include information on loans purchased by reporting institutions during

the reporting year, although the purchased loans may have been originated before 2019. Table 1

shows that lenders purchased 2.1 million loans from other institutions in 2019, an 18 percent

increase from 2018.

18

4. Mortgage outcomes by

demographic groups

The HMDA data are a key resource for policymakers and the public to understand the

distribution of mortgage credit across demographic groups. Tables 2 through 8 provide

information on loan shares, product usage, denials, and certain mortgage pricing information

for groups defined by applicant income, neighborhood income, and applicant race and ethnicity.

Tables 2 through 7 focus on first-lien home purchase and refinance loans for one-to-four-family,

owner-occupied, site-built properties, which accounted for approximately 82 percent of all

HMDA originations excluding purchased loans in 2019. Table 8, in contrast, also includes loans

for manufactured homes.

4.1 Distribution of home loans across

demographic groups

One of the 2015 HMDA rule changes to historical HMDA data points altered reporting

requirements for race and ethnicity. Beginning in 2018, mortgage applicants now have the

option of providing disaggregated information for the Asian, Pacific Islander, and Native

American race categories and for the Hispanic ethnicity category. Of the total of 17.5 million

records in the 2019 HMDA data, including open-end LOCs, about 1.6 million records (8.9

percent) included at least one disaggregated racial or ethnic category. Even though the number

of records reporting at least one disaggregated racial or ethnic category increased from 1.3

million (10 percent) in 2018, because of an increase in the total number of records, the share has

decreased from 2018 to 2019. Asian Indian was the most commonly reported disaggregated race

at 1.2 percent and Mexican was the most commonly reported disaggregated ethnicity at 2.7

percent.

To make the 2019 results consistent with and comparable to results from years prior to 2018,

this Data Point article aggregates all disaggregated race and ethnicity data to their

corresponding aggregate category. As an example, if an applicant reported being Chinese, that

applicant is aggregated into the Asian category. The 2015 HMDA rule also increased the number

of ethnicities primary applicants and co-applicants can provide from one each to five each. To

convert the new set of five ethnicity fields for the primary applicant back into one ethnicity field,

the Bureau uses values from just the first ethnicity data field as in the past years, unless the first

field contains a missing value. When the first ethnicity data field is missing, the Bureau replaces

19

that missing value using the remaining four data fields. A similar process is used for co-

applicants. The footnotes to Table 2 summarize how applicants were classified into racial and

ethnic categories.

21

Table 2 presents different groups’ shares of one-to-four-family, owner-occupied, site-built home

purchase and refinance loans and how these shares have changed over time. Continuing the

historical trend, the share of home-purchase loans for Black borrowers increased from 2018 to

2019, whereas those for non-Hispanic White borrowers decreased. The Black borrowers’ share

of home-purchase loans increased from 6.7 percent in 2018 to 7.0 percent, which was the sixth

consecutive year of an increase. For non-Hispanic White borrowers, their share of home-

purchase loans was 60.3 percent in 2019, down from 62.0 percent in 2018. This drop continues

a downward trend that began in 2013 when non-Hispanic White borrowers’ share of home

purchase loans was 70.2 percent.

The share of refinance loans decreased for all racial groups except Asian borrowers. For

example, the non-Hispanic White borrowers’ share of refinance loans declined from 63.3

percent in 2018 to 61.0 percent in 2019. The share for Black and Hispanic White borrowers

declined more modestly than non-Hispanic White borrowers. The share of refinance loans for

Black borrowers declined from 6.2 percent to 5.3 percent, while that for Hispanic White

borrowers declined from 6.8 percent to 6.2 percent. In contrast, the share for Asian borrowers

increased from 3.7 percent in 2018 to 5.4 percent in 2019.

21

The application is designated as “joint” if one applicant was reported as White and the other was

reported as one or more minority races or if the application is designated as White with one Hispanic

applicant and one non-Hispanic applicant.

20

TABLE 2: DISTRIBUTION OF HOME-PURCHASE AND REFINANCE LOANS, BY BORROWER AND NEIGHBORHOOD

CHARACTERISTICS, 2004-2019 (PERCENT EXCEPT AS NOTED)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

A. Home Purchase

Borrower race and

ethnicity

(1)

Asian 4.8 5.0 4.5 4.5 4.9 5.3 5.5 5.2 5.3 5.7 5.4 5.3 5.5 5.8 5.9 5.7

Black or African American 7.1 7.7 8.7 7.6 6.3 5.7 6.0 5.5 5.1 4.8 5.2 5.5 6.0 6.4 6.7 7.0

Hispanic white 7.6 10.5 11.7 9.0 7.9 8.0 8.1 8.3 7.7 7.3 7.9 8.3 8.8 8.8 8.9 9.2

Non-Hispanic white 57.1 61.7 61.2 65.4 67.5 67.9 67.6 68.7 70.0 70.2 69.1 68.1 66.4 64.9 62.0 60.3

Other minority

(2)

1.4 1.3 1.1 1.0 0.9 0.9 0.9 0.8 0.8 0.7 0.8 0.8 0.8 0.9 0.8 0.8

Joint 2.3 2.3 2.3 2.5 2.8 2.8 2.7 2.8 2.9 3.1 3.4 3.5 3.6 3.7 3.6 3.7

Missing 19.8 11.5 10.5 10.1 9.6 9.3 9.1 8.6 8.2 8.2 8.3 8.5 8.9 9.6 12.0 13.3

All 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Borrower income

(3)

