Financial Management

IV -Semester BBA

Bangalore University

Prepared by,

Dr.S.HARIHARAPUTHRIAN

Prof.Management

New Horizon College,

Kasturi Nagar,

Bangalore -43.

4.4 FINANCIAL MANAGEMENT

OBJECTIVE

The objective is to enable students to understand the basic concepts of Financial Management

and the role of Financial Management in decision-making.

Unit 1: INTRODUCTION TO FINANCIAL MANAGEMENT 10 Hrs

Introduction – Meaning of Finance – Business Finance – Finance Function – Aims of Finance

Function – Organization structure of finance - Financial Management – Goals of Financial

Management – Financial Decisions – Role of a Financial Manager – Financial Planning – Steps

in Financial Planning – Principles of a Sound Financial Planning.

Unit 2: TIME VALUE OF MONEY 10 Hrs

Introduction – Meaning & Definition – Need – Future Value (Single Flow – Uneven Flow &

Annuity) – Present Value (Single Flow – Uneven Flow & Annuity)– Doubling Period – Concept

of Valuation – Valuation of Bonds & Debentures – Preference Shares – Equity Shares – Simple

Problems.

Unit 3: FINANCING DECISION AND INVESTMENT DECISION 16Hrs

Financing Decisions: Introduction – Meaning of Capital Structure – Factors influencing Capital

Structure – Optimum Capital Structure – EBIT – EBT – EPS – Analysis – Leverages – Types of

Leverages – Simple Problems.

Investment Decisions: Introduction – Meaning and Definition of Capital Budgeting – Features –

Significance – Process – Techniques – Payback Period – Accounting Rate of Return – Net

Present Value – Internal Rate of Return – Profitability Index - Simple Problems

Unit 4: DIVIDEND DECISION 08 Hrs

Introduction – Meaning and Definition – Determinants of Dividend Policy – Types of Dividends

Provisions under Campiness Act in relation to dividends.

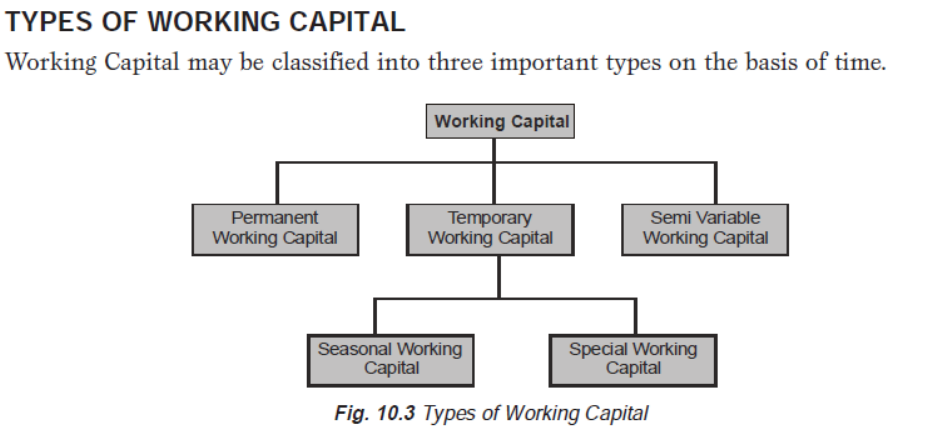

Unit 5: WORKING CAPITAL MANAGEMENT 12 Hrs

Introduction – Concept of Working Capital – Significance of Adequate Working Capital – Evils

of Excess or Inadequate Working Capital – Determinants of Working Capital – Sources of

Working Capital –Cash Management – Receivables Management – Inventory Management,.

SKILL DEVELOPMENT

Draw the organization chart of Finance Function

Illustrate operating cycle for at least 2 companies of your choice.

Evaluate the NPV of an investment made in any one of the capital projects with imaginary

figures for 5 years.

Prepare an ageing schedule of debtors with imaginary figures.

Capital structure analysis of companies in different industries

BOOKS FOR REFERENCE

1. Reddy, Appananaih: Financial Management., HPH

2. Sudrashan Reddy – Financial Management, HPH.

3. Venkataraman R _ Financial Management, VBH.

4. S N Maheshwari, Financial Management., Sultan Chand.

5. R.M.Srivastava : Financial Management –Management and Policy, Himalaya Publishers.

6. Khan and Jain, Financial Management, Tata McGraw Hill.

7. Dr. K.V. Venkataramana, Financial Management, SHB Publications.

8. Sudhindra Bhatt: Financial Management, Excel Books.

Unit I

INTRODUCTION TO FINANCIAL MANAGEMENT

Introduction – Meaning of Finance – Business Finance – Finance Function – Aims of Finance

Function – Organization structure of finance - Financial Management – Goals of Financial

Management – Financial Decisions – Role of a Financial Manager – Financial Planning – Steps

in Financial Planning – Principles of a Sound Financial Planning.

Introduction

Finance describes the management, creation and study of money, banking, credit, investments,

assets and liabilities that make up financial systems, as well as the study of those financial

instruments. Some people prefer to divide finance into three distinct categories: public finance,

corporate finance and personal finance. There is also the recently emerging area of social

finance. Additionally, the study of behavioral finance aims to learn about the more "human" side

of a science considered by most to be highly mathematical.

'Finance'

Public finance includes tax systems, government expenditures, budget procedures, stabilization

policy and instruments, debt issues and other government concerns.

Corporate finance involves managing assets, liabilities, revenues and debt for a business.

Personal finance defines all financial decisions and activities of an individual or household,

including budgeting, insurance, mortgage planning, savings and retirement planning.

Corporate Finance

Businesses obtain financing through a variety of means, ranging from equity investments to

credit arrangements. A firm might take out a loan from a bank, or arrange for a line of

credit. Acquiring and managing debt properly can help a company expand and ultimately

become more profitable.

Startups may receive capital from angel investors or venture capitalists in exchange for a

percentage of ownership. If a company thrives and decides to go public, it will issue shares on a

stock exchange; such initial public offerings (IPO) bring a great influx of cash into a firm.

Established companies may sell additional shares, or issue corporate bonds to raise money.

Businesses may purchase dividend-paying stocks, blue-chip bonds or interest-bearing bank

certificates of deposit; they may even buy other companies in an effort to boost revenue.

Finance describes the management, creation and study of money, banking, credit, investments,

assets and liabilities that make up financial systems, as well as the study of those financial

instruments. Some people prefer to divide finance into three distinct categories: public finance,

corporate finance and personal finance. There is also the recently emerging area of social

finance. Additionally, the study of behavioral finance aims to learn about the more "human" side

of a science considered by most to be highly mathematical.

'Finance'

Public finance includes tax systems, government expenditures, budget procedures, stabilization

policy and instruments, debt issues and other government concerns. Corporate finance involves

managing assets, liabilities, revenues and debt for a business. Personal finance defines all

financial decisions and activities of an individual or household, including budgeting, insurance,

mortgage planning, savings and retirement planning.

Public Finance

The federal government helps prevent market failure by overseeing allocation of resources,

distribution of income and stabilization of the economy. Regular funding for these programs is

secured mostly through taxation. Borrowing from banks, insurance companies and other

governments and earning dividends from its companies also help finance the federal government.

State and local governments also receive grants and aid from the federal government. In addition,

user charges from ports, airport services and other facilities; fines resulting from breaking laws;

revenues from licenses and fees, such as for driving; and sales of government securities and bond

issues are also sources of public finance.

Corporate Finance

Businesses obtain financing through a variety of means, ranging from equity investments to

credit arrangements. A firm might take out a loan from a bank, or arrange for a line of

credit. Acquiring and managing debt properly can help a company expand and ultimately

become more profitable.

Startups may receive capital from angel investors or venture capitalists in exchange for a

percentage of ownership. If a company thrives and decides to go public, it will issue shares on a

stock exchange; such initial public offerings (IPO) bring a great influx of cash into a firm.

Established companies may sell additional shares, or issue corporate bonds to raise money.

Businesses may purchase dividend-paying stocks, blue-chip bonds or interest-bearing bank

certificates of deposit; they may even buy other companies in an effort to boost revenue.

Personal Finance

Personal financial planning generally involves analyzing an individual's or a family's current

financial position, predicting short-term and long-term needs and executing a plan to fulfill those

need within individual financial constraints. Personal finance is a very personal activity that

depends largely on one's earnings, living requirements and individual goals and desires.

Aims of Finance Function:

The primary aim of finance function is to arrange as much funds for the business as are required

from time to time.

This function has the following aims:

1. Acquiring Sufficient Funds:

The main aim of finance function is to assess the financial needs of an enterprise and then

finding out suitable sources for raising them. The sources should be commensurate with the

needs of the business. If funds are needed for longer periods then long-term sources like share

capital, debentures, term loans may be explored.

