.

Recommended Disclosures Regarding Exposure, Capital Calls and

Performance Impacts

June 2020

Enhancing Transparency Around

Subscription Lines of Credit

Enhancing Transparency Around Subscription Lines of Credit:

Recommended Disclosures Regarding Exposure, Capital Calls and Performance Impacts

June 2020

Background

In June 2017, ILPA issued guidance on best practices related to the use of Subscription Lines of Credit

1

, intended to

foster clearer and more informed dialogue between Limited and General Partners. Overall, the guidance was warmly

received and resulted in enhanced conversation among industry participants.

Since the 2017 guidance was released, utilization of subscription lines has grown, making LPs’ ability to measure and

assess both exposure and performance at the fund level and for their PE programs significantly more difficult. While

transparency generally has improved, both GPs and LPs indicate that the means for providing this transparency varies

widely, and related disclosures are not being systematically provided to LPs. Importantly, both LPs and GPs alike have

articulated the view that greater standardization around disclosures related to subscription lines will be beneficial to the

industry.

At the time of publication of these recommendations—in the early days of the Covid-19 era—LPs are scrutinizing more

closely than ever before both their liquidity and the cash flow models they use to project that liquidity. This is made

more challenging by the lack of visibility into how much of their unfunded commitment has been deployed into

investments but financed through a subscription line rather than called from LPs. Even with a substantial investment of

time and resources, LPs lack critical information that would engender confidence in the data used to inform critical

decisions with respect to their liquidity and exposure.

In monitoring fund-level performance within their portfolios, LPs are left with the near-impossible task of creating their

own methodology for zeroing in on the impact that subscription lines may have on Net IRRs. This is also an important

consideration in the evaluation of historical reported performance for prior funds during the fundraising process, in

determining how a prospective GP’s track record reflects value-add. There is no universal agreed-upon approach for

calculating returns with and without the impact of subscription lines, and reporting practices vary (e.g., frequency, level

of detail). Nonetheless, one important step that the industry can take is to present net performance calculated with and

without the use of subscription lines at a regular frequency and in a way that illustrates the impact of the use of such

facilities.

Intended Scope and Application

This 2020 guidance regarding subscription lines of credit disclosures is intended as a follow-on to the 2017 guidance;

both sets of guidance should be read in tandem. The aim of this subsequent guidance is to lay out more specifically the

incremental disclosures that will aid LPs and GPs in gaining clarity around the impact of subscription lines, particularly

with respect to an LP’s cash flow modeling and commitment pacing, as well as the performance impacts posed by

subscription lines.

ILPA recognizes there are valid and beneficial uses of subscription lines that help both GPs and LPs—not least being the

smoothing of cash flows and the flattening of the J-curve—and that the use of the subscription line will vary across

strategies. While the parameters prescribed in 2017 guidance with respect to maximum percentage of uncalled capital

(15-25%) and maximum days outstanding on the subscription line (180 days) were most relevant to private equity, the

implementation of the disclosure recommendations herein should be feasible across nearly all strategies.

1

For the avoidance of doubt, also referred to as subscription facilities, subscription line financing, capital call facilities, bridge lines.

The words subscription lines of credit, subscription line, subline, line of credit, credit facility, and facility are used interchangeably in

the document.

ILPA Guidance on Enhancing Transparency Around Subscription Lines of Credit: Recommended Disclosures 3

A common reporting standard for the periodic disclosure of amounts financed through subscription lines relative to an

LP’s unfunded commitment will save LPs meaningful time and resources in requesting and aggregating the information

required to manage their portfolio exposure. Additionally, by adhering to more standardized reporting and common

disclosure norms, including the provision of returns both with and without use of subscription lines, GPs will save

meaningful time and resources in responding to bespoke data requests from LPs, while also increasing the reliability of

performance data. ILPA understands there is not an agreed upon methodology for calculating performance with and

without the use of subscription lines. As such, emphasis here is placed on providing LPs with transparency into the

methodology used to calculate Net IRR, with and without the use of subscription lines, rather than prescribing a specific

methodology.