Low or moderate 27.7 24.6 23.6 24.6 28.0 36.6 35.4 34.4 33.3 28.5 27.0 27.9 26.2 26.3 28.1 28.6

Middle 26.9 25.7 24.7 25.1 27.0 26.6 25.6 25.2 25.1 25.2 25.6 26.1 26.4 26.7 26.7 27.1

High 41.4 45.5 46.7 46.9 42.9 34.6 37.3 38.8 40.0 44.7 46.1 44.9 46.4 46.0 44.3 43.1

Income not used or not

applicable

4.0 4.2 5.0 3.4 2.1 2.2 1.7 1.6 1.5 1.6 1.3 1.1 1.0 1.0 0.9 1.2

All 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Neighborhood income

(4)

Low or moderate 14.5 15.1 15.7 14.4 13.2 12.6 12.1 11.0 12.8 12.7 13.3 13.5 14.1 16.1 17.0 16.5

Middle 48.7 49.2 49.5 49.6 49.8 50.2 49.5 49.4 43.6 43.7 44.6 45.2 45.8 44.2 44.2 44.3

High 35.8 34.7 33.7 35.1 35.9 35.8 37.7 39.1 43.2 43.2 41.8 41.0 40.0 39.6 38.8 38.9

21

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

All 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

B. Refinance

Borrower race and

ethnicity

(1)

Asian 3.5 2.9 3.0 3.1 3.1 4.1 5.2 5.4 5.5 4.7 4.3 5.0 5.5 4.0 3.7 5.4

Black or African American 7.4 8.3 9.6 8.4 6.0 3.5 2.9 3.1 3.3 4.4 5.4 5.0 5.0 5.9 6.2 5.3

Hispanic white 6.2 8.6 10.1 8.7 5.3 3.2 3.0 3.3 3.9 5.0 6.2 6.3 6.2 6.8 6.8 6.2

Non-Hispanic white 57.2 60.9 59.6 62.7 70.7 74.6 74.3 73.5 72.5 70.5 67.8 67.2 65.2 63.2 63.3 61.0

Other minority

(2)

1.4 1.4 1.3 1.1 0.8 0.6 0.5 0.6 0.6 0.7 0.9 0.8 0.9 1.0 0.9 0.8

Joint 2.1 2.1 1.9 2.0 2.2 2.6 2.7 2.8 3.1 3.1 3.2 3.3 3.4 3.3 2.9 3.3

Missing 22.1 15.7 14.6 14.1 11.9 11.4 11.4 11.3 11.1 11.6 12.2 12.4 13.8 15.8 16.2 17.9

All 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Borrower income

(3)

Low or moderate 26.2 25.5 24.7 23.3 23.4 19.6 18.9 19.2 19.6 21.1 22.1 19.0 16.9 22.9 30.0 23.8

Middle 26.3 26.8 26.1 25.5 25.4 22.4 22.5 21.3 21.8 21.7 21.9 21.0 20.3 23.4 24.9 21.9

High 38.8 40.8 43.7 46.0 44.6 45.6 49.5 48.1 47.6 46.3 44.9 45.2 47.5 44.0 41.0 43.1

Income not used or not

applicable

8.7 6.9 5.5 5.2 6.6 12.4 9.1 11.4 10.9 11.0 11.1 14.8 15.3 9.7 4.1 11.2

All 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Neighborhood income

(4)

Low or moderate 15.3 16.5 17.9 16.1 11.9 7.8 7.2 7.4 10.1 12.1 13.3 12.3 12.0 15.5 16.8 14.0

Middle 50.0 51.3 52.0 52.2 51.9 47.5 46.1 46.1 41.9 43.7 45.3 43.8 43.4 44.6 45.6 43.0

High 33.9 31.6 29.4 31.0 35.2 43.5 46.0 46.0 47.6 43.9 41.3 43.7 44.4 39.7 37.6 42.7

All 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

22

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Memo

Number of home-purchase

loans (thousands)

4,660 4,836 4,298 3,331 2,533 2,391 2,157 2,018 2,284 2,638 2,747 3,134 3,463 3,606 3,596 3,738

Number of refinance loans

(thousands)

6,412 5,692 4,397 3,588 2,869 5,243 4,483 3,823 5,888 4,349 1,971 2,816 3,341 2,176 1,631 3,081

NOTE: First-lien mortgages for one- to four-family, owner-occupied, site-built homes. Rows may not sum to 100 because of rounding or, for the distribution

by neighborhood income, because property location is missing.

(1) Applications are placed in one category for race and ethnicity. The application is designated as joint if one applicant was reported as white and the other

was reported as one or more minority races or if the application is designated as white with one Hispanic applicant and one non-Hispanic applicant. If there

are two applicants and each reports a different minority race, the application is designated as two or more minority races. If an applicant reports two races

and one is white, that applicant is categorized under the minority race. Otherwise, the applicant is categorized under the first race reported. "Missing" refers

to applications in which the race of the applicant(s) has not been reported or is not applicable or the application is categorized as white but ethnicity has not

been reported.

(2) Consists of applications by American Indians or Alaska Natives, Native Hawaiians or other Pacific Islanders, and borrowers reporting two or more

minority races.

(3) The categories for the borrower-income group are as follows: Low-

or

moderate-income (or LMI) borrowers have income that is less than 80 percent of

estimated current area median family income (AMFI), middle-income borrowers have income that is at least 80 percent and less than 120 percent of AMFI,

and high-income borrowers have income that is at least 120 percent of AMFI.