A concern with longer gestation period should rely more on owner’s funds instead of interest-

bearing securities because profits may not be there for some years.

2. Proper Utilisation of Funds:

Though raising of funds is important but their effective utilisation is more important. The funds

should be used in such a way that maximum benefit is derived from them. The returns from their

use should be more than their cost.

It should be ensured that funds do not remain idle at any point of time. The funds committed to

various operations should be effectively utilised. Those projects should be preferred which are

beneficial to the business.

3. Increasing Profitability:

The planning and control of finance function aims at increasing profitability of the concern. It is

true that money generates money. To increase profitability, sufficient funds will have to be

invested. Finance function should be so planned that the concern neither suffers from inadequacy

of funds nor wastes more funds than required.

A proper control should also be exercised so that scarce resources are not frittered away on

uneconomical operations. The cost of acquiring funds also influences profitability of the

business. If the cost of raising funds is more, then profitability will go down. Finance function

also requires matching of cost and returns from funds.

4. Maximising Firm’s Value:

Finance function also aims at maximising the value of the firm. It is generally said that a

concern’s value is linked with its profitability. Even though profitability influences a firm’s value

but it is not all. Besides profits, the type of sources used for raising funds, the cost of funds, the

condition of money market, the demand for products are some other considerations which also

influence a firm’s value.

Organization structure of finance

The roles assigned to finance department employees create the base of its organizational structure. For

most small businesses, these involve bookkeeping, payroll, financial and tax reporting, financing and

assisting in long-term business planning.

DEFINITION OF FINANCIAL MANAGEMENT

Financial management is an integral part of overall management. It is concerned with the duties

of the financial managers in the business firm.

The term financial management has been defined by Solomon, “It is concerned with the efficient

use of an important economic resource namely, capital funds”.

The most popular and acceptable definition of financial management as given by S.C. Kuchal is

that “Financial Management deals with procurement of funds and their effective utilization in the

business”.

Howard and Upton : Financial management “as an application of general managerial principles

to the area of financial decision-making.

Weston and Brigham : Financial management “is an area of financial decision-making,

harmonizing individual motives and enterprise goals”.

Joshep and Massie : Financial management “is the operational activity of a business that is

responsible for obtaining and effectively utilizing the funds necessary for efficient operations.

Thus, Financial Management is mainly concerned with the effective funds management in the

business. In simple words, Financial Management as practiced by business firms can be called as

Corporation Finance or Business Finance.

SCOPE OF FINANCIAL MANAGEMENT

Financial management is one of the important parts of overall management, which is directly

related with various functional departments like personnel, marketing and production. Financial

management covers wide area with multidimensional approaches. The following are the

important scope of financial management.

1. Financial Management and Economics

Economic concepts like micro and macroeconomics are directly applied with the financial

management approaches. Investment decisions, micro and macro environmental factors are

closely associated with the functions of financial manager. Financial management also uses the

economic equations like money value discount factor, economic order quantity etc. Financial

economics is one of the emerging area, which provides immense opportunities to finance, and

economical areas.

2. Financial Management and Accounting

Accounting records includes the financial information of the business concern. Hence, we can

easily understand the relationship between the financial management and accounting. In the

olden periods, both financial management and accounting are treated as a same discipline and

then it has been merged as Management Accounting because this part is very much helpful to

finance manager to take decisions. But nowaday’s financial management and accounting

discipline are separate and interrelated.

3. Financial Management or Mathematics

Modern approaches of the financial management applied large number of mathematical and

statistical tools and techniques. They are also called as econometrics. Economic order quantity,

discount factor, time value of money, present value of money, cost of capital, capital structure

theories, dividend theories,

ratio analysis and working capital analysis are used as mathematical and statistical tools and

techniques in the field of financial management.

4. Financial Management and Production Management

Production management is the operational part of the business concern, which helps to multiple

the money into profit. Profit of the concern depends upon the production performance.

Production performance needs finance, because production department requires raw material,

machinery, wages, operating expenses etc. These expenditures are decided and estimated by the

financial department

and the finance manager allocates the appropriate finance to production department. The

financial manager must be aware of the operational process and finance required for each process

of production activities.

5. Financial Management and Marketing

Produced goods are sold in the market with innovative and modern approaches. For this, the

marketing department needs finance to meet their requirements. Introduction to Financial

Management 5 The financial manager or finance department is responsible to allocate the

adequate finance to the marketing department. Hence, marketing and financial management are

interrelated and depends on each other.

6. Financial Management and Human Resource

Financial management is also related with human resource department, which provides an power

to all the functional areas of the management. Financial manager should carefully evaluate the

requirement of manpower to each department and allocate the finance to the human resource

department as wages,

salary, remuneration, commission, bonus, pension and other monetary benefits to the human

resource department. Hence, financial management is directly related with human resource

management.

OBJECTIVES OF FINANCIAL MANAGEMENT

Effective procurement and efficient use of finance lead to proper utilization of the finance by the

business concern. It is the essential part of the financial manager. Hence, the financial manager

must determine the basic objectives of the financial management. Objectives of Financial

Management may be broadly divided into two parts such as:

1. Profit maximization

2. Wealth maximization.

Profit Maximization

Main aim of any kind of economic activity is earning profit. A business concern is also

functioning mainly for the purpose of earning profit. Profit is the measuring techniques to

understand the business efficiency of the concern. Profit maximization is also the traditional and

narrow approach, which aims at, maximizes the profit of the concern. Profit maximization

consists of the following important features.

1. Profit maximization is also called as cashing per share maximization. It leads to maximize the

business operation for profit maximization.

2. Ultimate aim of the business concern is earning profit, hence, it considers all the possible ways

to increase the profitability of the concern.

3. Profit is the parameter of measuring the efficiency of the business concern. So it shows the

entire position of the business concern.

4. Profit maximization objectives help to reduce the risk of the business.

Favourable Arguments for Profit Maximization

The following important points are in support of the profit maximization objectives of the

business concern:

(i) Main aim is earning profit.

(ii) Profit is the parameter of the business operation.

(iii) Profit reduces risk of the business concern.

(iv) Profit is the main source of finance.

(v) Profitability meets the social needs also.

Unfavourable Arguments for Profit Maximization

The following important points are against the objectives of profit maximization:

(i) Profit maximization leads to exploiting workers and consumers.

(ii) Profit maximization creates immoral practices such as corrupt practice, unfair trade practice,

etc.

(iii) Profit maximization objectives leads to inequalities among the sake holders such as

customers, suppliers, public shareholders, etc.

Drawbacks of Profit Maximization

Profit maximization objective consists of certain drawback also:

Wealth Maximization

Wealth maximization is one of the modern approaches, which involves latest innovations and

improvements in the field of the business concern. The term wealth means shareholder wealth or

the wealth of the persons those who are involved in the business concern. Wealth maximization

is also known as value maximization or net present worth maximization. This objective is an

universally accepted concept in the field of business.

Favourable Arguments for Wealth Maximization

(i) Wealth maximization is superior to the profit maximization because the main aim of the

business concern under this concept is to improve the value or wealth of the shareholders.

(ii) Wealth maximization considers the comparison of the value to cost associated with the

business concern. Total value detected from the total cost incurred for the business operation. It

provides extract value of the business concern.

(iii) Wealth maximization considers both time and risk of the business concern.

(iv) Wealth maximization provides efficient allocation of resources.

(v) It ensures the economic interest of the society.

Unfavourable Arguments for Wealth Maximization

(i) Wealth maximization leads to prescriptive idea of the business concern but it may not be

suitable to present day business activities.

(ii) Wealth maximization is nothing, it is also profit maximization, it is the indirect name of the

profit maximization.

(iii) Wealth maximization creates ownership-management controversy.

(iv) Management alone enjoy certain benefits.

(v) The ultimate aim of the wealth maximization objectives is to maximize the profit.

ion, which involves the(vi) Wealth maximization can be activated only with the help of the

profitable position

of the business concern.

IMPORTANCE OF FINANCIAL MANAGEMENT

Finance is the lifeblood of business organization. It needs to meet the requirement of the business

concern. Each and every business concern must maintain adequate amount of finance for their

smooth running of the business concern and also maintain the business carefully to achieve the

goal of the business concern. The business goal can be achieved only with the help of effective

management of finance. We can’t neglect the importance of finance at any time at and at any

situation. Some of the importance of the financial management is as follows:

Financial Planning

Financial management helps to determine the financial requirement of the business concern and

leads to take financial planning of the concern. Financial planning is an important part of the

business concern, which helps to promotion of an enterprise.

Acquisition of Funds

Financial management involves the acquisition of required finance to the business concern.

Acquiring needed funds play a major part of the financial management, which involve possible

source of finance at minimum cost.