Approach

ILPA sought input from several subject matter experts, including consultants, CFOs within GP organizations, LPs,

academics, and industry groups on an anonymous basis to surface approaches and best practices around:

• Periodic disclosure of an LP’s unfunded commitment collateralized by the subscription facility; and

• The methodology used for calculating and reporting net returns, both with and without the impact of subscription

lines.

LP Challenges to Address

Lack of Visibility into Exposure and Accurate NAV Reporting

The use of subscription lines comes with a reduced cadence for, and potentially more concentrated, capital calls. When

capital is invested before it is called from the LP, it is difficult for the LP to achieve a clear understanding of their pro rata

share of the capital drawn from the subscription line. The LPs’ net asset value (NAV) does not include an allocation of the

amount owed to the subscription line due to the netting of assets and liabilities, which can lead to inaccuracies in

understanding the exposure across each fund and the entire portfolio. This can cause issues when considering institutional

allocation policy limits for private equity exposure as a percentage of the overall portfolio; LPs may be approaching or

even exceeding the upper bounds of policy limits should their unfunded commitment through subscription line usage be

taken into account. LPs have identified instances where actual private equity exposure may be as much as 2-4 percentage

points higher when factoring in their pro rata amount outstanding on subscription lines. Lack of clear visibility into this

exposure could result in the need to trim exposure to private equity under less than ideal circumstances, e.g., depressed

valuations in the secondaries market.

Cash Flow Management Difficulty

Consolidation of capital calls using subscription lines can be beneficial from an administrative perspective when done

correctly, smoothing cash flows generally. But it can also lead to cash flow management difficulties for the LP, particularly

in a down cycle when distributions typically used to fund capital calls may be decreasing. When LPs do not have a clear

understanding of how much capital will be called and when, they may struggle to balance their liquid and illiquid assets in

order to ensure sufficient liquidity to meet the demands of future capital calls. This challenge becomes more pronounced

when LPs are meeting capital calls by selling more liquid securities at a meaningful discount. During times of market

turmoil that lead to higher than anticipated capital calls or uncertainty surrounding the anticipated volume of future

capital calls – such as the current environment with Covid-19 – this issue is further exacerbated.

ILPA Guidance on Enhancing Transparency Around Subscription Lines of Credit: Recommended Disclosures 4