(4) The categories for the neighborhood-income group are based on the ratio of census-tract median family income to area median family income from the

2006-10 American Community Survey data for 2012-2019 and from the 2000 census for 2004-11, and the three categories have the same cutoffs as the

borrower-income groups (see note 3).

23

The shares of home purchase and refinance loans exhibit opposite trends for low- or moderate-

income (LMI) borrowers compared with high-income borrowers.

22

The LMI borrower share of

home-purchase loans increased from 28.1 percent to 28.6 percent, whereas high-income

borrowers’ share decreased from 44.3 percent to 43.1 percent. The LMI borrower share of

refinance loans decreased from 30.0 percent to 23.8 percent, while high-income borrowers’ share

increased from 41.0 percent to 43.1 percent.

The trends in shares of LMI and high-income neighborhoods mirror those of the borrowers for

refinance loans but not for home purchase loans.

23

The LMI neighborhoods’ share of refinance

loans decreased slightly, whereas high-income neighborhoods’ share of refinance loans increased.

On the other hand, the share of home purchase loans in LMI neighborhoods declined slightly,

while the share in high-income neighborhoods increased slightly between 2018 and 2019.

Even though the share of refinance loans for most racial/ethnic groups, LMI borrowers, and LMI

neighborhoods has decreased, because of the increase in the total number of refinance loans, the

number of refinance loans has increased for all groups between 2018 and 2019.

24

For example, the

share of refinance loans for Blacks decreased from 6.2 percent to 5.3 percent but the number

increased by about 63,000. The increase in the number of refinance loans was especially large for

non-Hispanic White borrowers, Asian borrowers, high-income borrowers, and high-income

neighborhoods.

In examining historical trends based on a borrower or neighborhood income, changes in

underlying estimates may impact income categories. First, in 2012 and 2017, the Federal Financial

Institutions Examination Council (FFIEC) revised the census-tract median family income

22

In accordance with the definitions used by the federal bank supervisory agencies to enforce the

Community Reinvestment Act, LMI borrowers are defined as those with incomes less than 80 percent of the

estimated current area median family income (AMFI). Middle-income borrowers have incomes of at least

80 percent and less than 120 percent of AMFI, and high-income borrowers have incomes of at least 120

percent of AMFI. AMFI is estimated based on the incomes of residents of the metropolitan area or

nonmetropolitan portion of the state in which the loan-securing property is located. For AMFI estimates,

see Federal Financial Institutions Examination Council (2019), “FFIEC Median Family Income Report,”

available at https://www.ffiec.gov/Medianincome.htm.

23

Definitions for LMI, middle-income, and high-income neighborhoods are identical to those for LMI,

middle-income, and high-income borrowers, but are based on the ratio of census-tract median family

income to AMFI measured from the census data.

24

The bottom of Table 2 provides the total loan counts for each year, and thus the number of loans to a

given group in a given year can be easily computed. For example, the number of home-purchase loans to

Asians in 2019 was approximately 213,000, calculated by multiplying 3.7 million loans by 5.7 percent.

24

estimates that accompany the public HMDA data (and that are used for this Data Point article).

25

Therefore, in Table 2 and all subsequent tables that use neighborhood income categories, the

underlying neighborhood income data used to generate the results for 2017 and later are different

from the data used for 2016 and earlier. Similarly, neighborhood income data used for the results

from 2012 through 2016 are different than those used from 2011 and earlier. Second, the tract

demographic measures for 2017 and later are based on the 2015 American Community Survey

(ACS) five-year estimates, whereas the 2012–2016 data relied on the 2010 ACS five-year

estimates, and the 2004–2011 data relied on the 2000 Census data. Lastly, the Office of

Management and Budget (OMB) updates metropolitan area delineations over time. In short,

income and demographic data can be compared across ACS datasets, and also between ACS and

the 2000 Census data.

26

However, given the changes in geographic delineations over time, some

caution should be exercised in comparing relative income measurements over time.

25

For details on the changes of census information used in this Data Point article, see FFIEC’s “Changes for

Current Census File,” at https://www.ffiec.gov/census/htm/2015CensusInfoSheet.htm

26

See https://www.census.gov/programs-surveys/acs/guidance/comparing-acs-data.html for more details.

25

4.2 Average loan size by demographic group

The average size of loan amount differs substantially by race and ethnicity. Table 3 shows the

average size of home purchase and refinance loans for different groups over time.

27

In 2019,

Asian borrowers continued to take out loans with the largest loan amount, averaging

approximately $412,000 for home purchases and $450,000 for refinance loans. On the other

hand, Black borrowers continued to take out loans with the smallest loan amount, averaging

approximately $243,000 for home purchases and $250,000 for refinance loans.

The average home-purchase loan amounts have followed historical trends in home prices, rising

during the mid-2000s, falling sharply through 2008 and 2009, and then beginning to rise again

since about 2010.

28

The average home-purchase loan amounts returned to pre-crisis levels (in

nominal terms) by 2014 for Asians and Blacks, and by 2013 for non-Hispanic Whites.

29

Hispanic

White borrowers were the last racial/ethnic group to have home-purchase loan amount surpass

the pre-crisis level in 2019. The average value of home-purchase loans to Hispanic White

borrowers was $249,000 in 2019, which surpasses the pre-Recession peak of $238,000 in 2006.

The average loan amount for refinancing has risen since 2013 and increased significantly more

than home-purchase loans between 2018 and 2019. The year-over-year increase in the average

loan amount for refinancing was 23.4 percent compared with 4.2 percent for home-purchase

loans. The largest increase in the average refinance loan amount occurred for LMI borrowers

and LMI neighborhoods.