Proper Use of Funds

Proper use and allocation of funds leads to improve the operational efficiency of the business

concern. When the finance manager uses the funds properly, they can reduce the cost of capital

and increase the value of the firm.

Financial Decision

Financial management helps to take sound financial decision in the business concern. Financial

decision will affect the entire business operation of the concern. Because there is a direct

relationship with various department functions such as marketing, production personnel, etc.

Improve Profitability

Profitability of the concern purely depends on the effectiveness and proper utilization of funds by

the business concern. Financial management helps to improve the profitability position of the

concern with the help of strong financial control devices such as budgetary control, ratio analysis

and cost volume profit analysis.

Increase the Value of the Firm

Financial management is very important in the field of increasing the wealth of the investors and

the business concern. Ultimate aim of any business concern will achieve the maximum profit and

higher profitability leads to maximize the wealth of the investors as well as the nation.

Promoting Savings

Savings are possible only when the business concern earns higher profitability and maximizing

wealth. Effective financial management helps to promoting and mobilizing individual and

corporate savings.

Nowadays financial management is also popularly known as business finance or corporate

finances. The business concern or corporate sectors cannot function without the importance of

the financial management.

FUNCTIONS OF FINANCE MANAGER

Finance function is one of the major parts of business organization

permanent, and continuous process of the business concern. Finance is one of the interrelated

functions which deal with personal function, marketing function, production function and

research and development activities of the business concern. At present, every business concern

concentrates more on the field of finance because, it is a very emerging part which reflects the

entire operational and profit ability position of the concern. Deciding the proper financial

function is the essential and ultimate goal of the business organization.

Finance manager is one of the important role players in the field of finance function. He must

have entire knowledge in the area of accounting, finance, economics and management. His

position is highly critical and analytical to solve various problems related to finance. A person

who deals finance related activities may be called finance manager.

Finance manager performs the following major functions:

1. Forecasting Financial Requirements

It is the primary function of the Finance Manager. He is responsible to estimate the financial

requirement of the business concern. He should estimate, how much finances required to acquire

fixed assets and forecast the amount needed to meet the working capital requirements in future.

2. Acquiring Necessary Capital

After deciding the financial requirement, the finance manager should concentrate how the

finance is mobilized and where it will be available. It is also highly critical in nature.

3. Investment Decision

The finance manager must carefully select best investment alternatives and consider the

reasonable and stable return from the investment. He must be well versed in the field of capital

budgeting techniques to determine the effective utilization of investment. The finance manager

must concentrate to principles of safety, liquidity and profitability while investing capital.

Introduction to Financial Management 9

4. Cash Management

Present days cash management plays a major role in the area of finance because proper cash

management is not only essential for effective utilization of cash but it also helps to meet the

short-term liquidity position of the concern.

5. Interrelation with Other Departments

Finance manager deals with various functional departments such as marketing, production,

personel, system, research, development, etc. Finance manager should have sound knowledge

not only in finance related area but also well versed in other areas. He must maintain a good

relationship with all the functional departments of the business organization

UNIT – II

TIME VALUE OF MONEY

Definition

Time Value of Money is a concept that recognizes the relevant worth of future cash flows arising

as a result of financial decisions by considering the opportunity cost of funds.

Concept

Money loses its value over time which makes it more desirable to have it now rather than later.

There are several reasons why money loses value over time. Most obviously, there is inflation

which reduces the buying power of money.

But quite often, the cost of receiving money in the future rather than now will be greater than just

the loss in its real value on account of inflation. The opportunity cost of not having the money

right now also includes the loss of additional income that you could have earned simply by

having received the cash earlier. Moreover, receiving money in the future rather than now may

involve some risk and uncertainty regarding its recovery. For these reasons, future cash flows are

worth less than the present cash flows.

Time Value of Money concept attempts to incorporate the above considerations into financial

decisions by facilitating an objective evaluation of cash flows from different time periods by

converting them into present value or future value equivalents. This ensures the comparison of

'like with like'.

The present or future value of cash flows are calculated using a discount rate (also known as cost

of capital, WACC and required rate of return) that is determined on the basis of several factors

such as:

● Rate of inflation Higher the rate of inflation, higher the return that investors would require

on their investment.

● Interest Rates Higher the interest rates on deposits and debt securities, greater the loss of

interest income on future cash inflows causing investors to demand a higher return on

investment.

● Risk Premium Greater the risk associated with future cash flows of an investment, higher

the rate of return required by an investors to compensate for the additional risk.

Why is the Time Value of Money Important?

The time value of money is a concept integral to all parts of business. A business does not want

to know just what an investment is worth todayit wants to know the total value of the investment.

What is the investment worth in total? Let's take a look at a couple of examples.

Suppose you are one of the lucky people to win the lottery. You are given two options on how to

receive the money.

1. Option 1: Take Rs 5,00000 right now.

2. Option 2: Get paid Rs 6,00000 every year for the next 10 years.

In option 1, you get Rs5,000,000 and in option 2 you get Rs6,000,000. Option 2 may seem like

the better bet because you get an extra Rs 1,000,000, but the time value of money theory says

that since some of the money is paid to you in the future, it is worth less.

By figuring out how much option 2 is worth today (through a process called discounting), you'll

be able to make an apples-to-apples comparison between the two options. If option 2 turns out to

be worth less than $5,000,000 today, you should choose option 1, or vice versa.

Let's look at another example. Suppose you go to the bank and deposit $100. Bank 1 says that if

you promise not to withdraw the money for 5 years, they'll pay you an interest rate of 5% a year.

Before you sign up, consider that there is a cost to you for not having access to your money for 5

years. At the end of 5 years, Bank 1 will give you back $128. But you also know that you can go

to Bank 2 and get a guaranteed 6% interest rate, so your money is actually worth 6% a year for

every year you don't have it. Converting our present cash worth into future value using the two

different interest rates offered by Banks 1 and 2, we see that putting our money in Bank 1 gives

us roughly $128 in 5 years, while Bank 2's interest rate gives $134. Between these two options,

Bank 2 is the better deal for maximizing future value.

Relevance of time value of money in financial decision making

A finance manager is required to make decisions on investment, financing and

dividend in view of the company's objectives. The decisions as purchase of

assets or procurement of funds i.e. the investment/financing decisions affect the

cash flow in different time periods. Cash outflows would be at one point of time

and inflow at some other point of time, hence, they are not comparable due to

the change in rupee value of money. They can be made comparable by

introducing the interest factor. In the theory of finance, the interest factor is one

of the crucial and exclusive concept, known as the time value of money.

Time value of money means that worth of a rupee received today is

different from the same received in future. The preference for money now as

compared to future is known as time preference of money. The concept is

applicable to both individuals and business houses.

Reasons of time preference of money :

1) Risk :

There is uncertainty about the receipt of money in future.

2) Preference for present consumption :

Most of the persons and companies have a preference for present consumption

may be due to urgency of need.

3) Investment opportunities :

Most of the persons and companies have preference for present money because

of availabilities of opportunities of investment for earning additional cash

flows.

Importance of time value of money :

The concept of time value of money helps in arriving at the comparable value of

the different rupee amount arising at different points of time into equivalent

values of a particular point of time, present or future. The cash flows arising at

different points of time can be made comparable by using any one of the

following :

- by compounding the present money to a future date i.e. by finding out the

value of present money.

- by discounting the future money to present date i.e. by finding out the present

value(PV) of future money.

1) Techniques of compounding :

i) Future value (FV) of a single cash flow :

The future value of a single cash flow is defined as :

FV = PV (1 + r)

n

Where, FV = future value

PV = Present value

r = rate of interest per annum

n = number of years for which compounding is done.

If, any variable i.e. PV, r, n varies, then FV also varies. It is very tedious to

calculate the value of

(1 + r)

n

so different combinations are published in the form of tables. These may

be referred for computation, otherwise one should use the knowledge of

logarithms.

ii) Future value of an annuity :

An annuity is a series of periodic cash flows, payments or receipts, of equal

amount. The premium payments of a life insurance policy, for instance are an

annuity. In general terms the future value of an annuity is given as :

FVA

n

= A * ([(1 + r)

n

- 1]/r)

Where,

FVA

n

= Future value of an annuity which has duration of n

years.

A = Constant periodic flow

r = Interest rate per period

n = Duration of the annuity

Thus, future value of an annuity is dependent on 3 variables, they being, the annual

amount, rate of interest and the time period, if any of these variable changes it will

change the future value of the annuity. A published table is available for various

combination of the rate of interest 'r' and the time period 'n'.

2) Techniques of discounting :

i) Present value of a single cash flow :

The present value of a single cash flow is given as :

PV = FV

n

( 1 )

n

1 + r

Where,

FV

n =

Future value n years hence

r = rate of interest per annum

n = number of years for which discounting is done.