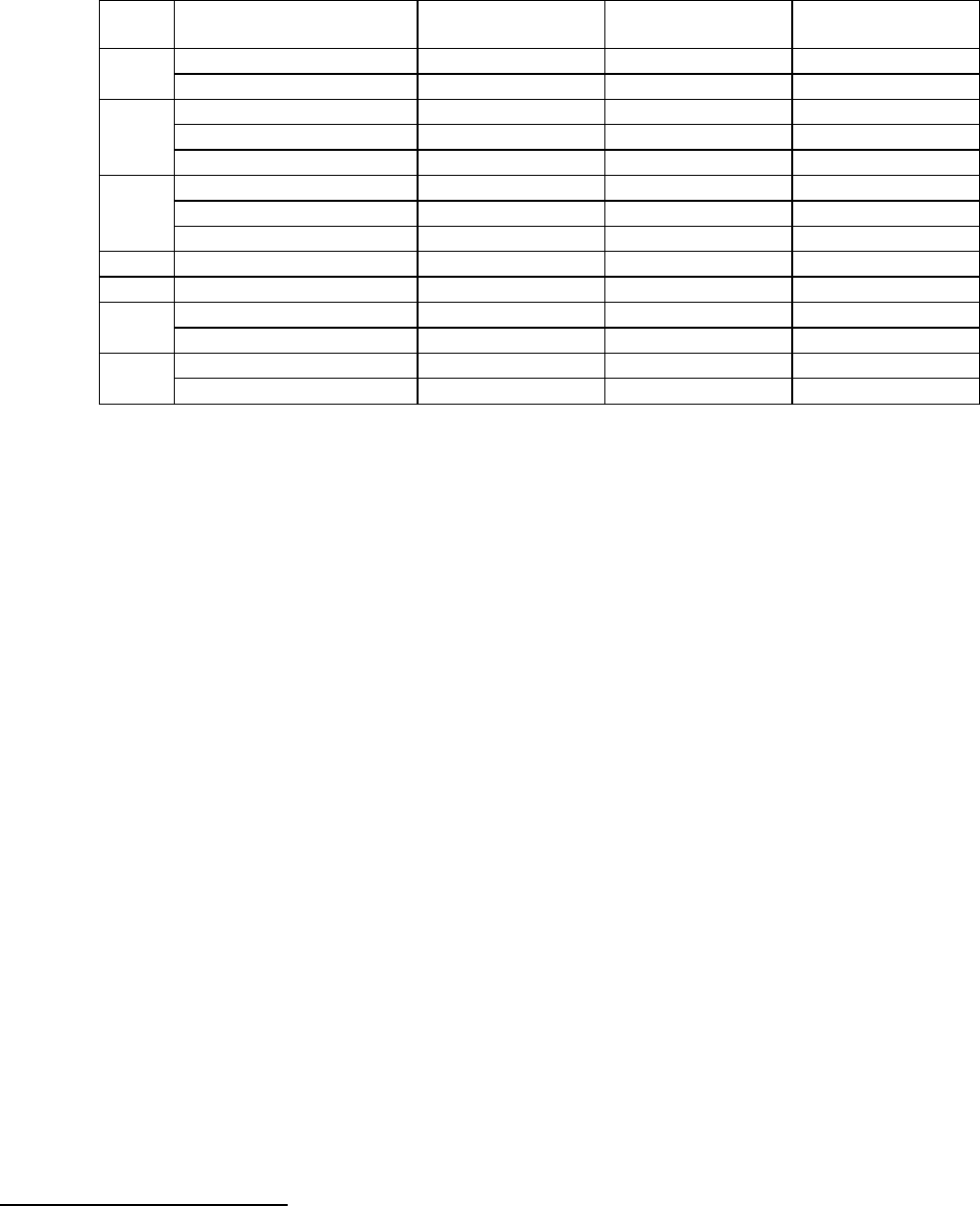

Inflated Returns and Impact on Performance Reporting

Because the use of such lines is not universal, the distortive effects on reported returns makes the comparability of

performance more challenging. A simplified notional example illustrates the effect of delaying the first capital call below:

Year

Transaction Type

Cash Flows

(without subline)

Cash Flows

(w/ 1-yr. subline)

Cash Flows

(w/ 2-yr. subline)

1

Investment

-100

Management Fees

-2

2

Investment

-100

Interest

-4

Management Fees

-2

-4

3

Investment

-100

Interest

-8

Management Fees

-2

-2

-6

4

Management Fees

-2

-2

-2

5

Management Fees

-2

-2

-2

6

Management Fees

-2

-2

-2

Realization

162

162

162

IRR

6.62%

7.14%

7.98%

TVPI

1.45x

1.40x

1.35x

The impact of use of a line of credit on IRR will be greatest early in the life of the fund and will naturally diminish later in

a fund’s life. Yet, it will never exactly equate to the level of the IRR without the subscription line (i.e., had the fund called

capital immediately from its LPs rather than utilizing the credit facility to temporarily finance the transaction

2

).

Systemic Risk

The rapid rise of this practice has brought forward questions about cumulative institutional liquidity risk. In particular, LPs

have raised concerns about the ability for the lender to recall the line in the case of an Event of Default (EOD) with the

General Partner. Additionally, in the unlikely event of a market event triggering the simultaneous calling of capital across

multiple lines at once, liquidity pressures could impede an individual LP’s ability to meet accumulated larger calls as these

lines mature. Due to the unevenness of disclosures by GPs, at any given point in time, many LPs are not fully aware of

their cumulative exposure through these facilities.

GP Challenges to Address

Competitive Edge

Subscription lines have the potential to increase time-sensitive return measures substantially and can thereby also

distort fund quartile rankings to the advantage of the funds employing them

3

. Therefore, many GPs feel compelled to

use subscription lines to appear competitive on a benchmarked return basis to attract investors.