27

All dollar amounts are reported in nominal terms.

28

The Federal Housing Finance Agency’s (FHFA’s) quarterly Purchase-Only House Price Index

(seasonally adjusted) increased each quarter during 2019 and was up 5.1 percent for the year. The housing

price increases seen at the national level varied considerably across geography ranging from a slight 3

percent increase in North Dakota to 12 percent increases in Idaho (seasonally adjusted, year-over-year

comparison). All of these data are available from FHFA at

https://www.fhfa.gov/DataTools/Downloads/Pages/House-Price-Index-Datasets.aspx.

29

Beginning in 2018, HMDA reporters were required to report the loan amount to the dollar instead of

rounded to the thousands, which might affect comparability of averages over time.

26

TABLE 3: AVERAGE VALUE OF HOME-PURCHASE AND REFINANCE LOANS, BY BORROWER AND NEIGHBORHOOD

CHARACTERISTICS, 2004-2019 (THOUSANDS OF DOLLARS, NOMINAL, EXCEPT AS NOTED)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

A. Home Purchase

Borrower race and

ethnicity

(1)

Asian 280 316 326 334 299 276 293 291 304 328 344 360 373 390 406 412

Black or African American 166 183 197 197 184 172 174 174 179 193 199 209 217 224 232 243

Hispanic white 189 224 238 220 186 168 168 168 176 190 198 209 220 230 237 249

Non-Hispanic white 193 211 216 222 209 195 204 204 213 226 231 239 246 254 261 273

Other minority

(2)

206 240 257 245 216 196 201 198 206 219 229 241 249 256 259 266

Joint 233 255 261 269 255 248 263 261 274 289 293 302 311 321 332 347

Missing 216 248 261 280 265 242 256 262 279 298 293 303 308 317 313 324

Borrower income

(3)

Low or moderate 114 116 117 124 128 129 128 125 131 132 132 141 146 152 163 174

Middle 165 170 170 176 182 187 189 184 192 194 193 204 209 217 228 242

High 281 306 313 317 298 291 303 302 313 323 328 341 345 359 371 386

Income not used or not

applicable

208 235 254 257 211 189 204 221 231 258 275 292 312 333 366 356

Neighborhood income

(4)

Low or moderate 159 180 189 188 175 160 164 163 158 171 178 188 199 204 213 221

Middle 172 190 197 196 186 174 177 173 178 191 196 206 216 224 233 244

High 258 284 294 301 277 257 270 271 282 300 306 316 324 340 349 360

Memo

27

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

All home-purchase loans 201 221 228 232 217 202 210 210 221 235 240 249 257 267 274 286

Conventional jumbo loans

(percent of originations)

(5)

11.2 12.7 9.4 6.8 2.3 1.3 1.7 2.2 3.0 4.0 4.8 5.3 5.2 5.5 5.2 4.8

Conventional jumbo loans

(percent of loaned dollars)

(5)

29.4 32.5 26.8 21.8 10.1 6.2 7.5 9.5 12.0 14.6 16.5 17.3 16.9 17.6 16.9 15.5

B. Refinance

Borrower race and

ethnicity

(1)

Asian 274 325 370 368 321 298 313 309 308 304 341 363 368 368 376 450

Black or African American 151 180 199 192 173 184 180 174 181 171 174 199 212 213 209 250

Hispanic white 178 219 252 244 193 190 191 183 190 180 190 214 228 223 227 272

Non-Hispanic white 180 205 221 222 205 209 210 208 212 206 216 239 251 238 237 289

Other minority

(2)

190 229 269 258 211 217 218 207 213 201 213 240 252 245 240 285

Joint 210 246 265 262 243 247 254 249 254 249 266 292 304 290 295 354

Missing 194 226 246 250 242 243 248 253 253 244 245 268 277 259 262 320

Borrower income

(3)

Low or moderate 114 124 124 126 129 138 133 128 135 128 123 136 143 143 154 192

Middle 162 181 183 181 180 185 180 174 182 171 174 193 202 200 208 244

High 256 294 320 312 276 268 274 281 277 276 301 324 330 329 335 395

Income not used or not

applicable

150 178 240 236 192 203 202 185 211 193 198 229 243 225 236 296

Neighborhood income

(4)

Low or moderate 142 169 188 185 164 173 173 167 163 153 157 182 196 185 187 232

Middle 158 184 201 198 182 184 182 175 181 173 180 201 214 204 205 251

High 245 282 313 311 272 259 265 269 269 270 290 311 321 316 320 377

28

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Memo

All refinance loans 185 212 232 231 212 216 220 218 221 213 222 247 259 246 245 302

Conventional jumbo loans

(percent of originations)

(5)

9.2 11.4 10.2 7.5 2.0 0.9 1.6 2.4 2.2 3.0 4.2 4.9 4.6 4.3 4.0 4.8

Conventional jumbo loans

(percent of loaned dollars)

(5)

25.8 29.6 28.3 23.0 9.0 4.1 6.9 10.7 9.2 12.7 16.5 16.8 15.7 16.4 15.3 16.3

NOTE: First-lien mortgages for one- to four-family, owner-occupied, site-built homes.

(1) See table 2, note 1.

(2) See table 2, note 2.

(3) See table 2, note 3.

(4) See table 2, note 4.

(5) Fraction of loans that are conventional and have loan amounts in excess of the single-family conforming loan-size limits for eligibility for purchase by

the government-sponsored enterprises.