From above, it is clear that present value of a future money depends upon 3 variables i.e. FV, the

rate of interest and time period. The published tables for various combinations of ( 1

)n

1 + r

are available.

ii) Present value of an annuity :

Sometimes instead of a single cash flow, cash flows of same amount is received

for a number of years. The present value of an annuity may be expressed as

below :

PVA

n

= A/(1 + r)

1

+ A/(1 + r)

2

+ ................ + A/(1 + r)

n-1

+ A/(1 + r)

n

= A [1/(1 + r)

1

+ 1/(1 + r)

2

+ ................ + 1/(1 + r)

n-1

+ 1/(1 + r)

n

]

= A [ (1 + r)

n

- 1]

r(1 + r)

n

Where,

PVA

n

= Present value of annuity which has duration of n years

A = Constant periodic flow

r = Discount rate.

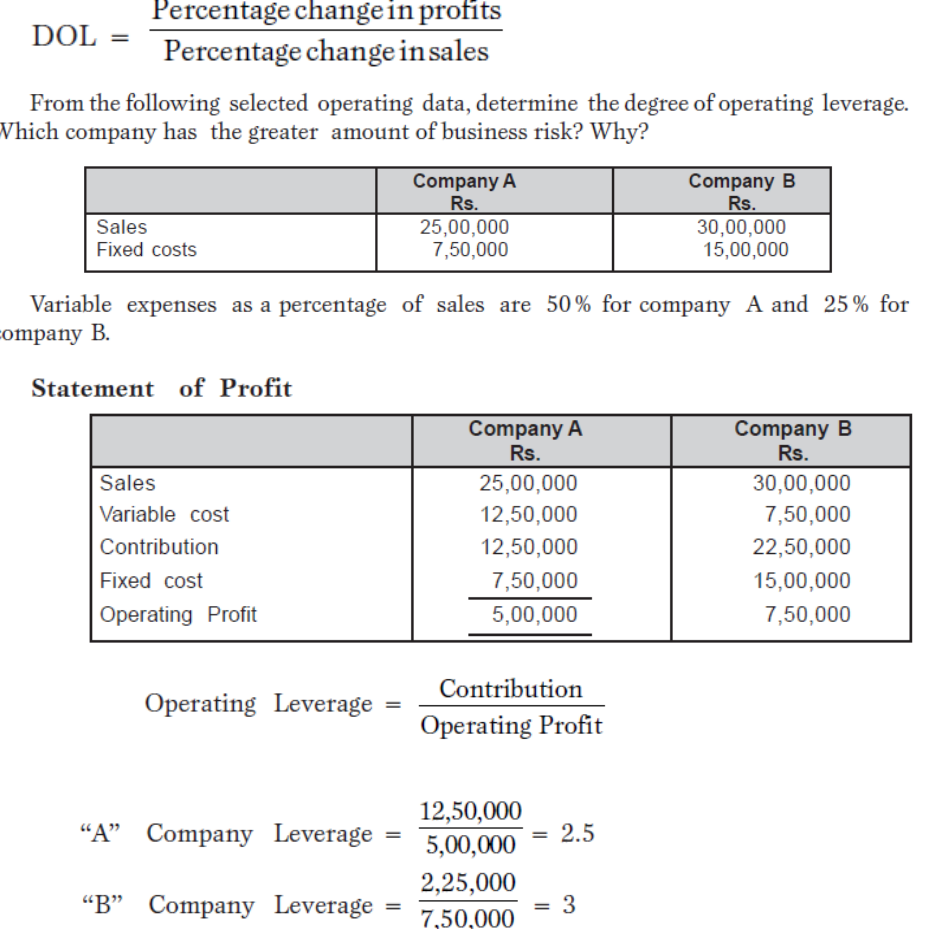

Risk and return is a complex topic. There are many types of risk, and many ways to evaluate

and measure risk. In the theory and practice of investing, a widely used definition of risk is:

“Risk is the uncertainty that an investment will earn its expected rate of return.”

Note that this definition does not distinguish between loss and gain. Typically, individual

investors think of risk as the possibility that their investments could lose money. They are likely

to be quite happy with an investment return that is greater than expected - a “positive surprise.”

However, since risky assets generate negative surprises as well as positive ones, defining risk as

the uncertainty of the rate of return is reasonable. Greater uncertainty results in greater

likelihood that the investment will generate larger gains, as well as greater likelihood that the

investment will generate larger losses (in the short term) and in higher or lower accumulated

value (in the long term.)

Concept of risk and return of a single asset and of a portfolio

The fact is that most investors invest their funds in more than one security suggest that there are other

factors, besides return, and they must be considered.

The investors not only like return but also dislike risk. So, what is required is: i.Clear understanding of

what risk and return are, ii.What creates them, and iii. How can they be measured?

Return:

the return is the basic motivating force and the principal reward in the investment process. The return may

be defined in terms of (i) realized return, i.e., the return which has been earned, and (ii) expected return,

i.e., the return which the investor anticipates to earn over some future investment period.

The expected return is a predicted or estimated return and mayor may not occur. The realized returns in

the past allow an investor to estimate cash inflows in terms of dividends, interest, bonus, capital gains,

etc, available to the holder of the investment.

The return can be measured as the total gain or loss to the holder over a given period of time and may be

defined as a percentage return on the initial amount invested. With reference to investment inequity

shares, return is consisting of the dividends and the capital gain or loss at the time of sale of these shares.

Risk:

Risk in investment analysis means that future returns from an investment are unpredictable. The concept

of risk may be defined as the possibility that the actual return may not be same as expected.

In other words, risk refers to the chance that the actual outcome (return)from an investment will differ

from an expected outcome. With reference to a firm, risk may be defined as the possibility that the actual

outcome of a financial decision may not be same as estimated.

The risk may be considered as a chance of variation in return. Investments having greater chances of

variations are considered more risky than those with lesser chances of variations. Between equity shares

and corporate bonds, the former is riskier than latter.

If the corporate bonds are held till maturity, then the annual interest inflows and maturity repayment are

fixed. However, in case of equity investment, neither the dividend inflow nor the terminal price is fixed.

Risk should be differentiated with uncertainty:

Risk is defined as a situation where the possibility of happening or non happening of an event can be

quantified and measured: while uncertainty is defined as a situation where this possibility cannot be

measured.

Thus, risk is a situation when probabilities can be assigned to an event on the basis of facts and figures

available regarding the decision. Uncertainty, on the other hand, is a situation where either the facts and

figures are not available, or the probabilities cannot be assigned.

Types of Risk:

1. Systematic Risk: It refers to that portion of variability in return which is caused by the factors

affecting all the firms. It refers to fluctuation in return due to general factors in the market such as money

supply, inflation, economic recessions, interest rate policy of the government, political factors, credit

policy, tax reforms, etc. these are the factors which affect almost all firms. The effect of these factors is to

cause the prices of all securities to move together. This part of risk arises because every security has a

built in tendency to move in line with fluctuations in the market. No investor can avoid or eliminate this

risk, whatever precautions or diversification may be resorted to. The systematic risk is also called the non-

diversifiable risk or general risk.

2. Market Risk: Market prices of investments, particularly equity shares may fluctuate widely within a

short span of time even though the earnings of the company are not changing. The reasons for this change

in prices may be varied. Due to one factor or the other, investors’ attitude may change towards equities

resulting in the change in market price. Change in market price causes the return from investment to very.

This is known as market risk. The market risk refers to variability in return due to change in market price

of investment. Market risk appears because of reaction of investors to different events. There are different

social, economic, political and firm specific events which affect the market price of equity shares. Market

psychology is another factor affecting market prices. In bull phases, market prices of all shares tend to

increase while in bear phases

The prices tend to decline. In such situations, the market prices are pushed beyond far out of line with the

fundamental value.

3. Interest-rate Risk:

interest rates on risk free securities and general interest rate level are related to each other. If the risk free

rate of interest rises or falls, the rate of interest on the other bond securities also rises or falls. The interest

rate risk refers to the variability in return caused by the change in level of interest rates. Such interest rate

risk usually appears through the change in market price of fixed income securities, i.e., bonds and

debentures. Security (bond and debentures) prices have an inverse relationship with the level of interest

rates. When the interest rate rises, the prices of existing securities fall and vice-versa.

3. Purchasing power or Inflation Risk:

The inflation risk refers to the uncertainty of purchasing power of cash flows to be received out of

investment. It shows the impact of inflation or deflation on the investment. The inflation risk is related to

interest rate risk because as inflation increases, the interest rates also tend to increase. The reason being

that the investor wants an additional premium for inflation risk (resulting from decrease in purchasing

power). Thus, there is an increase in interest rate. Investment involves a postponement in present

consumption. If an investor makes an investment, he forgoes the opportunity to buy some goods or

services during the investment period. If, during this period, the prices of goods and services go up, the

investor losses in terms of purchasing power. The inflation risk arises because of uncertainty of

purchasing power of the amount to be received from investment in future.