Lack of LP Alignment

An additional challenge that GPs face is the lack of alignment among LPs on the utilization of subscription lines. Some LPs

embrace the use of subscription lines as a cash flow management tool while others prefer that they not be used at all, and

fund documentation often leaves vague and unclear guidelines around the use of subscription lines, if any. Additionally,

when LPs are compensated based on IRR, they may look more favorably upon the use of subscription lines than if their

compensation were based on a different metric.

2

A Cobalt analysis of 498 funds found that delaying the first cash flow by up to one year yielded higher IRRs provided TVPI was above 1.0x, whereas delaying capital

calls one year decreased IRR for funds with TVPI under 1.0x. The median IRR increase was 206bps by year 3, falling to 35-45 bps by the end of the fund life for the

funds studied. Source: CobaltGP.com.

3

Distortion or Cash Flow Management? Understanding Credit Facilities in Private Equity Funds (Schillinger, Braun, Cornel 2019)

ILPA Guidance on Enhancing Transparency Around Subscription Lines of Credit: Recommended Disclosures 5

Just as LPs may not be philosophically aligned on the utilization of subscription lines, they may also request different

disclosures from GPs. GPs devote time responding to these bespoke reporting requests from LPs, who in turn may still not

be satisfied with the data they receive.

Recommendations

ILPA believes that guidance on subscription line disclosures will assist LPs and the private equity industry by helping to

create a common reporting standard for the periodic disclosure of amounts outstanding relative to an LP’s unfunded

commitment. The following recommendations reflect incremental reporting that, according to CFOs surveyed by ILPA,

would be feasible for most GPs as some of these metrics are implicit in quarterly and annual reporting today. The request

from LPs is that the following information is provided more explicitly, and where reasonable, on a more regular basis from

their GPs. If there is information that cannot be provided by the GP, an explanation should be provided in each instance

to inform LPs why they are not receiving these recommended disclosures.

The expectation is the recommendations would be reflected in reporting to LPs starting with the reporting period ending

6/30/2020. Due to the foundational nature of information requested in the annual reporting supplement, the data

points below denoted with ** should be included in the first reporting period ending at 6/30/2020. Going forward, the

annual supplemental disclosures would be enclosed within the fund’s annual reporting package, most commonly for the

reporting period ending at 12/31.

While ILPA recommends the preferred documents in which these disclosures are provided, i.e., Partners’ Capital Account

Statement, or PCAP, and the Annual Reporting Supplement, and this guidance offers an illustrative example of both, it is

not intended to serve as a template, i.e., a required format, for GPs to use at this time. The intention is for GPs to start

providing the recommended disclosures if they are not doing so already, rather than depicting the exact format for the

recommended disclosures to be provided.

Specific recommendations are detailed below:

1. GPs using subscription lines should disclose to their LPs on a quarterly basis the following:

As part of the PCAP statement:

• Total size of facility

• Total balance of the facility

• Individual LP and GP’s unfunded commitment financed ($ and %) through the facility

• The average number of days outstanding of each draw down

• Net IRR with and without the use of the facility

Additional disclosures recommended:

• A schedule of cash flows alongside the partner’s capital account statement and schedule of investments

2. GPs using subscription lines should disclose to their LPs on an annual basis the following, as a supplement within the

annual reporting package:

• Total size of facility

• Total balance of the facility

• Individual LP and GP’s unfunded commitment financed ($ and %) through the facility

• The average number of days outstanding of each draw down

• Lead Bank**

• Fund Draw Down Limit**

• Fund Maximum Allowable Borrowing (Days)**

ILPA Guidance on Enhancing Transparency Around Subscription Lines of Credit: Recommended Disclosures 6

• Facility Term Expiration**

• Facility Renewal Option**

• Collateral Base**

• Interest Rate**

• Upfront Fee Rate**

• Unused Fee Rate**

• Additional Fees**

• Total Fees Paid**

• The current use of the proceeds from such lines, i.e., solely to bridge capital calls (and the nature of those

capital calls) or for other purposes (such as accelerated distributions)**

While there is no universally accepted method for calculating Net IRR with and without the use of subscription

lines, annual disclosures should also include:

• Net IRRs both with and without the use of the facility to their investors**

• Clearly defined methodology for calculating these amounts with and without the use of the facility**

3. To provide LPs with greater predictability of capital calls, GPs should:

• Provide LPs with as much notice as possible rather than relying solely on the 10 business day standard (where

a predictable capital call schedule is not already in place), such as in cases where a single capital call is above

an agreed and stated percentage of the total unfunded commitment

4

• Provide an estimate or estimated range of the amount of capital to be called, with the appropriate caveats

regarding how amounts may move – the intention is for the estimate to be directional rather than precise

4. To monitor their exposure, LPs may utilize analytics to derive an estimate of their outstanding liability due to

subscription lines. Data already provided quarterly by the GPs can be used to calculate the exposure to the portfolio

value based on an LP’s ownership percentage as compared to the LP’s NAV disclosed in the Partners’ Capital Account

Statement (PCAP).

• The two data points required for the calculation are the:

• Investment Values on the Balance Sheet

• LP Ownership %, which may be determined by dividing the LP’s NAV by the Fund’s NAV

• With these data points, the LP can get an estimated exposure by multiplying the Investment Value by the LP

Ownership %. For example, with an Investment Value of $100,000,000 and an LP Ownership % of 3%, the

calculation would be:

• $100,000,000 x 0.03 = $3,000,000

• The estimated exposure and the LP’s NAV may differ because of the GP carry since the Investment Value is

gross of carry and the difference can be compared to the LP’s allocation of carry provided on the PCAP

• If the exposure is greater than the NAV, it is caused by Net Other Assets

• If the exposure is less than the NAV, it is caused by Liabilities, which will typically be the LP’s pro rata amount

outstanding on that Investment financed through a subscription line

• Both Net Other Assets and Liabilities can be reviewed on the Balance Sheet

4

The specific percentage should be determined in tandem by the GP and the fund’s LPs; LPs consulted in preparing these recommendations indicated that 20-25% or

higher of an LP’s unfunded commitment was generally deemed worthy of greater advance notice.

ILPA Guidance on Enhancing Transparency Around Subscription Lines of Credit: Recommended Disclosures 7

Illustrative examples of the quarterly and annual disclosures noted above are detailed below. Please note, this is for

illustration purposes only and not intended to prescribe a templated format for GPs to use when providing the

recommended disclosures to LPs.

Subscription Line of Credit Disclosures as of June 30, 2020

Quarterly

Total Size of Facility $ million

LP

Fund GP

Balance of Outstanding Borrowings, for period ending June 30, 2020 $ million $ million $ million

% of Total Outstanding Borrowings, for period ending June 30, 2020 % % %

Average Number of Days Outstanding of each draw down Average Days

Net IRR with use of the facility

%

Net IRR without use of the facility %

Annually

Total Size of Facility $ million

LP

Fund GP

Balance of Outstanding Borrowings, for period ending June 30, 2020 $ million $ million $ million

% of Total Outstanding Borrowings, for period ending June 30, 2020 % % %

Average Number of Days Outstanding of each draw down Average Days

Net IRR with use of the facility

%

Net IRR without use of the facility %

Methodology for calculating Net IRR with and without the use of facility

Lead Bank Bank Name

Fund Draw Down Limit $ million

Fund Maximum Allowable Borrowing Days

Facility Term Expiration MM/DD/YYYY

Facility Renewal option Renewal option statement

Collateral Base Unfunded Commitments, NAV, etc.

Interest Rate %

Upfront Fee Rate %

Unused Fee Rate %

Additional Fees

Total Fees Paid Provide the total $ amount fees paid across all fee types

Current use of the proceeds

Net IRR required to be net of base

fee, carry, and all fund expenses

(including those associated with

the subscription line of credit)

Provide type and % of additional fees paid not already provided

Provide the purpose for using the subscription line of credit (solely to

bridge capital calls, accelerated distributions, etc.)

Net IRR required to be net of base

fee, carry, and all fund expenses

(including those associated with

the subscription line of credit)

Provide insight into timing of when the return calculation begins (first

capital call vs. first fund investment)