29

4.3 Jumbo lending

A loan qualifies as jumbo if the loan amount is above the GSEs’ conforming loan-size limit for a

single-family home for that year and location. The conforming loan-size limit was mostly

uniform across the nation prior to 2008. The limits in Alaska, Hawaii, the U.S. Virgin Islands,

and Guam were 50 percent higher than in the nation at large. For the years 2008 and thereafter,

designated higher-cost areas had elevated limits. For 2019, the conforming loan-size limit was

$484,350 with the maximum limit of $726,525 for higher-cost areas.

As shown in Table 3, conventional jumbo loans—those with loan amounts greater than the

GSEs’ conforming loan limits and with no other government guarantee—made up 4.8 percent of

all first-lien home-purchase loans for owner-occupied, one-to-four-family, site-built homes in

2019, a slight decrease from 2018.

30

Among refinance loans, the share of conventional jumbo

loans increased to 4.8 percent in 2019 from 4.0 percent in 2018. Because of their larger size,

conventional jumbo loans made up a correspondingly larger share of the dollar volume of

mortgages, accounting for 15.5 percent of home-purchase loans and 16.3 percent of refinance

loans in 2019.

30

Beginning with 2018 data, two main issues with pre-2018 jumbo loans have been resolved. First,

conforming loan-size limits increase with the number of units that make up the property, but prior to

2018 the HMDA data did not have information on the number of units. Therefore, some loans could have

been misclassified as jumbo despite being eligible for purchase by a GSE. This is not an issue for data

from 2018 and later, since institutions reported the exact number of property units. A second issue prior

to 2018 was that HMDA’s implementing rules required lenders to report the loan amounts rounded to the

nearest thousands. However, the conforming loan limits published by FHFA may be set in hundreds of

dollars. Prior to 2018, FHFA conforming loan limits were rounded to the nearest thousands to match with

the HMDA reporting requirement. This is not an issue for 2018 and later years, since loan amount was

reported to the dollar (Publicly released loan amounts are rounded to the mid-point of ten-thousand-

dollar ranges to protect applicant and borrower privacy). Moreover, to make the identification of jumbo

loans easier, the Bureau has included a conforming loan flag in the release of the public HMDA Aggregate

LAR since 2018.

30

4.4 Variation across demographic groups in

nonconventional loan use

Historically, nonconventional loans (FHA, VA, RHS, and FSA) provide access to credit to those

who may otherwise have had limited access to mortgage credit. One advantage of

nonconventional loans is the relatively low down-payment requirement of as little as 3.5 percent

for FHA and VA lending programs, which serve the needs of borrowers who have few assets to

meet down-payment and closing-cost requirements. FHA-insured and VA-guaranteed programs

also provide credit access to borrowers who have low credit scores or high debt-to-income (DTI)

ratios and cannot obtain conventional loans.

31

Table 4 shows the share of nonconventional home

purchase and refinance loans by race/ethnicity, borrower’s income, and neighborhood income

groups.

Black and Hispanic White borrowers were more likely than other racial and ethnic groups to

take out nonconventional home-purchase loans.

32

In 2019, among those obtaining a first-lien,

owner-occupied, site-built, one-to-four-family home purchase mortgage, 60.6 percent of Blacks

and 48.8 percent of Hispanic Whites took out a nonconventional loan, whereas 29.7 percent of

non-Hispanic Whites and just 12.4 percent of Asians did so.

LMI borrowers and loans for properties in LMI neighborhoods were also more likely to use

nonconventional home-purchase loans. About 42 percent of both LMI home-purchase

borrowers and of applicants borrowing to purchase homes in LMI neighborhoods used

nonconventional loans, compared with 23.5 percent of high-income borrowers and 24.6 percent

of borrowers purchasing homes in high-income neighborhoods.

The use of nonconventional loans for home-purchase has declined since 2009 but remained

largely unchanged for all racial/ethnic groups from 2018 to 2019, except for Asian borrowers.

The share of Asian borrowers using nonconventional home-purchase loans increased by 5.6

percent between 2018 and 2019. Despite the increase, the share of Asian borrowers using

31

Sections 6.4.2 and 6.6 of last year’s second CFPB HMDA Data Point article explores this in more detail.

See “Introducing New and Revised Data Points in HMDA: Initial Observation from New and Revised Data

Points in 2018 HMDA,” available at https://files.consumerfinance.gov/f/documents/cfpb_new-revised-

data-points-in-hmda_report.pdf.

32

Findings of the Federal Reserve Board’s Survey of Consumer Finances for 2017 indicate that income,

liquid asset levels, and financial wealth holdings for minorities and lower-income groups are substantially

smaller than they are for non-Hispanic White borrowers or higher-income populations, and the long-

standing and substantial wealth disparities between families of different racial and ethnic groups have

changed little in the past few years. See Board of Governors of the Federal Reserve System, “Recent

Trends in Wealth-Holding by Race and Ethnicity: Evidence from the Survey of Consumer Finances,”

available at https://www.federalreserve.gov/econres/notes/feds-notes/recent-trends-in-wealth-holding-

by-race-and-ethnicity-evidence-from-the-survey-of-consumer-finances-20170927.htm.

31

nonconventional home-purchase loans remained below its peak of 26.6 percent in 2010 and far

below other racial/ethnic groups.

The shares of nonconventional home-purchase loans across borrower and neighborhood

incomes mostly increased between 2018 and 2019. The share of nonconventional home-

purchase loans largely remained unchanged for LMI borrowers, whereas the share for middle-

and high-income borrowers increased slightly between 2018 and 2019.