Unsystematic Risk:

The unsystematic risk represents the fluctuation in return from an investment due to factors which are

specific to the particular firm and not the market as a whole.

These factors are largely independent of the factors affecting market in general. Since these factors are

unique to a particular firm, these must be examined separately for each firm and for each industry.

These factors may also be called firm-specific as these affect one firm without affecting the other firms.

For example, a fluctuation in price of crude oil will affect the fortune of petroleum companies but not the

textile manufacturing companies.

As the unsystematic risk results from random events that tend to be unique to an industry or a firm, this

risk is random in nature. Unsystematic risk is also called specific risk or diversifiable risk

Types of Unsystematic Risk:

1. Business Risk:

Business risk refers to the variability in incomes of the firms and expected dividend there from, resulting

from the operating condition in which the firms have to operate. For example, if the earning or dividends

from a company are expected to increase say, by 6%, however, the actual increase is 10% or 12 %.The

variation in actual earnings than the expected earnings refers to business risk. Some industries have higher

business risk than others. So, the securities of higher business risk firms are more risky than the securities

of other firms which have lesser business risk.

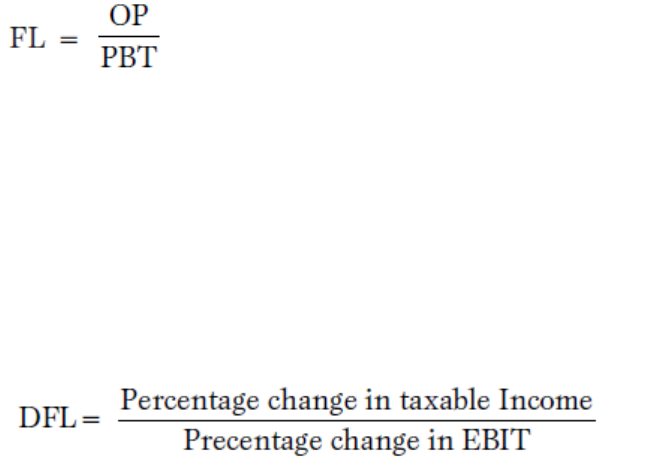

2. Financial Risk:

It refers to the degree of leverage or degree of debt financing used by a firm in the capital structure.

Higher the degree of debt financing, the greater is the degree of financial risk. The presence of interest

payment brings more variability in the earning available for equity shares. This is also known as financial

leverage. A firm having lesser or no risk financing has lesser or no financial risk.

Measurement of risk:

No investor can predict with certainty whether the income from an investment increase or decrease or by

how much. Statistical measures can be used to make precise measurement of risk about the estimated

returns, to gauge the extent to which the expected return and actual return are likely to differ

Methods Of Valuation Of Shares

The methods of valuation depends on the purpose for which valuation is required. Generally, there are

three methods of valuation of shares:

1. Net Assets Method Of Valuation Of Shares

Under this method, the net value of assets of the company are divided by the number of shares to arrive at

the value of each share. For the determination of net value of assets, it is necessary to estimate the worth

of the assets and liabilities. The goodwill as well as non-trading assets should also be included in total

assets. The following points should be considered while valuing of shares according to this method:

* Goodwill must be properly valued

* The fictitious assets such as preliminary expenses, discount on issue of shares and debentures,

accumulated losses etc. should be eliminated.

* The fixed assets should be taken at their realizable value.

* Provision for bad debts, depreciation etc. must be considered.

* All unrecorded assets and liabilities ( if any) should be considered.

* Floating assets should be taken at market value.

* The external liabilities such as sundry creditors, bills payable, loan, debentures etc. should be deducted

from the value of assets for the determination of net value.

The net value of assets, determined so has to be divided by number of equity shares for finding out the

value of share. Thus the value per share can be determined by using the following formula:

Value Per Share=(Net Assets-Preference Share Capital)/Number Of Equity Shares

2. Yield or Market Value Method Of Valuation Of Shares

The expected rate of return in investment is denoted by yield. The term "rate of return" refers to the return

which a shareholder earns on his investment. Further it can be classified as (a) Rate of earning and (b)

Rate of dividend. In other words, yield may be earning yield and dividend yield.

a. Earning Yield

Under this method, shares are valued on the basis of expected earning and normal rate of return. The

value per share is calculated by applying following formula:

Value Per Share = (Expected rate of earning/Normal rate of return) X Paid up value of equity share

Expected rate of earning = (Profit after tax/paid up value of equity share) X 100

b. Dividend Yield

Under this method, shares are valued on the basis of expected dividend and normal rate of return. The

value per share is calculated by applying following formula:

Expected rate of dividend = (profit available for dividend/paid up equity share capital) X 100

Value per share = (Expected rate of dividend/normal rate of return) X 100

3. Earning Capacity Method Of Valuation Of Shares

Under this method, the value per share is calculated on the basis of disposable profit of the company. The

disposable profit is found out by deducting reserves and taxes from net profit. The following steps are

applied for the determination of value per share under earning capacity:

Step 1: To find out the profit available for dividend

Step 2: To find out the capitalized value

Capitalized Value =( Profit available for equity dividend/Normal rate of return) X 100

Step 3: To find out value per share

Value per share = Capitalized Value/Number of Shares

4. Intrinsic value

The intrinsic value is the difference between the underlying price and the strike price, to the extent that

this is in favor of the option holder. For a call option, the option is in-the-money if the underlying price is

higher than the strike price; then the intrinsic value is the underlying price minus the strike price. For a

put option, the option is in-the-money if the strike price is higher than the underlying price; then the

intrinsic value is the strike price minus the underlying price. Otherwise the intrinsic value is zero.

In simple words, it is the value by which is already available in the market. If you are holding NIFTY

5000 Call (Bullish/Long) option and NIFTY is at 5050 level then you already have

₹ 50 advantage

if the option expires today. These ₹ 50 are the intrinsic value of option.

Conversely if you are holding a put option and NIFTY is below strike price then your option has an

intrinsic value equaling the difference between the strike price and NIFTY value. So,

Intrinsic value

= current stock price – strike price (call option)

= strike price – current stock price (put option)

Time value

The option premium is always greater than intrinsic value. This extra money is for the risk which the

option writer/seller is undertaking. This is called the Time Value.

Time value is the amount the option trader is paying for a contract above its intrinsic value, with the belief

that prior to expiration the contract value will increase because of a favorable change in the price of the

underlying asset. Obviously, the longer the amount of time until the expiry of the contract, the greater the

time value. So,

Time value = option premium – intrinsic value

There are many factors which determine option premium. These factors affect the premium of the option

with varying intensity. Some of these factors are listed here:

Price of the underlying: Any fluctuation in the price of the underlying (stock/index/commodity)

obviously has the largest impact on premium of an option contract. An increase in the underlying price

increases the premium of call option and decreases the premium of put option. Reverse is true when

underlying price decreases.

Strike price: How far is the strike price from spot also has an impact on option premium. Say, if NIFTY

goes from 5000 to 5100 the premium of 5000 strike and of 5100 strike will change a lot compared to a

contract with strike of 5500 or 4700.

Time till expiry: Lesser the time to expiry, option premium follows the intrinsic value more closely. On

the expiry date Time Value approaches zero.

Volatility of underlying: Underlying security is a constantly changing entity. The degree by which its

price fluctuates can be termed as volatility. So a share which fluctuates 5% on either side on daily basis is

said to have more volatility than let’s say a stable blue chip shares whose fluctuation is more benign at 2–

3%. Volatility affects calls and puts alike. Higher volatility increases the option premium because of

greater risk it brings to the seller.

Apart from above, other factors like bond yield (or interest rate) also affect the premium. This is due to

the fact that the money invested by the seller can earn this risk free income in any case and hence while

selling option; he has to earn more than this because of higher risk he is taking.

Pricing models

Because the values of option contracts depend on a number of different variables in addition to the value

of the underlying asset, they are complex to value. There are many pricing models in use, although all

essentially incorporate the concepts of rational pricing, moneyness, option time value and put-call parity.

Amongst the most common models are:

Black–Scholes and the Black model

Binomial options pricing model

Monte Carlo option model

Finite difference methods for option pricing

Other approaches include:

Heston model

Heath–Jarrow–Morton framework Variance gamma model (see variance gamma process)

Bond Valuation

Bonds are long-term debt securities that are issued by corporations and government entities. Purchasers of

bonds receive periodic interest payments, called coupon payments, until maturity at which time they

receive the face value of the bond and the last coupon payment. Most bonds pay interest semiannually.

The Bond Indenture or Loan Contract specifies the features of the bond issue. The following terms are

used to describe bonds.