As was the case for home-purchase loans, Black borrowers and lower-income borrowers were

each more likely than borrowers in other groups to refinance through a nonconventional loan.

However, the differences were not as stark as for home-purchase loans. Overall, the share of

borrowers using nonconventional loans for refinancing was lower than that for home purchases.

The share of borrowers using nonconventional loans for refinancing was at its lowest in 2006,

increased substantially between 2006 and 2009, and has been fluctuating ever since. For

example, the share of Black borrowers using nonconventional loans for refinancing has

fluctuated between its lowest in 2013 at 37.1 percent and its highest in 2016 at 53.0 percent.

Similarly, the share for LMI borrowers has fluctuated between 9.3 percent in 2012 and 32.3

percent in 2019.

33

33

The reported nonconventional share of refinance loans likely underestimates the actual share for the

groups categorized by borrower income because, for most nonconventional refinance loans, income was

not reported. Thus, when income was reported on a refinance loan, the loan is likely to be conventional.

32

TABLE 4: NONCONVENTIONAL SHARE OF HOME-PURCHASE AND REFINANCE LOANS, BY BORROWER AND

NEIGHBORHOOD CHARACTERISTICS, 2004-2019 (PERCENT)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

A. Home Purchase

Borrower race and

ethnicity

(1)

Asian 2.9 1.8 2.1 2.6 13.4 26.1 26.6 25.8 21.9 16.1 14.7 16.6 15.6 13.4 11.8 12.4

Black or African American 21.7 14.3 13.6 21.7 64.1 82.0 82.9 80.3 77.2 70.8 68.0 70.2 68.5 64.9 60.6 60.6

Hispanic white 13.7 7.5 7.0 12.4 51.4 75.4 77.0 74.1 70.7 63.1 59.6 62.7 59.8 55.5 48.8 48.8

Non-Hispanic white 11.1 8.9 9.5 11.5 35.4 52.0 50.3 47.4 42.2 35.5 33.4 36.0 35.2 33.1 29.7 29.7

Other minority

(2)

14.0 9.3 9.4 14.8 48.4 67.6 68.8 65.9 62.2 55.5 54.0 55.3 54.2 52.1 49.3 50.1

Joint 16.9 12.8 14.4 17.2 46.4 59.4 56.3 53.6 48.9 42.1 41.3 43.8 43.1 40.9 37.3 37.1

Missing 11.3 5.1 5.7 8.8 32.7 50.6 49.4 45.9 39.4 31.9 32.2 34.9 34.7 31.9 31.0 32.5

Borrower income

(3)

Low or moderate 20.3 15.2 14.9 16.0 46.1 65.3 66.6 64.5 59.7 52.5 50.3 53.4 51.7 47.5 41.6 41.5

Middle 14.3 11.0 12.6 16.7 46.1 60.4 59.3 57.0 51.5 45.6 44.8 47.7 47.6 45.1 40.8 41.5

High 5.3 3.9 4.9 7.5 26.7 38.5 37.2 34.4 29.5 25.1 24.2 26.3 26.7 25.2 23.2 23.5

Neighborhood income

(4)

Low or moderate 15.8 9.7 9.6 13.8 45.4 64.3 65.0 61.2 57.9 49.9 48.1 50.4 48.8 46.2 41.4 42.0

Middle 14.1 10.2 10.8 14.2 42.7 59.8 59.4 56.9 52.1 44.7 43.1 45.6 44.6 41.7 37.8 38.1

High 7.1 5.4 6.1 7.6 27.4 43.4 42.0 39.5 34.6 28.2 26.1 29.0 28.4 26.3 23.8 24.6

Memo: All borrowers 11.9 8.5 9.0 11.8 37.6 54.4 53.4 50.5 45.2 38.2 36.6 39.4 38.7 36.3 33.0 33.4

33

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

B. Refinance

Borrower race and

ethnicity

(1)

Asian 1.2 0.7 0.6 1.0 4.6 5.7 4.7 4.3 5.9 6.7 6.8 9.8 8.3 10.2 11.0 9.1

Black or African American 11.1 5.8 4.4 10.2 39.2 53.8 42.0 37.8 38.6 37.1 39.1 49.4 53.0 47.0 43.1 52.5

Hispanic white 5.6 2.6 1.9 3.9 20.5 36.2 28.2 22.9 26.9 25.8 21.2 32.1 30.5 26.4 23.3 29.5

Non-Hispanic white 4.0 2.4 2.6 4.9 15.9 16.8 13.6 12.2 14.2 14.8 16.3 21.0 21.7 22.3 21.5 22.6

Other minority

(2)

5.5 3.4 2.4 4.9 20.0 28.3 23.3 21.9 25.5 24.9 25.0 32.6 36.7 33.7 33.1 38.7

Joint 7.5 3.7 3.4 6.2 19.5 21.1 16.6 16.3 20.1 20.5 25.5 28.0 29.3 29.6 28.5 30.7

Missing 4.2 1.9 1.7 4.1 18.7 19.0 12.5 13.6 16.5 16.7 21.5 25.5 27.7 28.3 25.7 29.5

Borrower income

(3)

Low or moderate 2.3 1.6 2.9 5.7 18.3 16.6 14.1 11.5 9.3 9.3 13.0 16.5 18.4 23.5 28.2 32.3

Middle 1.7 1.3 2.7 6.2 19.6 13.2 12.3 10.9 8.9 9.5 13.2 14.8 15.3 21.4 23.5 17.3

High 0.8 0.6 1.1 2.7 10.6 7.2 6.8 6.3 5.5 6.1 8.8 9.2 9.2 14.2 16.4 10.2

Neighborhood income

(4)

Low or moderate 5.9 3.2 2.9 6.3 24.6 31.2 23.1 19.7 22.2 22.1 22.4 29.5 30.4 30.4 28.1 32.1

Middle 5.2 3.0 2.9 5.8 20.2 22.3 17.5 16.1 18.4 19.0 20.9 26.8 28.2 27.8 26.1 29.2

High 2.9 1.7 1.6 3.0 11.3 12.1 10.0 9.3 11.7 12.4 14.5 18.5 19.0 19.4 18.4 19.8

Memo: All borrowers 4.6 2.6 2.5 5.0 17.6 18.7 14.4 13.3 15.6 16.4 18.4 23.5 24.3 24.9 23.5 25.5

NOTE: First-lien mortgages for one- to four-family, owner-occupied, site-built homes. Excludes applications where no credit decision was made.

Nonconventional loans are those insured by the Federal Housing Administration or backed by guarantees from the U.S. Department of Veterans Affairs,

the Farm Service Agency, or the Rural Housing Service.

(1) See table 2, note 1.

34

(2) See table 2, note 2.

(3) See table 2, note 3.

(4) See table 2, note 4.

35

4.5 Denial rates and reasons

As in past years, Black and Hispanic White borrowers had notably higher denial rates in 2019

than non-Hispanic White and Asian borrowers. For example, the denial rates for conventional

home-purchase loans were 16.0 percent for Black borrowers and 10.8 percent for Hispanic

White borrowers (Table 5). In contrast, denial rates for such loans were 8.6 percent for Asian

borrowers and 6.1 percent for non-Hispanic White borrowers.

Differences in denial rates and in the incidence of higher-priced lending (the topic of the next

subsection) among racial and ethnic groups may stem, at least in part, from factors related to

credit risk.

34

Some of those factors—such as credit history (including credit score), ratio of total

monthly DTI ratio, and combined loan-to-value (CLTV) ratio—were available for the second

consecutive year in the 2019 HMDA data.

35

Denial rates for home-purchase applications were generally lower in 2019 compared to 2018.

36

The overall denial rate on applications for conventional and nonconventional home-purchase

loans was 8.9 percent in 2019, 10 percent lower than in 2018. The denial rate for each

racial/ethnic group also declined from 2018 to 2019. These declines in 2019 continued a general

trend since the Great Recession of declining denial rates for home-purchase mortgages.

Although denial rates on home-purchase applications declined from 2018 to 2019, the rate of

decline varied by racial/ethnic group and types of loans. For example, for conventional and

nonconventional applications combined, denial rates for non-Hispanic Whites declined from 7.9

percent in 2018 to 7.0 percent in 2019 (11 percent decline) compared to a smaller decline for

Blacks from 17.4 percent to 15.9 percent (8 percent). As a second example, the denial rate for all

applications for nonconventional home-purchase loans decreased by 11 percent, while that for

conventional loans decreased by 9 percent.

34

HMDA data are regularly used in fair lending examination and enforcement processes. When

examiners for the federal banking agencies evaluate an institution’s fair lending risk, they analyze HMDA

price data, loan application outcomes, and explanatory factors, in conjunction with other information and

risk factors, which can be drawn directly from loan files or electronic records maintained by lenders, in

accordance with the Interagency Fair Lending Examination Procedures (available at

https://www.ffiec.gov/PDF/fairlend.pdf).

35

To protect applicant and borrower privacy, credit score is excluded from the 2019 application-level

HMDA data made available to the public, and DTI is binned into ranges.

36

Denial rates are calculated as the number of denied loan applications divided by the total number of

applications, excluding withdrawn applications and application files closed for incompleteness.

36

Consistent with home-purchase loans, denial rates on refinance applications also decreased

between 2018 and 2019 but at a much faster rate. Denial rates on refinance loans applications

for conventional and nonconventional combined decreased by 34 percent, from 29.0 percent in

2018 to 19.2 percent in 2019. Furthermore, denial rates for all refinance loan types decreased

between 2018 and 2019 for all racial and ethnic groups with the largest change being a 42-

percent decline for Asian applicants for conventional loans. Overall, refinance applications were

denied at about twice the rate of home-purchase applications.

37

TABLE 5: HOME-PURCHASE AND REFINANCE LOAN DENIAL RATES, BY LOAN TYPE AND BORROWER RACE AND

ETHNICITY, 2004-2019 (PERCENT)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

A. Home Purchase

Conventional and

nonconventional

(1)

All applicants 14.4 16.0 18.0 18.7 18.0 15.5 15.6 15.8 14.9 14.4 13.3 12.1 11.5 10.7 9.8 8.9

Asian 13.7 15.9 16.9 17.5 19.2 16.3 15.9 16.5 15.8 15.3 14.1 12.7 11.6 10.6 10.2 9.1

Black or African American 23.6 26.5 30.3 33.5 30.6 25.5 24.9 26.0 26.0 25.5 23.0 20.8 19.8 18.4 17.4 15.9

Hispanic white 18.3 21.1 25.1 29.5 28.3 22.2 21.8 21.1 20.2 20.5 18.4 16.2 15.0 13.4 13.1 11.6

Non-Hispanic white 11.1 12.2 12.9 13.3 14.0 12.8 13.0 13.1 12.5 12.0 11.1 10.0 9.5 8.8 7.9 7.0

Other minority

(2)