Par or Face Value

The par or face value of a bond is the amount of money that is paid to the bondholders at maturity. For

most bonds the amount is $1000. It also generally represents the amount of money borrowed by the bond

issuer.

Coupon Rate

The coupon rate, which is generally fixed, determines the periodic coupon or interest payments. It is

expressed as a percentage of the bond's face value. It also represents the interest cost of the bond issue to

the issuer.

Coupon Payments

The coupon payments represent the periodic interest payments from the bond issuer to the bondholder.

The annual coupon payment is calculated be multiplying the coupon rate by the bond's face value. Since

most bonds pay interest semiannually, generally one half of the annual coupon is paid to the bondholders

every six months.

Maturity Date

The maturity date represents the date on which the bond matures, i.e., the date on which the face value is

repaid. The last coupon payment is also paid on the maturity date.

Original Maturity

The time remaining until the maturity date when the bond was issued.

Remaining Maturity

The time currently remaining until the maturity date.

Call Date

For bonds which are callable, i.e., bonds which can be redeemed by the issuer prior to maturity, the call

date represents the date at which the bond can be called.

Call Price

The amount of money the issuer has to pay to call a callable bond. When a bond first becomes callable,

i.e., on the call date, the call price is often set to equal the face value plus one year's interest.

Required Return

The rate of return that investors currently require on a bond.

Yield to Maturity

The rate of return that an investor would earn if he bought the bond at its current market price and held it

until maturity. Alternatively, it represents the discount rate which equates the discounted value of a bond's

future cash flows to its current market price.

Yield to Call

The rate of return that an investor would earn if he bought a callable bond at its current market price and

held it until the call date given that the bond was called on the call date.

The box below illustrates the cash flows for a semiannual coupon bond with a face value of $1000, a 10%

coupon rate, and 15 years remaining until maturity. (Note that the annual coupon is $100 which is

calculated by multiplying the 10% coupon rate times the $1000 face value. Thus, the periodic coupon

payments equal $50 every six months.)

Valuation of shares and bonds

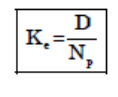

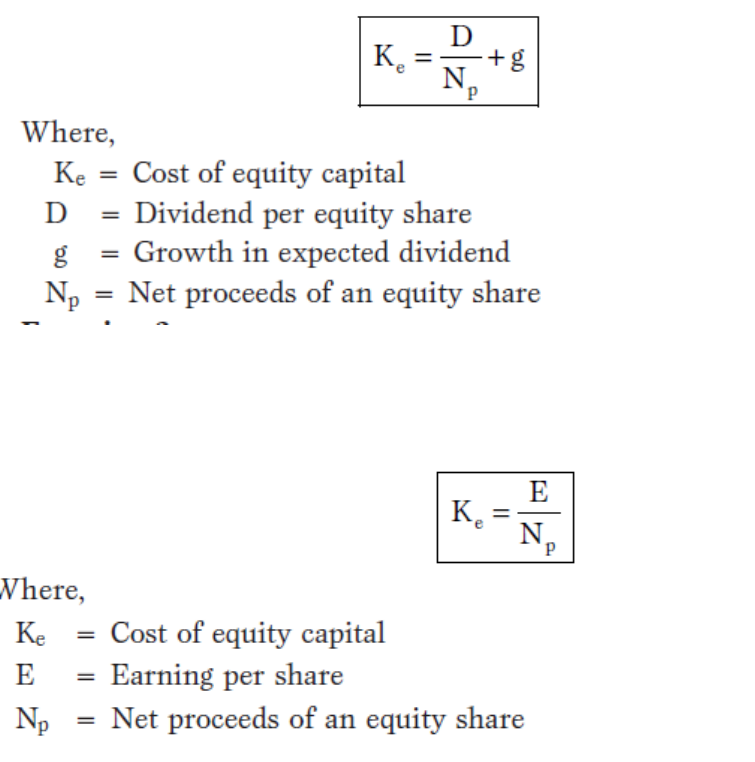

Cost of Equity

Cost of equity capital is the rate at which investors discount the expected dividends of the firm to

determine its share value.

Conceptually the cost of equity capital (Ke) defined as the “Minimum rate of return that a firm

must earn on the equity financed portion of an investment project in order to leave unchanged the

market price of the shares”.

Cost of equity can be calculated from the following approach:

• Dividend price (D/P) approach

• Dividend price plus growth (D/P + g) approach

• Earning price (E/P) approach

• Realized yield approach.

Dividend Price Approach

The cost of equity capital will be that rate of expected dividend which will maintain the present

market price of equity shares.

Dividend price approach can be measured with the help of the following formula:

Where,

Ke = Cost of equity capital

D = Dividend per equity share

Np = Net proceeds of an equity share

Exercise 1

A company issues 10,000 equity shares of Rs. 100 each at a premium of 10%. The company has

been paying 25% dividend to equity shareholders for the past five years and expects to maintain

the same in the future also. Compute the cost of equity capital. Will it make any difference if the

market price of equity share is Rs. 175?

(b) If the current market price of an equity share is Rs. 120. Calculate the cost of existing equity

share capital

Exercise 4

A firm is considering an expenditure of Rs. 75 lakhs for expanding its operations The relevant

information is as follows :

Number of existing equity shares =10 lakhs

Market value of existing share =Rs.100

Net earnings =Rs.100 lakhs

Compute the cost of existing equity share capital and of new equity capital assuming that new

shares will be issued at a price of Rs. 92 per share and the costs of new issue will be Rs. 2 per

share.

Solution

Cost of existing equity share capital:

Valuation of Debenture (Bond)

Cost of Debt

Cost of debt is the after tax cost of long-term funds through borrowing. Debt may be issued at

par, at premium or at discount and also it may be perpetual or redeemable.

Debt Issued at Par

Debt issued at par means, debt is issued at the face value of the debt. It may be calculated with

the help of the following formula.

Where,

Kd = Cost of debt capital

t = Tax rate

R = Debenture interest rate

Debt Issued at Premium or Discount

If the debt is issued at premium or discount, the cost of debt is calculated with the help of the

following formula

Where,

Kd = Cost of debt capital

I = Annual interest payable

Np = Net proceeds of debenture

t = Tax rate

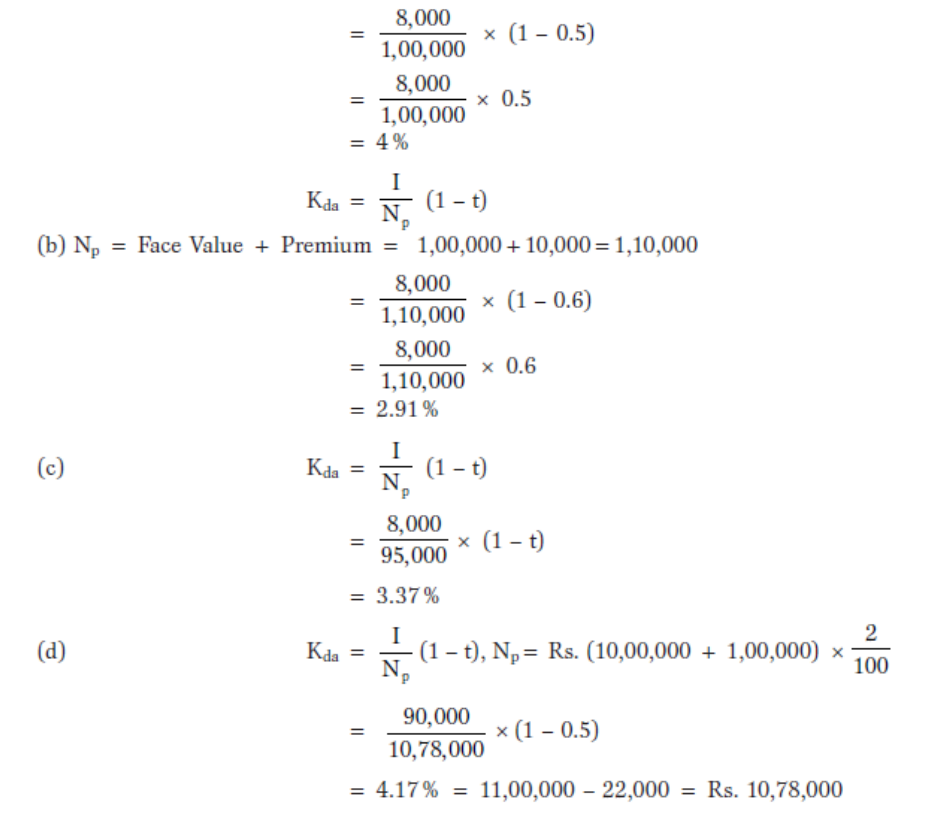

Exercise 5

(a) A Ltd. issues Rs. 10,00,000, 8% debentures at par. The tax rate applicable to the company is

50%. Compute the cost of debt capital.

(b) B Ltd. issues Rs. 1,00,000, 8% debentures at a premium of 10%. The tax rate applicable to

the company is 60%. Compute the cost of debt capital.

(c) A Ltd. issues Rs. 1,00,000, 8% debentures at a discount of 5%. The tax rate is 60%, compute

the cost of debt capital.

(d) B Ltd. issues Rs. 10,00,000, 9% debentures at a premium of 10%. The costs of floatation are

2%. The tax rate applicable is 50%. Compute the cost of debt-capital.

In all cases, we have computed the after-tax cost of debt as the firm saves on account of tax by

using debt as a source of finance.

Solution

UNIT- III

FINANACING DECISISONS AND INVESTMENT DECISIONS

Capital Budgeting: Principles and techniques - Nature of capital budgeting- Identifying relevant

cash flows - Evaluation Techniques: Payback, Accounting rate of return, Net Present Value,

Internal Rate of Return, Profitability Index - Comparison of DCF techniques - Project selection

under capital rationing - Inflation and capital budgeting - Concept and measurement of cost of

capital - Specific cost and overall cost of capital

Nature of Capital Budgeting:

Capital budgeting is the process of making investment decisions in capital expenditures. A

capital expenditure may be defined as an expenditure the benefits of which are expected to be

received over period of time exceeding one year.

The main characteristic of a capital expenditure is that the expenditure is incurred at one point of

time whereas benefits of the expenditure are realized at different points of time in future. In

simple language we may say that a capital expenditure is an expenditure incurred for acquiring

or improving the fixed assets, the benefits of which are expected to be received over a number of

years in future.

The following are some of the examples of capital expenditure:

(1) Cost of acquisition of permanent assets as land and building, plant and machinery, goodwill,

etc.

(2) Cost of addition, expansion, improvement or alteration in the fixed assets.

(3) Cost of replacement of permanent assets.

(4) Research and development project cost, etc.

Capital expenditure involves non-flexible long-term commitment of funds. Thus, capital

expenditure decisions are also called as long term investment decisions. Capital budgeting

involves the planning and control of capital expenditure. It is the process of deciding whether or

not to commit resources to a particular long term project whose benefits are to be realized over a

period of time, longer than one year. Capital budgeting is also known as Investment Decision

Making, Capital Expenditure Decisions, Planning Capital Expenditure and Analysis of Capital

Expenditure.

Charles T. Horngreen has defined capital budgeting as, “Capital budgeting is long term planning

for making and financing proposed capital outlays.”

According to G.C. Philippatos, “Capital budgeting is concerned with the allocation of the firm’s

scarce financial resources among the available market opportunities. The consideration of

investment opportunities involves the comparison of the expected future streams of earnings

from a project with the immediate and subsequent streams of earning from a project, with the

immediate and subsequent streams of expenditures for it”.

Richard and Greenlaw have referred to capital budgeting as acquiring inputs with long-run

return.

In the words of Lynch, “Capital budgeting consists in planning development of available capital

for the purpose of maximizing the long term profitability of the concern.”

From the above description, it may be concluded that the important features which

distinguish capital budgeting decision from the ordinary day to day business decisions are:

(1) Capital budgeting decisions involve the exchange of current funds for the benefits to be

achieved in future;

(2) The future benefits are expected to be realized over a series of years;

(3) The funds are invested in non-flexible and long term activities;

(4) They have a long term and significant effect on the profitability of the concern;

(5) They involve, generally, huge funds;

(6) They are irreversible decisions.

(7) They are ‘strategic’ investment decisions, involving large sums of money, major departure

from the past practices of the firm, significant change of the firm’s expected earnings associated

with high degree of risk, as compared to ‘tactical’ investment decisions which involve a

relatively small amount of funds that do not result in a major departure from the past practices of

the firm.

Need and Importance of Capital Budgeting:

Capital budgeting means planning for capital assets.

Capital budgeting decisions are vital to any organisation as they include the decisions as to:

(a) Whether or not funds should be invested in long term projects such as setting of an industry,

purchase of plant and machinery etc.

(b) Analyze the proposal for expansion or creating additional capacities.

(c) To decide the replacement of permanent assets such as building and equipment’s.

(d) To make financial analysis of various proposals regarding capital investments so as to choose

the best out of many alternative proposals.

The importance of capital budgeting can be well understood from the fact that an unsound

investment decision may prove to be fatal to the very existence of the concern.

The need, significance or importance of capital budgeting arises mainly due to the

following:

(1) Large Investments:

Capital budgeting decisions, generally, involve large investment of funds. But the funds

available with the firm are always limited and the demand for funds far exceeds the resources.

Hence, it is very important for a firm to plan and control its capital expenditure.

(2) Long-term Commitment of Funds:

Capital expenditure involves not only large amount of funds but also funds for long-term or more

or less on permanent basis. The long-term commitment of funds increases the financial risk

involved in the investment decision. Greater the risk involved, greater is the need for careful

planning of capital expenditure, i.e. Capital budgeting.

(3) Irreversible Nature:

The capital expenditure decisions are of irreversible nature. Once the decision for acquiring a

permanent asset is taken, it becomes very difficult to dispose of these assets without incurring

heavy losses.

(4) Long-Term Effect on Profitability:

Capital budgeting decisions have a long-term and significant effect on the profitability of a

concern. Not only the present earnings of the firm are affected by the investments in capital

assets but also the future growth and profitability of the firm depends upon the investment

decision taken today. An unwise decision may prove disastrous and fatal to the very existence of

the concern. Capital budgeting is of utmost importance to avoid over investment or under

investment in fixed assets.

(5) Difficulties of Investment Decisions:

The long term investment decisions are difficult to be taken because:

(i) Decision extends to a series of years beyond the current accounting period,

(ii) Uncertainties of future and

(iii) Higher degree of risk.

(6) National Importance:

Investment decision though taken by individual concern is of national importance because it

determines employment, economic activities and economic growth. Thus, we may say that

without using capital budgeting techniques a firm may involve itself in a losing project. Proper

timing of purchase, replacement, expansion and alternation of assets is essential.

Limitations of Capital Budgeting:

Capital budgeting techniques suffer from the following limitations:

(1) All the techniques of capital budgeting presume that various investment proposals under

consideration are mutually exclusive which may not practically be true in some particular

circumstances.

(2) The techniques of capital budgeting require estimation of future cash inflows and outflows.

The future is always uncertain and the data collected for future may not be exact. Obliviously the

results based upon wrong data may not be good.

(3) There are certain factors like morale of the employees, goodwill of the firm, etc., which

cannot be correctly quantified but which otherwise substantially influence the capital decision.

(4) Urgency is another limitation in the evaluation of capital investment decisions.

(5) Uncertainty and risk pose the biggest limitation to the techniques of capital budgeting.

METHODS OF CAPITAL BUDGETING OF EVALUATION

By matching the available resources and projects it can be invested. The funds available are

always living funds. There are many considerations taken for investment decision process such

as environment and economic conditions.

The methods of evaluations are classified as follows:

(A) Traditional methods (or Non-discount methods)

(i) Pay-back Period Methods

(ii) Post Pay-back Methods

(iii) Accounts Rate of Return

(B) Modern methods (or Discount methods)

(i) Net Present Value Method

(ii) Internal Rate of Return Method

(iii) Profitability Index Method

Pay-back Period

Pay-back period is the time required to recover the initial investment in a project

(It is one of the non-discounted cash flow methods of capital budgeting).

Merits of Pay-back method

The following are the important merits of the pay-back method:

1. It is easy to calculate and simple to understand.

2. Pay-back method provides further improvement over the accounting rate return.

3. Pay-back method reduces the possibility of loss on account of obsolescence.

Demerits

1. It ignores the time value of money.

2. It ignores all cash inflows after the pay-back period.

3. It is one of the misleading evaluations of capital budgeting.

Accept /Reject criteria

If the actual pay-back period is less than the predetermined pay-back period, the project

would be accepted. If not, it would be rejected.

Exercise 1

Project cost is Rs. 30,000 and the cash inflows are Rs. 10,000, the life of the project is

5 years. Calculate the pay-back period.

Exercise 2

A project costs Rs. 20,00,000 and yields annually a profit of Rs. 3,00,000 after

depreciation @ 12½% but before tax at 50%. Calculate the pay-back period.

Uneven Cash Inflows

Normally the projects are not having uniform cash inflows. In those cases the pay-back period is

calculated, cumulative cash inflows will be calculated and then interpreted.

Exercise 3

Certain projects require an initial cash outflow of Rs. 25,000. The cash inflows for 6 years are

Rs. 5,000, Rs. 8,000, Rs. 10,000, Rs. 12,000, Rs. 7,000 and Rs. 3,000.