19.4 20.8 24.0 26.7 25.5 21.2 22.0 20.9 20.8 21.2 19.0 17.2 16.6 14.7 14.3 13.0

Conventional only

All applicants 14.6 16.3 18.5 19.0 18.3 15.8 15.2 15.1 13.6 12.9 11.9 10.8 10.2 9.6 8.4 7.6

Asian 13.7 16.0 17.1 17.5 19.1 15.8 14.9 15.5 14.4 14.2 13.3 11.9 10.9 10.1 9.6 8.6

Black or African American 25.0 27.8 31.9 35.7 37.6 35.8 33.7 33.2 32.0 28.5 25.1 23.3 22.0 19.2 16.9 16.0

Hispanic white 18.6 21.4 25.7 30.5 32.5 26.9 24.9 24.2 22.4 21.5 18.9 17.2 15.4 13.5 12.1 10.8

Non-Hispanic white 11.2 12.3 13.2 13.3 14.1 13.3 12.9 12.7 11.6 10.8 9.9 9.1 8.5 7.8 6.8 6.1

Other minority

(2)

19.7 21.2 24.8 27.8 29.0 25.9 28.1 24.6 23.6 22.5 20.2 18.2 16.8 14.8 13.4 12.9

Nonconventional only

(1)

All applicants 13.3 12.5 12.1 16.2 17.4 15.3 16.0 16.5 16.3 16.8 15.8 13.9 13.4 12.8 12.7 11.3

Asian 12.6 11.6 10.6 15.5 20.2 17.7 18.7 19.3 20.2 20.6 18.9 16.2 14.9 14.1 14.2 12.9

Black or African American 17.7 16.8 16.2 22.8 25.3 22.6 22.7 23.9 24.0 24.1 21.9 19.7 18.8 17.9 17.7 15.9

Hispanic white 16.3 17.2 15.7 20.5 23.1 20.4 20.7 19.9 19.3 19.9 18.0 15.6 14.7 13.4 14.3 12.4

38

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Non-Hispanic white 10.7 10.2 10.0 13.1 13.9 12.5 13.0 13.6 13.7 14.1 13.4 11.7 11.2 10.6 10.5 9.1

Other minority

(2)

16.8 16.3 15.2 18.6 20.9 18.7 18.7 18.8 18.9 20.1 17.9 16.2 16.4 14.7 15.2 13.2

B. Refinance

Conventional and

nonconventional

(1)

All applicants 29.5 32.6 35.4 39.6 37.7 24.0 23.3 23.8 19.9 23.3 31.0 27.2 29.9 26.3 29.0 19.2

Asian 18.8 23.5 27.5 32.6 32.5 21.4 19.5 20.1 17.3 21.0 28.1 23.8 25.1 24.7 28.0 16.0

Black or African American 39.9 42.2 44.1 52.0 56.0 42.2 41.7 40.0 32.8 35.0 45.8 43.1 45.9 39.1 44.1 32.8

Hispanic white 28.7 30.1 33.2 43.0 49.1 36.4 33.4 33.2 27.5 29.6 36.7 32.5 33.8 30.1 32.0 23.0

Non-Hispanic white 24.1 26.9 30.1 33.7 32.2 20.7 20.6 21.3 17.8 20.5 27.5 24.1 26.9 22.9 24.9 16.4

Other minority

(2)

33.7 35.5 40.6 52.0 57.4 37.3 35.4 34.4 30.0 32.1 41.6 40.1 44.2 37.2 42.2 30.4

Conventional only

All applicants 30.1 32.9 35.6 39.9 37.0 22.1 21.2 22.3 19.4 22.5 29.6 26.4 28.8 24.0 24.8 16.6

Asian 18.8 23.5 27.5 32.5 31.5 20.2 18.5 19.4 17.0 20.5 27.2 23.2 23.7 23.4 25.4 14.7

Black or African American 41.7 43.0 44.7 53.3 60.9 48.6 41.4 40.6 34.8 36.0 47.0 47.7 52.3 39.3 39.9 33.5

Hispanic white 29.3 30.2 33.3 43.2 50.2 38.9 33.6 33.5 28.9 30.6 37.3 34.8 35.2 30.0 30.1 22.7

Non-Hispanic white 24.6 27.1 30.4 33.9 31.5 19.1 18.9 20.1 17.4 19.9 26.2 23.2 25.7 20.6 21.2 14.1

Other minority

(2)

34.5 35.7 40.9 52.6 59.4 38.4 34.8 34.4 31.1 32.6 40.9 41.2 45.9 34.5 37.1 28.5

Nonconventional only

(1)

All applicants 15.0 20.1 21.9 31.6 40.9 31.1 33.3 32.2 22.2 26.7 36.5 29.6 33.0 32.4 39.6 25.7

Asian 15.0 20.0 22.0 38.5 48.9 37.2 34.2 32.7 22.2 26.9 37.5 28.8 36.7 34.1 43.7 26.7

Black or African American 17.5

23.6 24.6 33.7 43.5 35.1 42.2 39.1 29.5 33.1 43.9 37.5 38.8 38.8 48.9 32.2

Hispanic white 15.7 23.6 26.3 34.6 43.4 31.4 33.0 32.3 23.3 26.6 34.5 27.1 30.5 30.6 37.3 23.7

39

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Non-Hispanic white 12.0 17.6 19.7 28.3 36.1 27.4 29.3 29.0 19.7 23.8 33.7 26.9 31.0 29.7 36.0 23.3

Other minority

(2)

15.2 25.8 22.2 34.8 45.4 34.1 37.0 34.4 26.6 30.6 43.8 37.6 41.2 41.9 50.2 33.3