Solution

Accounting Rate of Return or Average Rate of Return

Average rate of return means the average rate of return or profit taken for considering

the project evaluation. This method is one of the traditional methods for evaluating

the project proposals:

Merits

1. It is easy to calculate and simple to understand.

2. It is based on the accounting information rather than cash inflow.

3. It is not based on the time value of money.

4. It considers the total benefits associated with the project.

Demerits

1. It ignores the time value of money.

2. It ignores the reinvestment potential of a project.

3. Different methods are used for accounting profit. So, it leads to some difficulties

in the calculation of the project.

Accept/Reject criteria

If the actual accounting rate of return is more than the predetermined required rate of

return, the project would be accepted. If not it would be rejected.

Exercise 5

A company has two alternative proposals. The details are as follows

Net Present Value

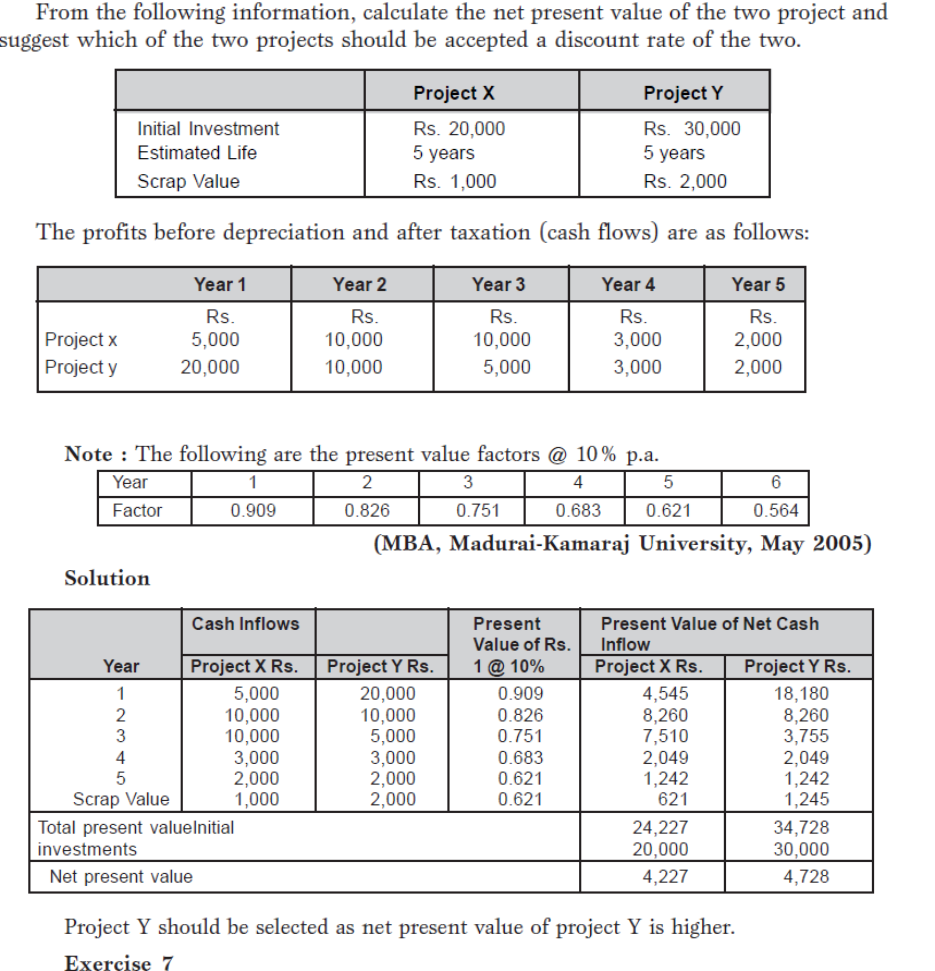

Net present value method is one of the modern methods for evaluating the project proposals. In

this method cash inflows are considered with the time value of the money. Net present value

describes as the summation of the present value of cash inflow and present value of cash

outflow. Net present value is the difference between the total present value of future cash inflows

and the total present value of future cash outflows.

Merits

1. It recognizes the time value of money.

2. It considers the total benefits arising out of the proposal.

3. It is the best method for the selection of mutually exclusive projects.

4. It helps to achieve the maximization of shareholders’ wealth.

Demerits

1. It is difficult to understand and calculate.

2. It needs the discount factors for calculation of present values.

3. It is not suitable for the projects having different effective lives.

Accept/Reject criteria

If the present value of cash inflows is more than the present value of cash outflows, it would be

accepted. If not, it would be rejected.

Exercise 6

From the following information, calculate the net present value of the two project and suggest

which of the two projects should be accepted a discount rate of the two.

Internal Rate of Return

Internal rate of return is time adjusted technique and covers the disadvantages of the traditional

techniques. In other words it is a rate at which discount cash flows to zero. It is expected by the

following ratio: Cash inflow Investment

Base factor = Positive discount rate

DP = Difference in percentage

Merits

1. It consider the time value of money.

2. It takes into account the total cash inflow and outflow.

3. It does not use the concept of the required rate of return.

4. It gives the approximate/nearest rate of return.

Demerits

1. It involves complicated computational method.

2. It produces multiple rates which may be confusing for taking decisions.

3. It is assume that all intermediate cash flows are reinvested at the internal rate

of return.

Accept/Reject criteria

If the present value of the sum total of the compounded reinvested cash flows is greater than the

present value of the outflows, the proposed project is accepted. If not it would be rejected.

Capital Rationing

In the rationing the company has only limited investment the project are selected according to

the profitability. The project has selected the combination of proposal that will yield the greatest

portability.

Exercise 12 Let us assume that a firm has only Rs. 20 lakhs to invest and funds cannot be

provided. The various proposals along with the cost and profitability index are as follows.

Solution

In this example all proposals expect number 2 give profitability exceeding one and are profitable

investments. The total outlay required to be invested in all other (profitable) project is Rs.

25,00,000(1+2+3+4+5) but total funds available with the firm are Rs. 20 lakhs and hence the firm has to

do capital combination of project within a total which has the lowest profitability index along with the

profitable proposals cannot be taken.

Meaning of Cost of Capital

Cost of capital is the rate of return that a firm must earn on its project investments to maintain its market

value and attract funds. Cost of capital is the required rate of return on its investments which belongs to

equity, debt and retained earnings. If a firm fails to earn return at the expected rate, the market value of

the shares will fall and it will result in the reduction of overall wealth of the shareholders.

Definitions

The following important definitions are commonly used to understand the meaning and concept of the

cost of capital.

According to the definition of John J. Hampton “ Cost of capital is the rate of return the firm required

from investment in order to increase the value of the firm in the market place”.

According to the definition of Solomon Ezra, “Cost of capital is the minimum required rate of earnings

or the cut-off rate of capital expenditure”.

IMPORTANCE OF COST OF CAPITAL

Computation of cost of capital is a very important part of the financial management to decide the capital

structure of the business concern.

Importance to Capital Budgeting Decision

Capital budget decision largely depends on the cost of capital of each source. According to net

present value method, present value of cash inflow must be more than the present value of cash

outflow. Hence, cost of capital is used to capital budgeting decision.

Importance to Structure Decision

Capital structure is the mix or proportion of the different kinds of long term securities. A firm

uses particular type of sources if the cost of capital is suitable. Hence, cost of capital helps to

take decision regarding structure.

Importance to Evolution of Financial Performance

Cost of capital is one of the important determine which affects the capital budgeting, capital

structure and value of the firm. Hence, it helps to evaluate the financial performance of the firm.

Importance to Other Financial Decisions

Apart from the above points, cost of capital is also used in some other areas such as, market

value of share, earning capacity of securities etc. hence, it plays a major part in the financial

management.

COMPUTATION OF COST OF CAPITAL

Computation of cost of capital consists of two important parts:

1. Measurement of specific costs

2. Measurement of overall cost of capital

Measurement of Cost of Capital

It refers to the cost of each specific sources of finance like:

• Cost of equity

• Cost of debt

• Cost of preference share

• Cost of retained earnings

Cost of Equity

Cost of equity capital is the rate at which investors discount the expected dividends of the

firm to determine its share value. Conceptually the cost of equity capital (Ke) defined as the

“Minimum rate of return that a firm must earn on the equity financed portion of an investment

project in order to leave unchanged the market price of the shares”.

Cost of equity can be calculated from the following approach:

• Dividend price (D/P) approach

• Dividend price plus growth (D/P + g) approach

• Earning price (E/P) approach

• Realized yield approach.

Dividend Price Approach

The cost of equity capital will be that rate of expected dividend which will maintain the

present market price of equity shares.

Dividend price approach can be measured with the help of the following formula:

Where,

Ke = Cost of equity capital

D = Dividend per equity share

Np = Net proceeds of an equity share

Exercise 1